/AI%20(artificial%20intelligence)/Close-%20up%20of%20computer%20chip%20with%20AI%20sign%20by%20YAKOBCHUK%20V%20via%20Shutterstock.jpg)

Micron (MU) stock is down 17.5% since June 25, one day after it announced its fiscal second quarter earnings. I had pointed out in my Micron earnings preview that I still had conviction in the company’s business. However, the stock was worth selling considering the volatility and risk involved. As it turns out, the stock’s slump since the earnings has proven that this risk was not worth taking.

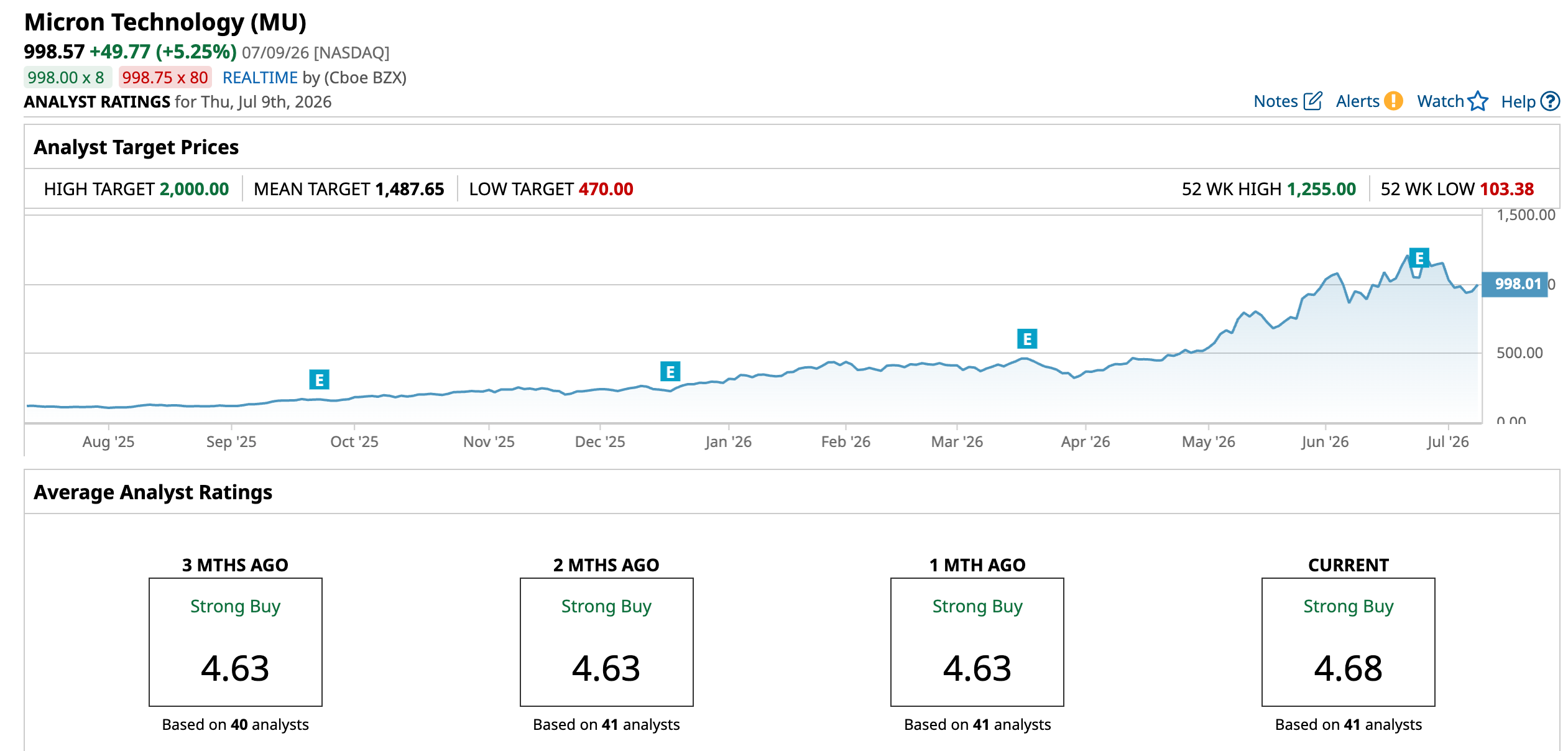

Now that the stock is down, the question arises that if the business is as sound as before, what’s a good entry point? Bank of America Securities came out with an update on July 6, and they have the answer to the above question. To begin with, their price target stands at $1550, so they still see massive upside from this point onwards. Micron is one of their top picks right now.

As for the business, the bank expects global cloud and AI infrastructure spending to cross the $1.5 trillion mark by next year. There is no structural change in AI demand, so once the analysts get better visibility into the 2027 cloud capex across the board, renewed momentum may emerge, especially for names like Micron, Advanced Micro Devices (AMD), and Intel (INTC), among others. Analysts at BofA believe that the market is underestimating the importance of Micron’s long-term agreements and still pricing the stock as if it has reached peak earnings cycle, which doesn't reflect the evidence of AI demand.

About Micron Stock

Micron is a semiconductor company specializing in memory and storage solutions for consumer devices, data centers, and artificial intelligence. The company operates across four segments, including Mobile and Client, Core Data Center, Cloud Memory, and Automotive and Embedded. Most recently, Micron has become a key memory and storage supplier for Anthropic, emphasizing its growing importance in the AI infrastructure supply chain. Led by CEO Sanjay Mehrotra, the company is headquartered in Boise, Idaho.

Over the last 12 months, Micron Technology’s stock has surged 727.6%, vastly outperforming even the Philadelphia Semiconductor Index ($SOX), which gained 130.8% during the same period. The SOX Index has had a remarkable increase due to the AI infrastructure boom as it is dominated by hardware stocks. Micron surpassing it so comfortably reflects the extraordinary investor confidence in the firm, along with the importance of memory as a bottleneck. The record quarterly results and the significant pricing power amidst the global supply shortage have heavily favored the firm.

Micron's valuation remains debated, being cheap on earnings and expensive on revenue. The forward GAAP price-to-earnings ratio of 13.05 times remains well below the sector median of 33.19 times. The stock remains inexpensive on an earnings basis despite a monumental 723% stock price increase in the past year. The forward price-to-sales ratio of 8.27 times is considerably different, sitting over twice the company's own 5-year average of 3.93 times. The company's capital structure and EPS growth projection provide justification for the premium. Micron has a net cash position of $3.79 billion, which makes for a strong balance sheet for a company that has exceeded the trillion-dollar market cap. The EPS growth trajectory is now at an extraordinary 791% in 2026 compared to 635% before the Q3 results. The decline expected in 2029 has also reduced from -72% to -32%, suggesting that analysts’ confidence in the longevity of the AI memory cycle is gradually improving.

Micron Stock Beats Earnings Estimates

Micron reported its third-quarter fiscal 2026 earnings on June 24. The firm delivered record results across every key metric. Revenue reported at $41.46 billion, more than quadrupled year-over-year (YOY) comfortably beating the $35.69 billion consensus. The non-GAAP EPS growth was even more extraordinary, going from $1.91 to $25.11, a more than 13 times increase YOY. The gross margin skyrocketed from the same quarter last year, going from 39% to 84.9%. CEO Sanjay Mehrotra credited the growing strategic value of memory in the AI era as the driver of Micron’s record quarter.

For the fourth quarter, the guided revenue is approximately $50 billion, well over any quarter in the firm’s history. The non-GAAP EPS is also expected to be a record $31.00, plus or minus $1.00. The management expects the free cash flow to increase substantially, which was already at a record $18.3 billion in Q3. The CFO stated that the HBM total addressable market is expected to surpass $100 billion in 2027, a full year ahead of the previous estimate of 2028. Both the CFO and Chief Business Officer underlined that memory supply will be unable to meet demand not just through 2027 but into 2028 as well. The comments suggest that Micron executives believe the current boom isn’t slowing anytime soon.

What Are Analysts Saying About Micron Stock?

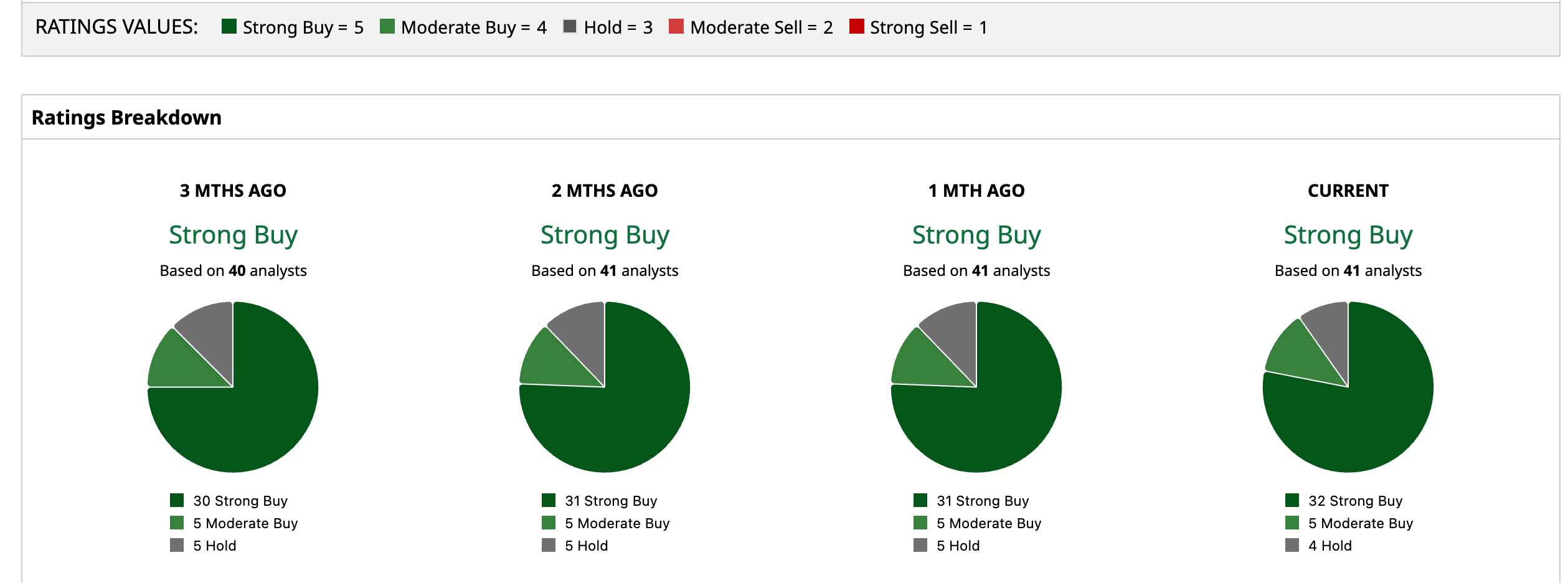

Robert W. Baird analyst Tristan Gerra significantly increased Micron’s price target from $500 to $1280 due to a combination of factors while maintaining a “Buy” rating. The analyst cited the favorable supply-demand outlook, robust data center and AI server growth, and the HBM expected to reach $100 billion in 2027 as reasons for the price target increase. JP Morgan analyst Harlan Sur also nearly tripled Micron’s price target from $550 to $1540 while maintaining a “Buy” rating. Analysts raising the firm’s price target so drastically is indicative of the strength of Micron’s recent financial performance.

Based on the 41 Wall Street analysts, Micron holds a “Strong Buy” rating, with a mean price target of $1,487.65, indicating a 49% upside. Prior to the Q3 results, the mean price target was $916.06, suggesting a 19% downside. This shows that earlier analysts believed the rapid stock rise had made the company’s stock overvalued, but with a record quarter and continued momentum expected, analysts’ confidence in Micron has further increased.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)