I highlighted the differentials between U.S. and European natural gas prices in an April 24, 2026, Barchart article, where I concluded with the following:

As European and Asian LNG demand rises due to the ongoing war in Ukraine and hostilities in the Middle East, demand for U.S. LNG could rise, keeping prices elevated and above critical technical support levels. The differential between U.S. and European/Asian natural gas prices could prove bullish for NYMEX U.S. natural gas futures over the coming months if hostilities continue or escalate.

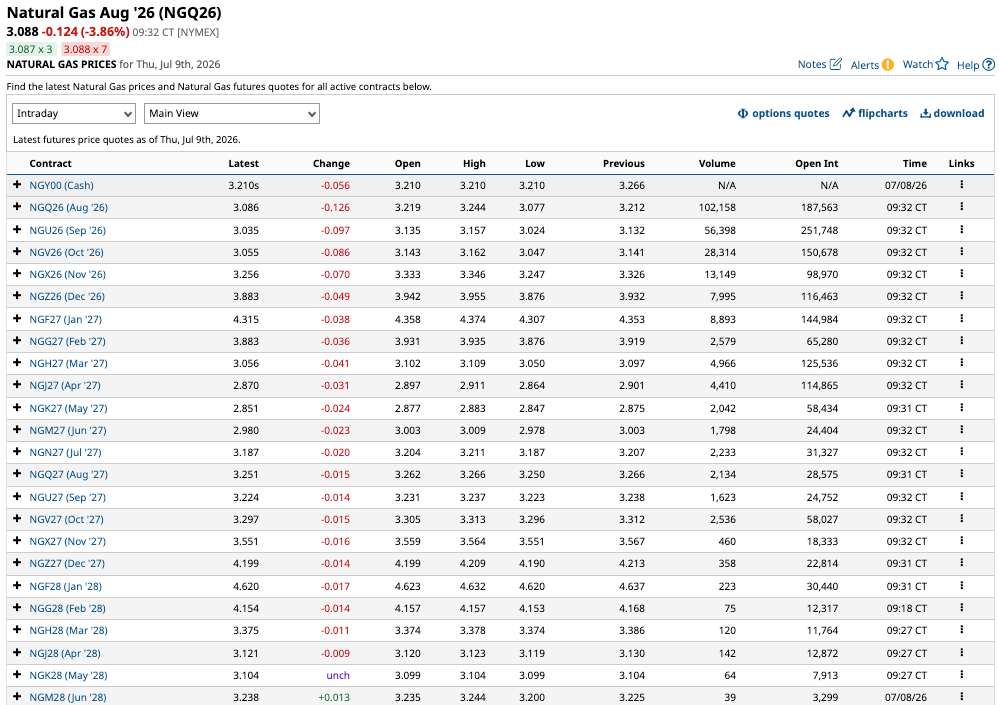

Nearby U.S. NYMEX natural gas prices were at the $2.73 per MMBtu on April 23. In July 2026, prices were above $3 per MMBtu on the nearby August contract.

A bullish bias in U.S. natural gas futures

U.S. natural gas futures reached a low of $2.561 per MMBtu on April 14, 2026, during the shoulder season when heating and cooling demand are absent from the energy commodity.

The daily chart shows a pattern of higher lows since mid-April, which took natural gas futures to a high of $3.396 per MMBtu on June 1, 2026. At over $3.00, natural gas remains slightly above the midpoint between the mid-April low and the early June high. While the energy commodity has made higher lows, it has settled into a trading range between just over $3 and just below $3.40 since late May, but it threatened the bottom of the range on July 9.

The forward curve displays seasonality

U.S. natural gas is a highly volatile energy commodity that displays significant seasonality.

The forward curve from August 2026 through June 2028 shows that prices reach highs during the winter heating season and lows during the shoulder season in April-May, then start to climb gradually during the summer cooling season.

The Middle East remains volatile

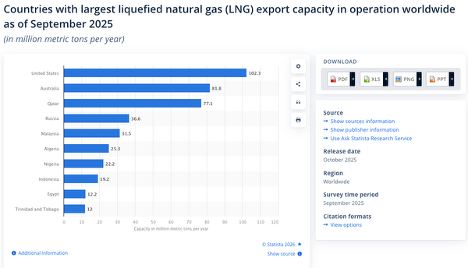

U.S. natural gas futures began trading on the CME’s NYMEX division in 1990, when the energy commodity was transported only by pipeline in the Americas. Technological advances in liquefication created the opportunity to export LNG beyond the pipeline network to regions where prices are far higher. The U.S. has become the world’s leading natural gas-producing and exporting country.

The chart shows that the United States has the largest LNG capacity. Australia is second, with its exports going to Asia due to its geographic position. Qatar and Russia rank third and fourth, with combined export capacity exceeding that of the U.S.

Europe has historically depended on Russia and Qatar for LNG, but sanctions and retaliatory measures stemming from the ongoing war in Ukraine have limited Russia’s LNG exports to Europe. In 2026, hostilities around the Strait of Hormuz will further limit European access to Qatari LNG, thereby increasing demand for U.S. LNG.

The Strait of Hormuz is a critical logistical chokepoint for crude oil, LNG, fertilizers, and other commodities. The ongoing situation in the Middle East has led to supply shortages and concerns about future supply disruptions.

European prices reflect uncertainty

European natural gas futures remain elevated in July 2026.

The continuous monthly chart of U.K. natural gas prices shows that, at 119.68 on July 9, 2026, prices are higher than in July 2025, when they traded between 76.56 and 87.61, and in July 2024, when they traded between 70.00 and 87.25.

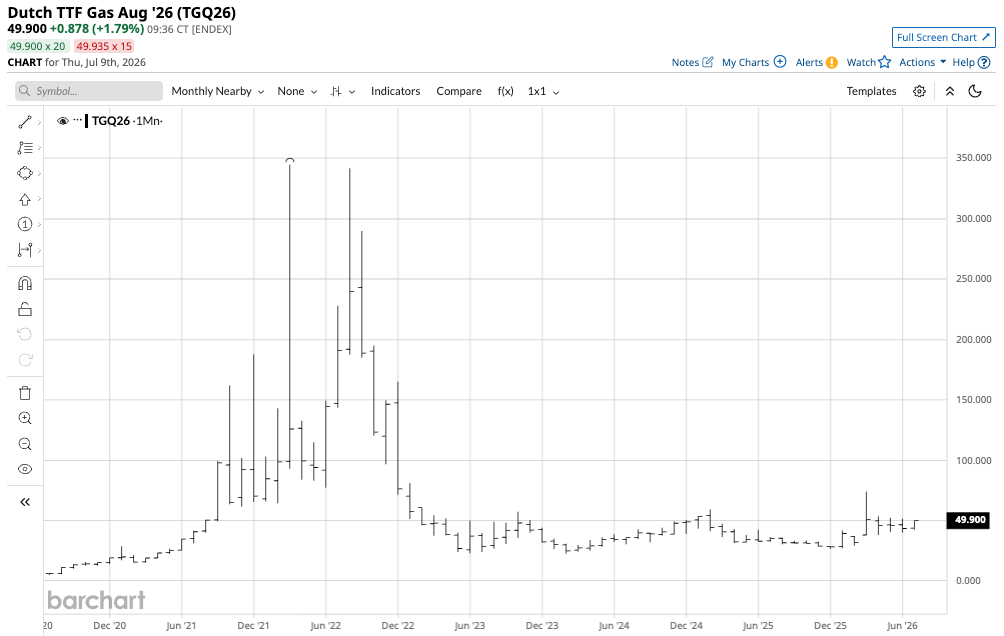

The continuous monthly chart of Dutch natural gas prices shows that, at 49.90 on July 9, 2026, prices are higher than in July 2025, when they traded between 32.365 and 36.32, and in July 2024, when they traded between 30.325 and 36.00.

Elevated European natural gas prices, sanctions on Russia, and issues in the Strait of Hormuz are increasing European demand for U.S. LNG.

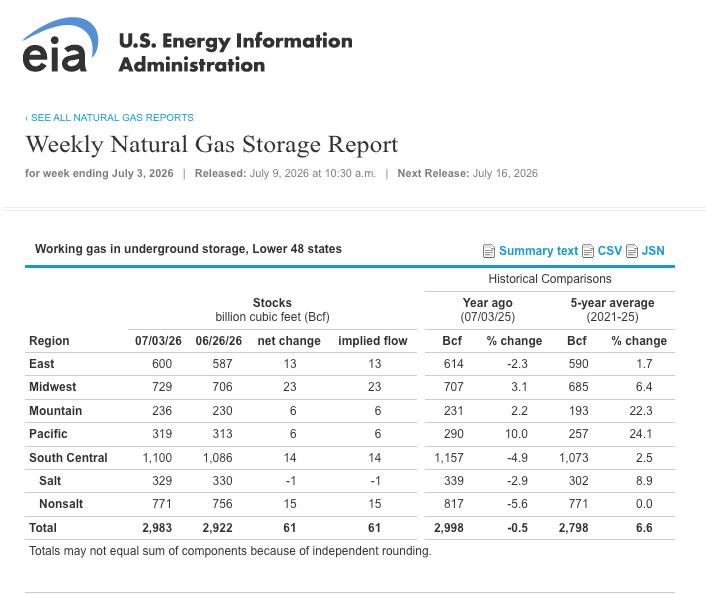

The chart shows that while natural gas inventories across the United States were 6.6% above the 5-year average for the week ending on July 3, 2026, they were 0.5% below the level in early July 2025. Increased demand for LNG is likely to lead to lower U.S. inventories this year compared to last.

Meanwhile, U.S. energy policy under the Trump administration supports a “drill-baby-drill” and “frack-baby-frack” approach to crude oil and natural gas production to achieve energy independence and increase exports. As of the week ending July 2, 2026, Baker Hughes reported 126 U.S. natural gas rigs operating, up from 108 at the same time in 2025. The bottom line is that natural gas inventories are below the previous year’s level, and production has increased, reflecting higher LNG demand from Europe and other regions with higher natural gas prices, with supply fears driving U.S. exports higher.

The bullish trend in natural gas prices likely reflects increasing LNG demand. As the peak winter demand season approaches, the issues facing Russian and Qatari exports could ignite a substantial rally in the U.S. natural gas futures market.

BOIL and KOLD are useful U.S. natural gas trading tools

Natural gas is a highly volatile energy commodity.

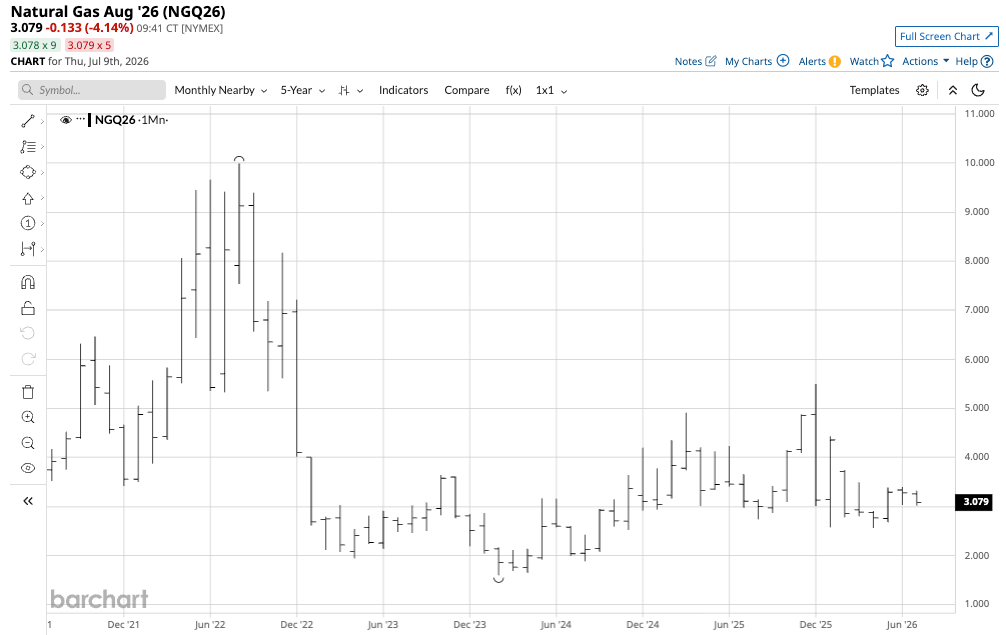

The five-year monthly continuous U.S. natural gas futures chart shows a range of $1.60 to $9.987 per MMBtu. The low was in February 2024, when a warm winter and the approaching shoulder season drove prices lower, while the high was in August 2022, when a hot summer increased cooling demand, causing a surge in domestic power demand, and climate change policies under the Biden administration led to production cuts.

At $3.079 per MMBtu, continuous U.S. natural gas futures prices are around $1.50 above the five-year low, and $6.90 below the high. Natural gas price volatility makes the energy commodity more suitable for trading than investing.

The most direct route for a risk position in natural gas is the CME’s NYMEX futures and futures options contracts. Natural gas futures require specialized trading accounts with margin requirements, which create leverage in an already volatile market. The United States Natural Gas Fund (UNG) is an unleveraged product that tracks U.S. natural gas futures prices. At $11.02 per share, UNG had $412.38 million in assets under management. UNG trades an average of over 5.43 million shares per day and charges a 1.24% expense ratio. UNG is a liquid ETF.

My favorite ETF trading products in the natural gas sector are the bullish Ultra Bloomberg Natural Gas 2X ETF (BOIL) and its bearish counterpart, the Ultrashort Bloomberg Natural Gas -2X ETF (KOLD).

At $24.50 per share, BOIL had over $309.46 million in assets under management. BOIL trades an average of over 3.26 million shares per day and charges a 0.95% expense ratio. BOIL is a liquid leveraged ETF.

At $25.16 per share, KOLD had over $133.9 million in assets under management. KOLD trades an average of over 3 million shares per day and charges the same 0.95% expense ratio. KOLD is also a liquid leveraged ETF.

UNG, BOIL, and KOLD only trade during U.S. stock market hours. Since futures trade around the clock, the ETFs can miss highs or lows that occur when the stock market is closed. Meanwhile, the leveraged BOIL and KOLD ETFs experience significant time decay because they use options and swap contracts to create their gearing, making them appropriate only for short-term trading. Stable natural gas prices will cause BOIL and KOLD to lose value, while price moves in the opposite direction will magnify losses. A risk-reward plan and discipline to accept losses in the quest for greater profits is critical for success with the leveraged BOIL and KOLD ETFs.

With the peak cooling season in high gear, the heating season on the horizon, and U.S. LNG demand soaring, this could be the perfect time to put natural gas on your trading radar. BOIL and KOLD are trading products that can enhance trading results as the volatile energy commodity follows a volatile path over the coming weeks and months.

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)