Public Storage (PSA) is a leading real estate investment trust (REIT) that acquires, owns, develops, and operates self-storage facilities across the U.S. Its business centers on renting storage space for personal and commercial use, along with related services such as merchandise sales and tenant protection. The company’s headquarters is in Frisco, Texas and has a market capitalization of $57.71 billion.

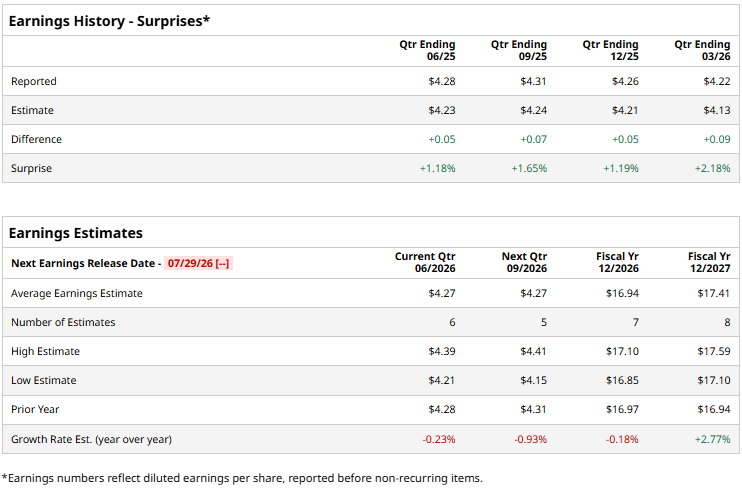

Public Storage is set to report its second-quarter results for fiscal 2026 soon. Ahead of the results, Wall Street analysts expect the company to report a profit of $4.27 per diluted share for Q2, down marginally year-over-year (YOY). However, the company has a solid track record of exceeding consensus estimates, topping them in all four of the trailing quarters. For the full fiscal year 2026, Wall Street analysts expect Public Storage’s profit to decrease slightly to $16.94 per share, followed by a 2.8% YOY improvement to $17.41 per share in fiscal 2027.

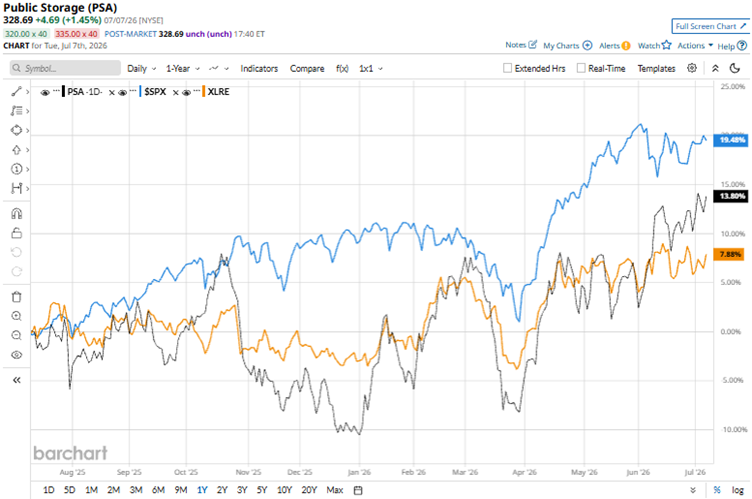

Investors have rewarded Public Storage for its stable self-storage cash flows, dividend appeal, and continued earnings resilience. The company’s stock has gained 12.6% over the past 52 weeks and 26.7% year-to-date (YTD). On the other hand, the broader S&P 500 Index ($SPX) has increased by 20.5% and 9.6% over the same periods, respectively. Therefore, PSA has underperformed the broader market over the past year.

Next, we compare the stock’s performance with that of its own sector. The State Street Real Estate Select Sector SPDR ETF (XLRE) has gained 8.2% over the past 52 weeks and 11.3% YTD. Therefore, Public Storage has outperformed its sector over the past year.

Last month, Public Storage announced that its operating partners, Public Storage OP, L.P. and Public Storage Operating Company (PSOC), have entered into an agreement to acquire Public Storage Canada for $1.20 billion, which gives the company exposure to the growing Canadian self-storage industry with low supply ratios. In the first quarter, Public Storage reported $4.22 in core FFO per share, higher than Street analysts had expected. Moreover, core FFO grew 2.4%, while total self-storage revenue increased 2.6% in the first quarter of 2026.

Wall Street analysts have been bullish about Public Storage’s future. Among the 19 analysts covering the stock, the consensus rating is “Moderate Buy.” The rating configuration has stayed stable over the past three months. The ratings consist of seven “Strong Buys” and 12 “Holds.” The mean price target of $332 implies a modest 1% upside from current levels, while the Street-high price target of $363 implies 10.4% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)