/A%20close-up%20shot%20of%20the%20Taiwan%20Semi%20logo%20on%20a%20corporate%20building%20by%20Jack%20Hong%20via%20Shutterstock.jpg)

The excitement surrounding artificial intelligence (AI) stocks has tempered down again, with fears of an AI bubble resurfacing. While investors debate whether the AI trade has gone too far, Taiwan Semiconductor (TSM) (TSMC) heads into another quarterly report with exceptional momentum.

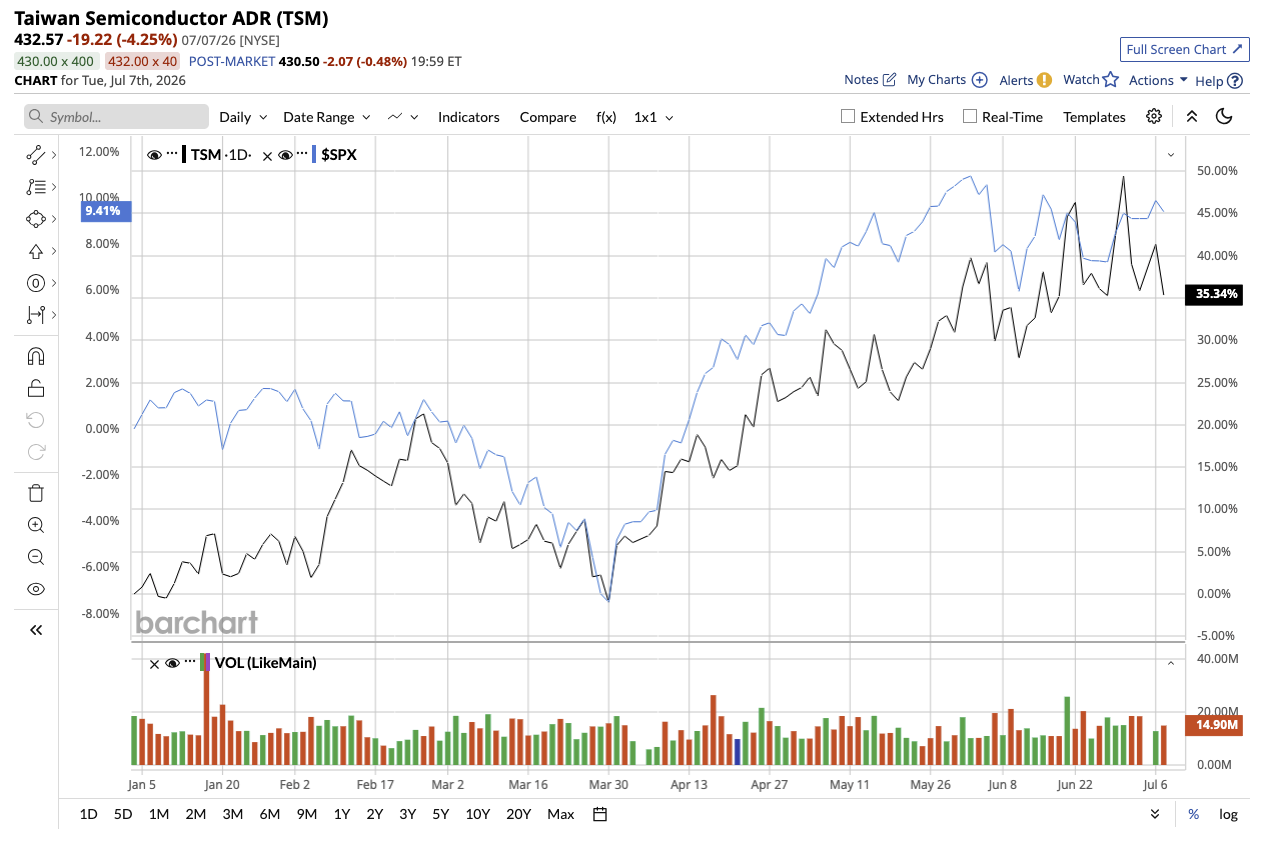

TSMC will kick off the tech sector’s high-stakes earnings season with its second-quarter results on July 16. TSM stock has climbed 46% year-to-date (YTD), outperforming the broader market's gain of roughly 10% so far this year.

Let’s take a closer look at what investors can expect from TSMC this quarter.

TSMC Heads Into Q2 Earnings With Exceptional Momentum

TSMC enters the Q2 earnings report after delivering one of its strongest quarters in recent years. Revenue surged 41% year-over-year (YOY) to $35.9 billion in Q1, with EPS up 58%, driven by demand for its most advanced technologies. Using advanced fabrication technology, TSMC manufactures chips designed by customers such as Apple (AAPL), Nvidia (NVDA), and AMD (AMD), among others.

In the quarter, advanced technologies at 7-nanometer and below generated 74% of total wafer revenue, highlighting how quickly customers continue migrating toward TSMC's latest and most advanced process nodes. High-performance computing (HPC) revenue increased 20% sequentially, one of the clearest signs that AI infrastructure spending is flowing directly into TSMC's fab. As demand increases faster than the company can meet it, TSMC is adding another 3nm fab in Taiwan's Tainan Science Park, with volume production set to begin in the first half of 2027. Additionally, the company's second Arizona fabrication plant is slated to enter volume production during the second half of 2027, while its second Japanese fab will likewise adopt 3nm technology with production beginning in 2028.

Management emphasized that, even after increasing capital spending and accelerating factory construction, supply remains constrained, as building a leading-edge fabrication plant is a lengthy process. Specifically, a new fab takes roughly two to three years to construct with another one to two years before reaching full production. This also highlights the fact that building a new fab is not an easy feat. This is why TSMC’s experience and leadership create high switching costs for customers, giving it a competitive edge in the industry.

Guidance Has Raised the Bar Even Higher

For Q2, management projects revenue between $39 billion and $42 billion, representing 32% YOY growth at the midpoint. Gross margin is expected between 65.5% and 67.5%. Furthermore, analysts forecast a 53% increase in earnings despite the company’s heavy investments in future manufacturing capacity.

During the Q1 earnings call, CEO C.C. Wei repeatedly stressed that AI-related demand remains "extremely robust,” as the industry shifts from generative AI toward agentic AI. Management further emphasized that cloud service providers' spending massively reinforces the idea that the AI semiconductor cycle is a multiyear opportunity rather than a temporary spending wave. TSMC justified its higher capital spending target of $52 billion to $56 billion for 2026, stating that demand from HPC and AI applications remains strong. For the full year, TSMC now expects revenue to grow above 30%.

Despite the massive spending, TSMC's balance sheet remains robust, with $106 billion in cash and marketable securities at the end of Q1. After such an exceptional quarter and upbeat outlook, investors will be watching whether the company once again raises its outlook and whether AI-related demand remains as intense as it was three months ago. Investors might also want proof that the company's enormous capital spending plans are enough to keep pace with customers who continue to ask for more leading-edge capacity. If Taiwan semiconductor reports another stronger-than-expected quarter, it may reassure investors who have recently been questioning the outlook for AI stocks.

What Does Wall Street Think of TSM Stock?

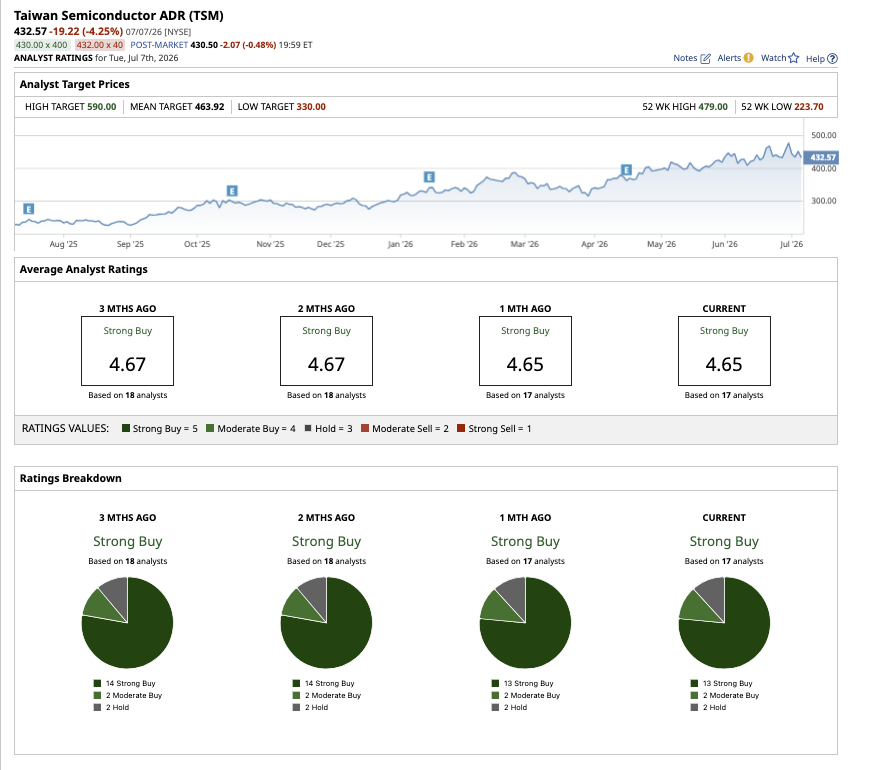

Some analysts have raised their price targets for TSM stock, anticipating another strong quarter. Recently, BofA hiked its target to $590 from $490, citing stronger-than-expected demand for AI processors. The firm believes revenue in 2026 and 2027 will grow by 40% and 39%, respectively. In late June, Barclays also increased its target price to $625 from $470 with a “Buy” rating.

On Wall Street, TSM stock holds a consensus “Strong Buy” rating. Out of 17 analysts with coverage, 13 rate the stock as a “Strong Buy,” two have a “Moderate Buy" rating, and two analysts recommend a “Hold.” The average price target of $463.92 implies the stock can climb by 5% from current levels, while Barclays' high target of $625 suggests potential upside of 42% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)