/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

KeyBanc analysts downgraded Apple (AAPL) to “Underweight” from “Sector Weight” on Tuesday, setting a $250 price target that implies more than 20% downside from current levels. Analyst Brandon Nispel cited weakening hardware demand, slowing upgrade cycles, lower carrier subsidies, and elevated valuation as primary concerns underpinning the bearish call.

The downgrade arrives just one day after Apple stock reached an all-time intraday high of $323.45, capping a nearly 17% year-to-date gain that made it the best-performing Magnificent 7 stock of 2026.

Why Is KeyBanc Bearish on Apple Stock?

KeyBanc’s proprietary spending data showed indexed Apple spending declined 2% month-over-month in June, well below the three-year average of 9% monthly growth.

The investment firm attributed part of the weakness to a normalization following last year’s tariff-related demand pull-forward, when consumers purchased devices ahead of expected price hikes.

Apple recently raised prices across Macs, iPads, and home devices to offset surging memory chip costs, and is expected to raise iPhone prices as well later this year.

What Else Warrants Caution in Playing AAPL Shares?

A central pillar of the downgrade involves U.S. wireless carriers. KeyBanc noted that all three major carriers — Verizon (VZ), AT&T (T), and T-Mobile (TMUS) — have publicly discussed pulling back on device subsidies as handset prices rise.

This shift could lengthen smartphone replacement cycles, weaken U.S. upgrade rates, and force the titan to rely more heavily on international markets to sustain growth, which becomes increasingly difficult in a rising-price environment.

Additionally, KeyBanc sees consensus expectations for 8% iPhone revenue growth in fiscal 2027 as too aggressive — and expects revenue estimates for Mac, iPad, and wearables to move lower as unit growth decelerates.

According to its experts, slower hardware sales will constrain expansion of Apple’s active installed base, creating a knock-on effect on Services revenue growth, which they estimate will decelerate to about 7% in fiscal 2027 versus the consensus forecast of roughly 12%.

Apple Is Vastly Overvalued at Current Price

Valuation was another key concern. Apple is trading at 36x forward earnings and 24.5x KeyBanc’s fiscal 2027 EV/EBITDA estimate, representing a premium of more than two standard deviations above the S&P 500 and Nasdaq.

The investment firm called that premium rather unwarranted given the slowing growth trajectory, especially compared to Apple's 10-year average price-to-earnings multiple of about 23x.

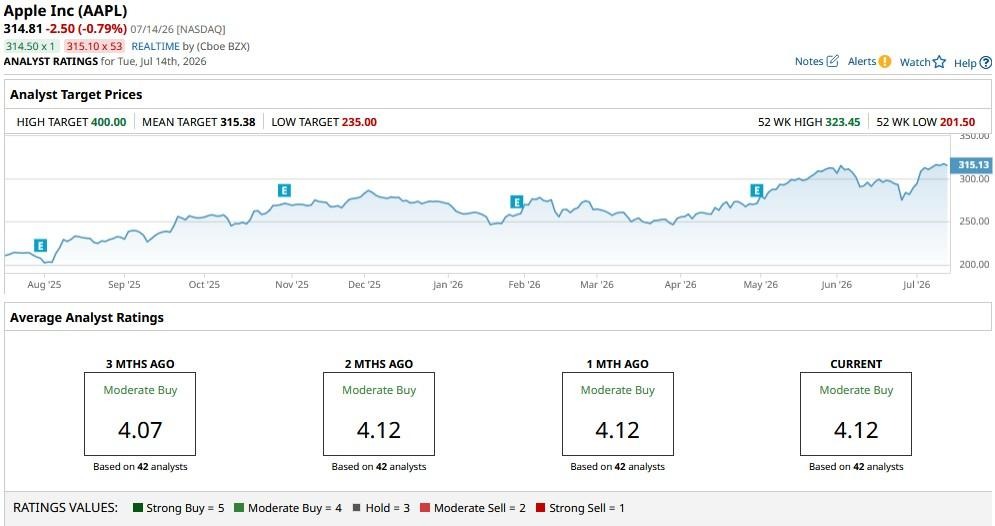

How Wall Street Recommends Apple

KeyBanc’s downgrade is notably rare on Wall Street, where more than half of the 42 analysts that cover AAPL shares recommend buying them.

However, the mean price target on Apple sits at about $315 currently, which is roughly in line with its price at the time of writing.

Investors face a critical near-term catalyst with Apple's fiscal third-quarter earnings scheduled for July 30, which will also serve as outgoing CEO Tim Cook’s final call before John Ternus takes the helm on Sept. 1.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.