/DaVita%20Inc%20location-%20by%20sanfel%20via%20iStock.jpg)

Headquartered in Denver, Colorado, DaVita Inc. (DVA) has built its business around kidney care, providing dialysis treatment for patients living with chronic kidney failure. The company, which carries a market cap of about $15.1 billion, operates a broad network of outpatient dialysis centers, clinical laboratories, and home dialysis programs.

Its portfolio also extends to integrated kidney care, disease management, physician services, clinical research, transplant software, and administrative support for healthcare providers.

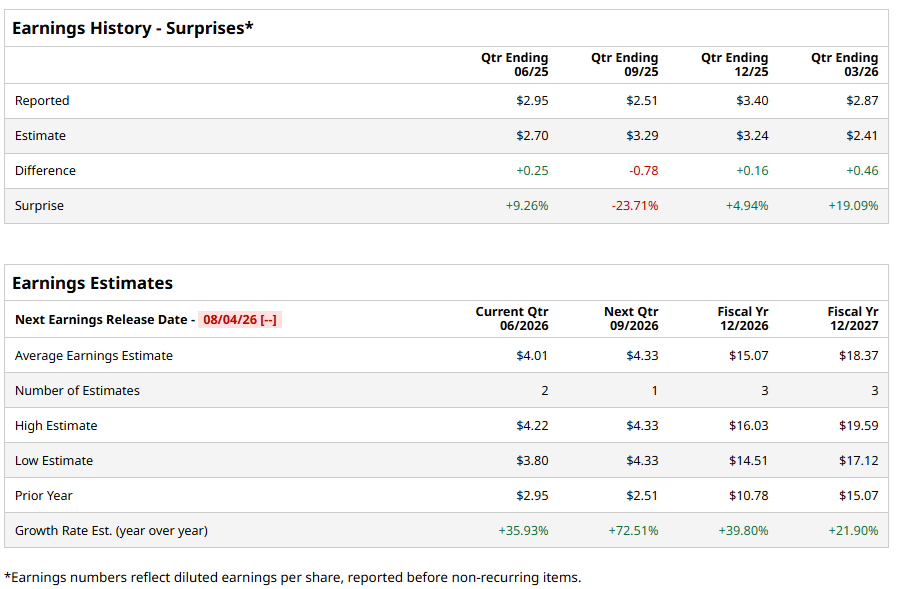

Investors will soon get another look under the hood when DaVita reports its Q2 FY2026 results. Wall Street expects the company to post diluted EPS of $4.01, up 35.9% from $2.95 in the same quarter last year. In fact, DaVita has beaten analysts' earnings estimates in three of the past four quarters, giving the market another reason to watch this report closely.

The optimism does not stop with one quarter. Analysts expect DaVita to deliver FY2026 diluted EPS of $15.07, representing year-over-year growth of 39.8%. They also project FY2027 diluted EPS of $18.37, pointing to another 21.9% increase from the previous year.

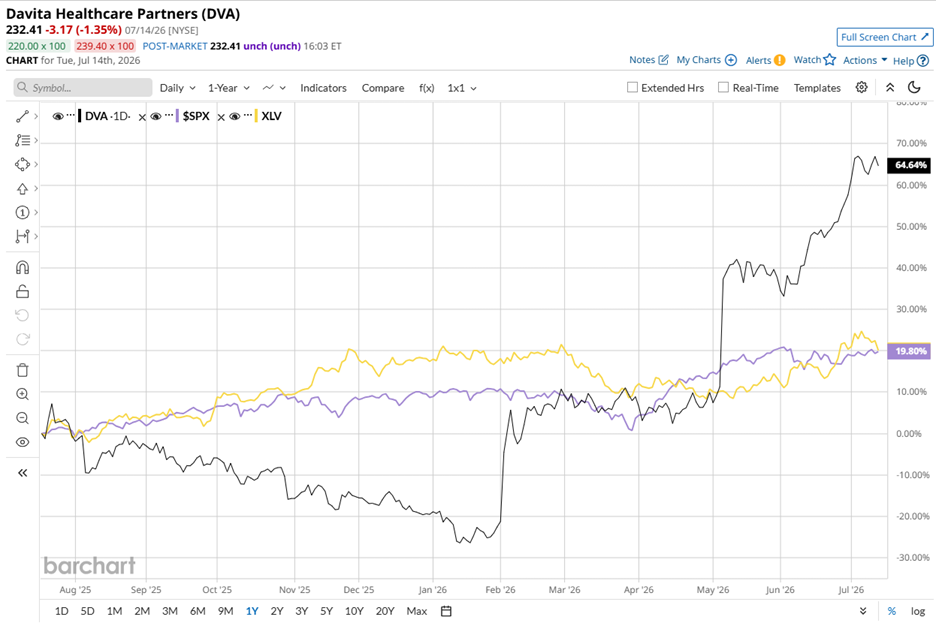

The stock has already rewarded shareholders in a big way. Over the past 52 weeks, DaVita’s shares climbed 62.1%, comfortably outpacing the S&P 500 Index ($SPX), which gained 20.3% during the same period. The gap has widened even further in 2026. DVA stock has soared 104.6% year-to-date (YTD), while the benchmark index surged 10.2%.

The comparison looks just as favorable within the healthcare space. DVA stock outperformed the State Street Health Care Select Sector SPDR ETF (XLV) across both time frames. The healthcare ETF returned 17.2% over the past 52 weeks and gained 2.3% on a YTD basis, leaving DaVita comfortably ahead.

Much of that momentum gathered pace after the company's Q1 FY2026 earnings release on Tuesday, May 5. Investors responded enthusiastically, sending DVA stock up 23.5% on Wednesday, May 6. Revenue increased 6% year over year to $3.42 billion, topping analysts' estimate of $3.35 billion. Adjusted EPS climbed 43.5% to $2.87, beating Wall Street's forecast of $2.33.

Management credited the strong quarter to healthy gains in treatment volume, higher revenue per treatment, disciplined cost management, stronger productivity, and favorable patient outcomes. They also highlighted continued investments in technology and data infrastructure as key drivers of both clinical quality and operational excellence.

Looking ahead, they expect stronger treatment volumes and sustained productivity improvements to support future performance. The company raised and narrowed its adjusted operating income guidance to a range of $2.15 billion to $2.25 billion. Management also lifted adjusted EPS guidance to a range of $14.10 to $15.20 per share.

Wall Street has yet to turn unanimously bullish on DaVita. The stock currently carries an overall “Hold” rating. Among eight analysts tracking the company, two recommend “Strong Buy,” five maintain “Moderate Buy” ratings, and one rates the stock “Moderate Sell.”

Price targets also suggest analysts believe the rally may not have reached the finish line. The stock is already trading above its average target price of $215.28. However, the Street-High target of $270 points to an even stronger potential gain of 16.2%.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.