/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

As Micron (MU) tumbled on the semiconductor selloff triggered in part by news coming out of South Korea, investors contemplated whether to take profit before today's earnings. The earnings come out later today and will be an eagerly awaited event, especially in the context of what happened in South Korea yesterday. The Korea Composite Stock Price Index ($KSIC) crashed on rumors that memory demand may be slowing down. The index had already nearly doubled year-to-date (YTD) and with extremely high leverage, this was bound to happen sooner or later.

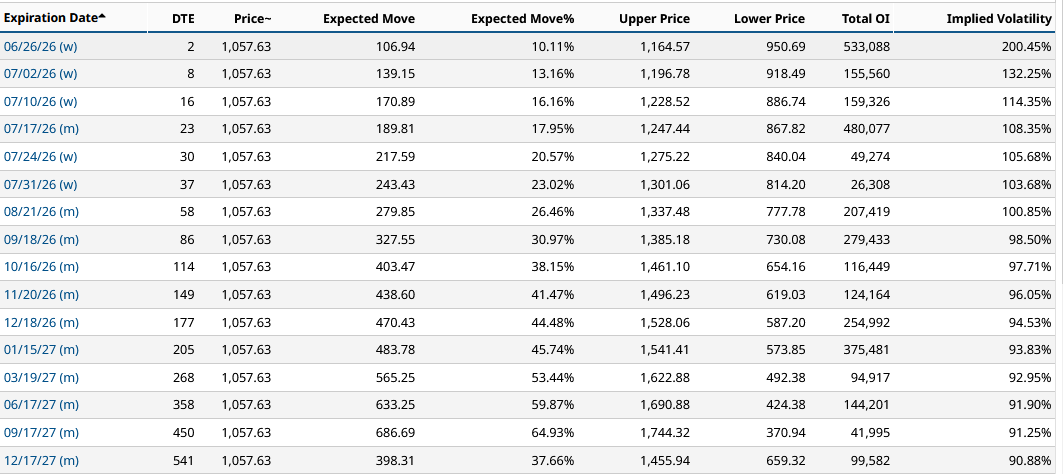

The problem for Micron investors is that this happened a day before the earnings release, not an ideal time for someone betting on an earnings beat. If you’re one of those, you’re not only down on your investment but staring at massive volatility post-earnings. Data from Barchart’s Micron Option Prices suggests an extreme move either side of the stock price.

MU stock is pricing an expected move of $106.94 as of today’s trading. This equates to a 10% move, showing how the earnings call is a binary event for many traders. The farther you move from this week’s expiration date, the higher the expected move becomes. This is not the type of earnings play where you could wait out a quarter to avoid losses. If there is even a hint of a slowdown in memory demand, the stock could tank and continue to do so over the coming weeks.

While many continue to look at memory demand to decide whether to sell or hold the stock, it is clear that this is a binary move, and therefore, the selling decision comes down to controlling your risk rather than checking your conviction. The AI buildout is still in its early stage, there is no doubt about that. Memory demand may come down from the current extremely high levels, but it is likely to persist as a bottleneck. What you’re not going to get is an elevated stock price if the earnings don’t pan out well. The trading decision, therefore, comes down to a matter of risk control rather than a lack of conviction.

About Micron Technology Stock

Micron Technology is a semiconductor company that designs and manufactures memory and storage products. Its product portfolio includes DRAM, NAND flash memory, High Bandwidth Memory (HBM), and Solid-State Drives (SSDs). The firm operates globally, serving cloud providers, technology companies, and enterprise customers. Founded in 1978, the company is headquartered in Boise, Idaho, and is led by CEO Sanjay Mehrotra.

Over the last 12 months, MU stock has gained an extraordinary 712%, comfortably outperforming the S&P 500 ($SPX), which rose 21.8% during the same period. Having recently crossed the $1000 mark, the stock currently sits relatively near its 52-week high. The surge has been driven primarily by the rise in AI infrastructure demand, with Micron’s High Bandwidth Memory chips being supplied to Nvidia (NVDA) for its Blackwell GPU platform. The stock price further increased after Micron was approved to supply HBM4 to Nvidia for its next-generation Vera Rubin platform, boosting investor confidence in the firm’s growth prospects.

Micron’s valuation can look highly overvalued or undervalued depending on which metric the investors focus on. The forward GAAP P/E is 17.33x, which is 47% below the sector median. The stock looks relatively cheap despite a 712% rise in the past year, showing how monumental the firm’s recent earnings growth has been. The forward price-to-sales (P/S) ratio, however, is 10.42x compared to the sector median of 3.25x and well above the company’s own 5-year average of 3.86x.

The biggest risk factor for the investors is the firm’s long-term EPS consensus, with the EPS growth expected to slow dramatically in 2028, before declining sharply by 72% in 2029. Nonetheless, the extraordinary estimates of 635% EPS growth in 2026 and 93% in 2027 suggest the analysts remain confident that the AI boom will continue to offer Micron great returns in the near term. The company being $3.79 billion net cash positive provides further reassurance to investors that if the memory cycle turns negative, Micron has the financial strength to survive and recover.

Micron Continues to Post Incredible Earnings Growth

Micron reported its second-quarter fiscal 2026 earnings on March 18. The firm had a record quarter in key metrics like revenue, EPS, gross margin, and free cash flow. Revenue was reported at $23.86 billion, nearly tripling year-on-year (YoY) from $8.05 billion, and comfortably above the analyst consensus of $20.07 billion. The non-GAAP EPS increased almost 8 times, going from $1.56 to $12.20, shattering the EPS consensus of $8.73. The CFO stated that the firm was able to end the quarter with the highest net cash position in the firm’s history.

For the next quarter, the CEO expects the firm to break its financial records again. The revenue guidance is approximately $33.5 billion, which exceeds every full-year revenue of the company’s history through fiscal 2024. The company expects a record EPS of roughly $19.15, representing over 900% growth from the same quarter last year. The CFO stated that the higher price, lower cost, and favorable mix will help the firm achieve a gross margin of nearly 81%. Since the March results were reported, analyst sentiment heading into the next report is overwhelmingly positive, which is also reflected in the drastic recent stock rise.

What Analysts Are Saying About MU Stock

Stifel Nicolaus analyst Brian Chin significantly increased his MU stock price target from $550 to $1500 while maintaining a “Buy” rating. The revision comes after AI-driven demand more than doubled DRAM prices from what the analyst originally estimated. Wedbush analyst Matt Bryson also increased his price target from $550 to $1300 while maintaining an “Outperform” rating, after significantly boosting the firm’s revenue and EPS estimates.

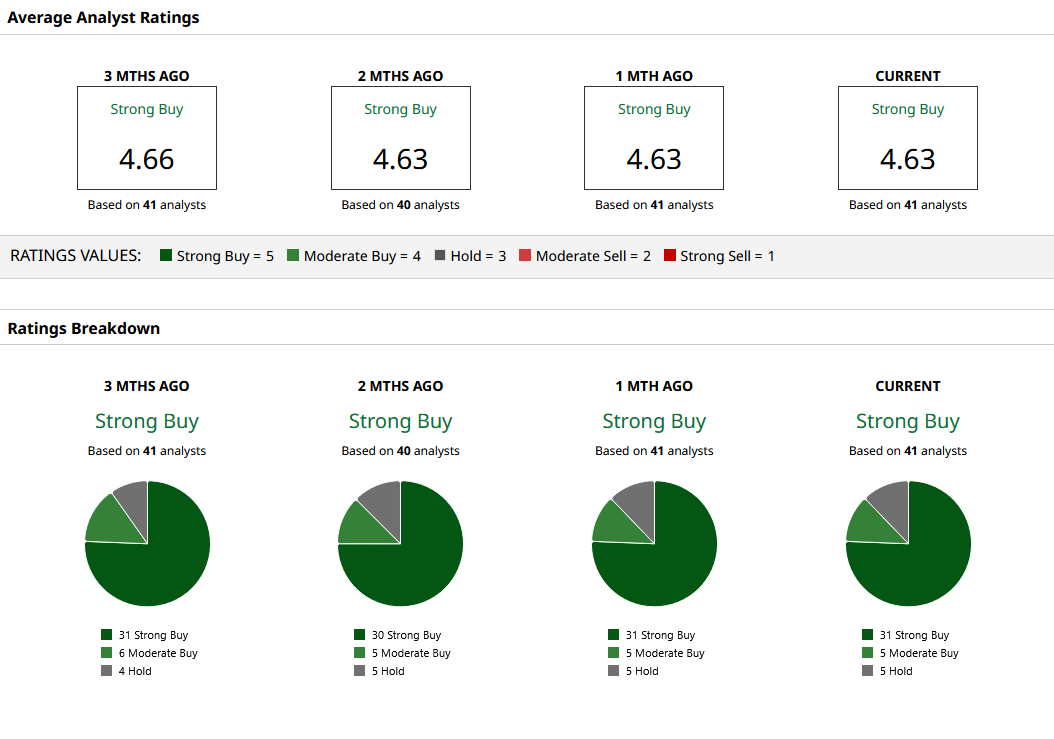

Based on the 41 Wall Street analysts, MU stock holds a “Strong Buy” consensus rating. The mean price target is $1,058.91, indicating a slight 2% upside from its current price. The overall consensus suggests that while the stock's rapid rise may make it look slightly overvalued, the analysts still expect the firm to grow meaningfully.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)