I frequently analyze ETFs whose returns are tied to the movement of volatility, specifically to the Cboe Volatility Index ($VIX). I have tracked and have owned several of them over the years.

To me, being “long” volatility is the key feature of these ETFs. It allows me an alternative to S&P 500 Index ($SPX) put options.

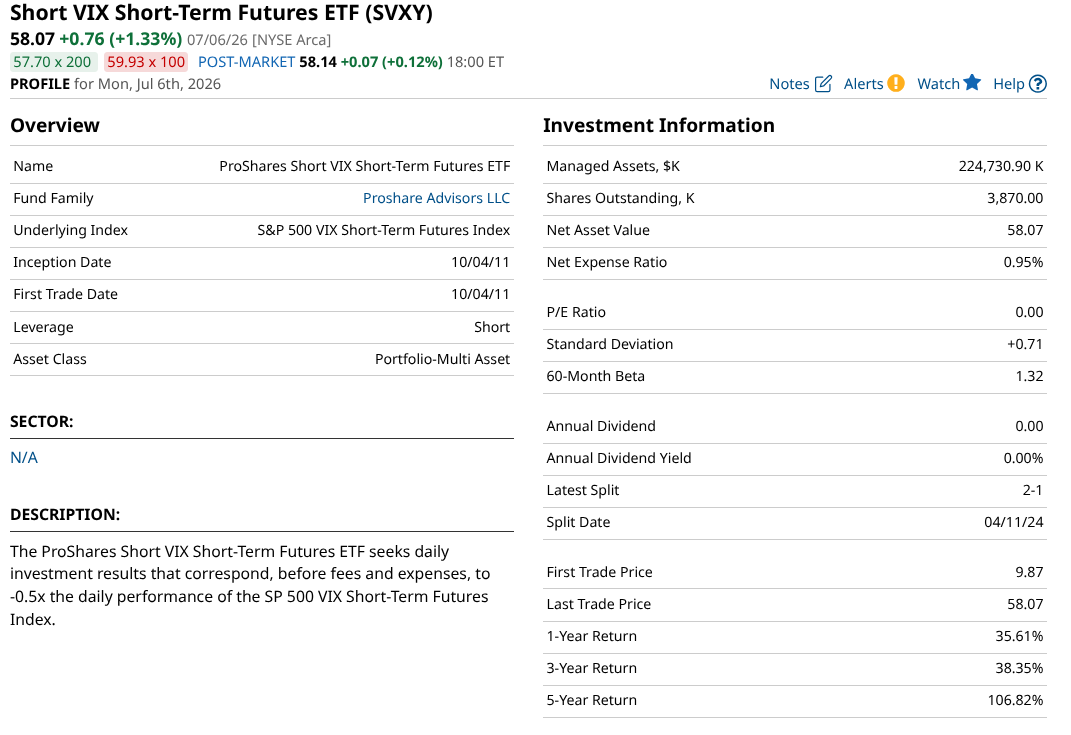

Now, though, I’m interested in a different volatility story: the ProShares Short VIX Short-Term Futures ETF (SVXY).

SVXY is a volatility-driven ETF. However, its goal is to profit from a decline in the $VIX. That is typically what happens when the S&P 500 is rising.

For simplicity, think of it this way. If ETFs like the ProShares VIX Short-Term Futures ETF (VIXY) and ProShares VIX Mid-Term Futures ETF (VIXM) are the ETF world’s alternative to owning put options, SVXY is more like using ETFs as S&P 500 call options. As I see it, these types of funds will always be small holdings. They are just too volatile to be larger positions in your portfolio.

That said, if I allocate 1%, 2% or 3% of a portfolio to SVXY, that’s all I can lose. But the upside can be pretty big.

Why is SVXY a play to consider now?

Following brief, localized spikes in the VIX, the market’s broad “fear gauge,” the standard spot VIX has continuously struggled to maintain any persistent upward momentum, routinely sliding back toward its historical baseline. As someone who continuously hedges his equity portfolio against sudden disaster, this is something I see every day, in vivid color.

In fact, recently, I’ve pointed out in my work here the many cracks I see in the U.S. equity market, particularly the Nasdaq-100 Index ($IUXX), which has led the broader market higher for years. So the idea of volatility steadily declining as it has recently doesn’t add up cleanly to me.

But I’m devoted to the charts. And if I follow them as I read them, there is a growing trend toward a lower $VIX, and thus a higher SVXY.

SVXY has been around for nearly 15 years, and is under the radar at just $224 million in assets. Interestingly, this ETF has more than doubled over the past five years, up 107%. That’s versus SPY’s return of 71%.

That’s right, SVXY has been an S&P 500-beater, during a period of historically high returns for the stock market.

SVXY’s holdings structure is super simple. It uses $VIX futures out to the next two months, so July and August in this case. It acts as a commodity pool in this regard, using cash and Treasury collateral to sell those short near-term VIX futures contracts — specifically balancing positions across the front-month and second-month contracts daily.

To effectively use SVXY, you must understand the underlying plumbing of this unique ETF. It does not track the spot CBOE Volatility Index directly. Instead, it seeks daily investment results corresponding to exactly one-half the inverse (-0.5x) of the daily performance of the S&P 500 VIX Short-Term Futures Index.

The main fundamental edge for short-volatility strategies like SVXY does not just rely on the spot VIX dropping. It also relies on the mathematical structure of the VIX futures curve. Historically, VIX futures reside in a state of contango roughly 84% of the time. This means that longer-dated futures trade at a premium to the near-term expiring contracts.

While long-volatility funds like VIXY or VIXM suffer from a continuous, wealth-destroying roll cost — mechanically forced to “buy high and sell low” every day — an inverse vehicle like SVXY sits on the exact opposite side of that equation. It harvests this roll yield premium as the more expensive contracts slide down the curve toward the cheaper spot price. During extended periods of market calm, what is a headwind for long-vol investors acts as a compounding tailwind for short-vol ETFs like SVXY.

Note that the structural design of SVXY was permanently altered following the 2018 “Volmageddon” collapse, when the old -1.0x inverse vehicles suffered near-100% single-day liquidations. By cutting the daily leverage mandate in half to -0.5x, ProShares, the fund’s manager, insulated the fund from instant extinction during a rapid, overnight VIX doubling.

Still, severe tail-risk remains an inherent factor of the daily reset mechanism. I go back again to the idea of lower position size as my personal risk management move to counter this.

The other way I use SVXY is to pair it with cash instead of owning a higher position in SPY, QQQ or similar ETFs. It can even be paired with VIXY or VIXM and a lot of cash to construct a “long volatility” trade. However you consider them, be proactive and educate yourself. The more wide-ranging your tool kit in these markets, the more chances you have to win.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)