/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom has created no shortage of trillion-dollar companies. Investors have watched chipmakers, cloud providers, and software giants add hundreds of billions of dollars in market value as AI reshapes the technology landscape. Yet one of the biggest winners has been hiding in plain sight. While most of the attention has gone to Nvidia (NVDA), memory manufacturer Micron Technology (MU) has quietly become one of the market's most powerful AI plays.

After an extraordinary run over the past year, many investors assume the easy money has already been made. The numbers suggest otherwise.

Memory Has Become the AI Industry's Biggest Bottleneck

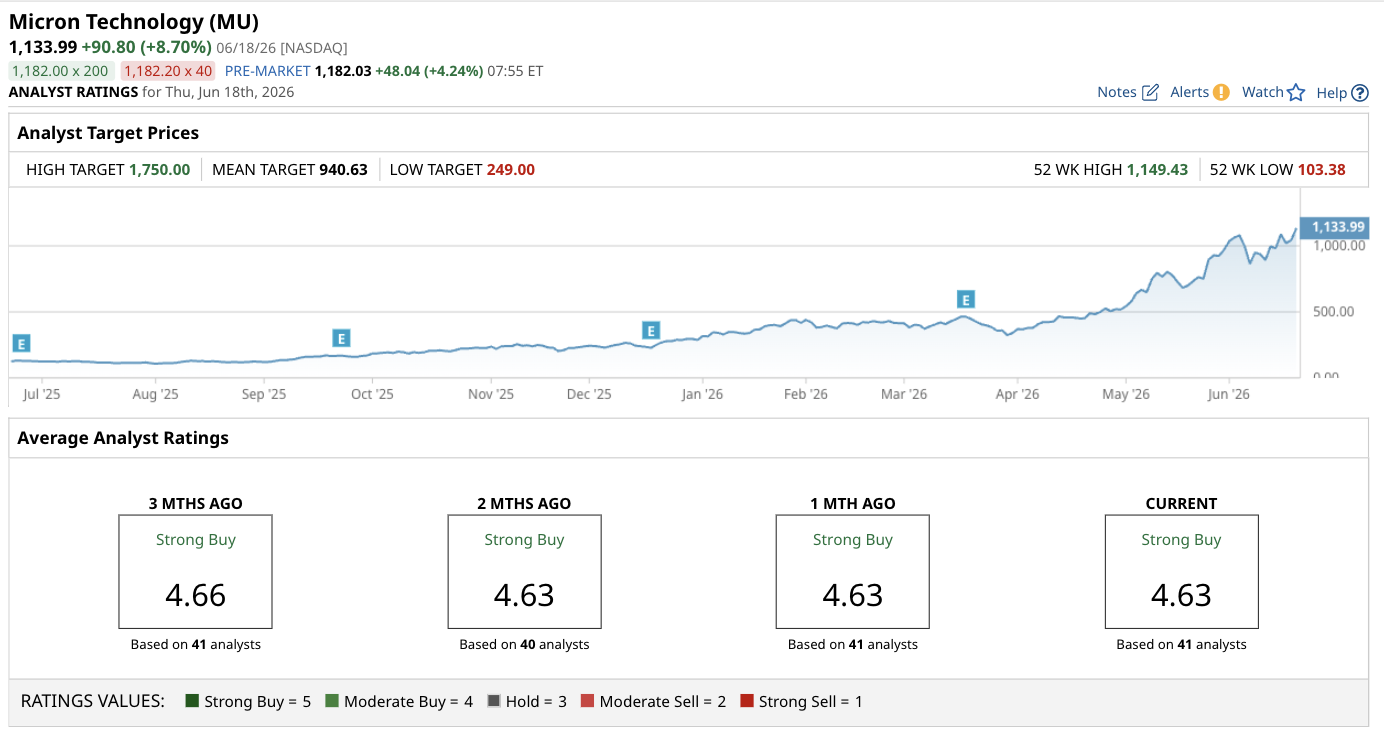

MU stock has climbed 270% year-to-date (YTD) and more than 760% over the last 12 months, pushing its market capitalization to approximately $1.36 trillion. That puts it within striking distance of Meta Platforms (META), valued at roughly $1.42 trillion, while Tesla (TSLA) sits only slightly higher at $1.52 trillion.

Many investors still think of memory as a cyclical commodity business. That description no longer fits. According to comments made by Perplexity CEO Aravind Srinivas during a recent 20VC podcast interview, memory is now one of the primary bottlenecks in AI infrastructure. His observation was simple: Whoever controls the bottleneck controls pricing power.

That's exactly what Micron is experiencing today. High-bandwidth memory (HBM), the specialized memory used in AI accelerators, has seen prices increase roughly fivefold over the past 18 months. Micron has already sold out its entire 2026 HBM production under long-term contracts.

The reason is straightforward. AI demand is consuming every available unit of advanced memory.

AI Agents Could Create an Even Bigger Demand Wave

Memory isn't only required for Nvidia GPUs. It sits at every layer of the AI stack. Data must be stored, moved, processed, retrieved, and analyzed. Every one of those functions requires memory.

The next phase of AI could accelerate that demand. Passive chatbots generate responses. Autonomous AI agents perform tasks. They download files, process information, run workflows, store outputs, and execute multiple compute cycles on behalf of users. Each step increases memory consumption.

The transition from chatbots to agentic AI is not simply a software upgrade. It represents a structural increase in memory demand per user. As AI adoption spreads across enterprises and consumers, the pressure on memory supply could intensify rather than ease.

For Micron, that's a favorable setup.

The Valuation Case Is Stronger Than Many Investors Realize

Micron's operating performance is beginning to reflect those market conditions. In its second-quarter report, the company guided gross margins to reach 81% in Q3. Even more striking, Micron's Q3 revenue guidance exceeds the company's full-year revenue generated in any fiscal year through 2024. Wall Street currently forecasts EPS growth of as much as 127% annually over the next five years.

Yet despite that growth, Micron trades at 11 times forward earnings and carries a PEG ratio of just 0.38 times, compared to Nvidia's 24 times forward earnings and PEG ratio of 0.64 times.

If Micron merely expanded from an 11 times forward earnings multiple to Nvidia's multiple, its valuation would increase greatly. That's also before considering the possibility that Wall Street's growth forecasts prove too conservative. Analysts are significantly raising their price targets on MU stock.

Key Takeaway

In short, Micron is no longer just a memory manufacturer. It has become a critical supplier of AI infrastructure at a time when memory is emerging as one of the industry's most constrained resources.

Granted, no stock rises indefinitely, and expectations have risen alongside Micron's share price. That said, a company growing earnings at a projected 127% annual rate while trading at 11 times forward earnings doesn't look fully valued.

Meta and Tesla are already looking over their shoulders. If AI demand continues pushing memory supply to its limits, Micron's march toward a $2 trillion valuation is not only possible — the underlying math suggests it may be easier to achieve than many investors realize.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)