With a market cap of $122.3 billion, Vertiv Holdings Co (VRT) is a global provider of critical digital infrastructure solutions, offering integrated hardware, software, analytics, and services that help customers keep their essential applications running reliably and efficiently. It delivers innovative power, cooling, and IT infrastructure solutions for data centers, communication networks, and commercial and industrial facilities, supporting scalable growth from the cloud to the network edge.

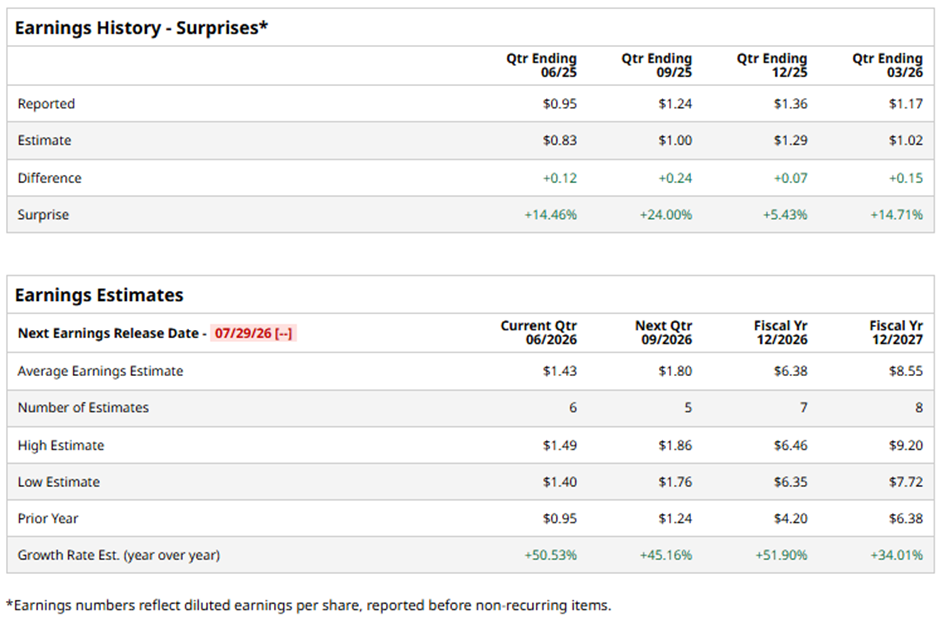

The Westerville, Ohio-based company is expected to release its fiscal Q2 2026 results soon. Ahead of the event, analysts project VRT to report an adjusted EPS of $1.43, a 50.5% surge from $0.95 in the year-ago quarter. The company has exceeded Wall Street's bottom-line estimates in each of the last four quarters.

For fiscal 2026, analysts forecast Vertiv to post adjusted EPS of $6.38, up 51.9% from $4.20 in fiscal 2025.

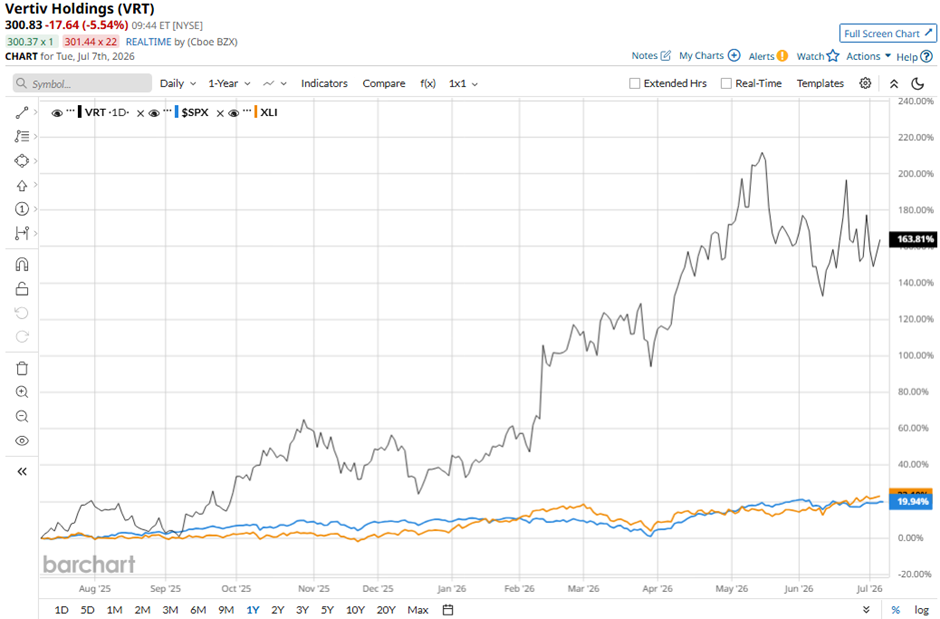

Shares of General Dynamics have increased 143.5% over the past 52 weeks, significantly outpacing the broader S&P 500 Index's ($SPX) 20% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 24.6% gain over the same period.

Shares of Vertiv fell 2.3% on Apr. 22 despite reporting strong Q1 2026 results, as investors focused on signs of slowing demand in the Europe, Middle East, and Africa (EMEA) region, where revenue declined 20.3% and organic sales dropped 29.4%, raising concerns about slowing demand and potential project delays. The market largely overlooked the company's solid performance, including adjusted EPS of $1.17, which exceeded consensus estimates, and net sales of $2.65 billion that met expectations.

Investor sentiment remained cautious despite Vertiv raising its full-year 2026 guidance to $13.5 billion - $14 billion in revenue and $6.30 - $6.40 in adjusted EPS.

Analysts' consensus view on VRT stock is bullish, with a "Strong Buy" rating overall. Among 25 analysts covering the stock, 18 suggest a "Strong Buy," two give a "Moderate Buy," and five provide a "Hold" rating. The average analyst price target is $363.04, suggesting a potential upside of 20.7% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)