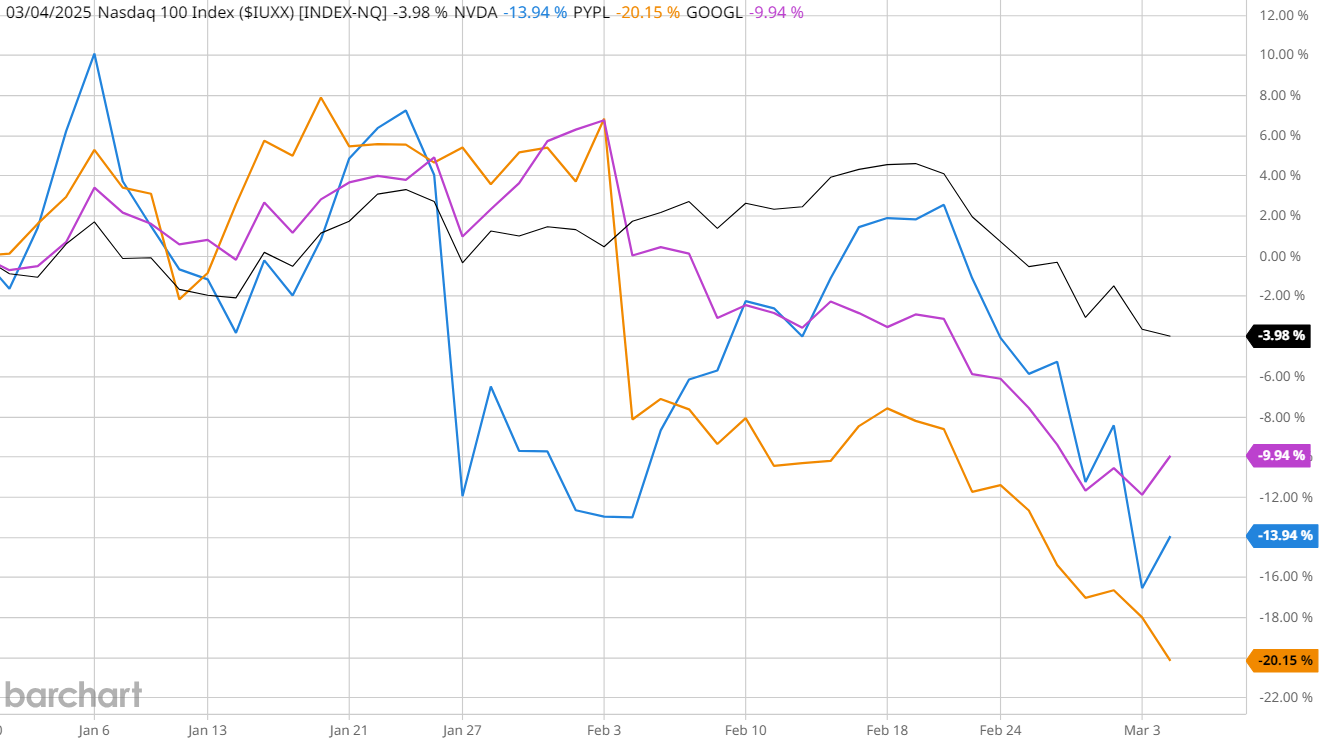

It’s been a rough stretch for U.S. stocks, with many leading names in the benchmark Nasdaq-100 Index ($IUXX) now down by 10% or more on a year-to-date basis. Investors have been tracking tariffs between the U.S. and key trade partners, which has added significant uncertainty to the forecast for top global corporations.

But with many mega-caps down big from their highs, is now a good time to buy the dip - or should investors continue to play it safe for now? Here’s a look at a few of the leading Nasdaq stocks worth a closer look after their recent pullbacks.

#1. Nvidia (NVDA), down -13.65% YTD

Investors should consider the recent dip in NVIDIA stock as a potential buying opportunity, albeit with careful consideration of the risks involved. The company's current stock price of $115.99 represents a significant 24% pullback from recent highs, primarily driven by geopolitical tensions and regulatory concerns rather than fundamental business issues.

NVIDIA's impressive financial metrics, including a robust profit margin of 55.85% and exceptional return on equity of 112.33%, demonstrate the fabless semiconductor company's operational excellence and market leadership.

Forward-looking earnings estimates show consistent growth expectations, with analysts projecting EPS to increase from $4.14 in FY2026 to $5.12 in FY2027, indicating strong future earnings potential. And while NVIDIA's dominant position in the AI chip market and its record-breaking data center revenue growth of 93% year-over-year could easily command a rich premium, that’s not the case right now.

"After yesterday's rout, the stock trades at ~25x NTM (next twelve months) earnings, their weakest level in a year and close to 10 year lows," wrote Bernstein's Stacy Rasgon in a note today. “In fact, the stock now trades BELOW parity relative to the SOX (something we have seen only once or twice in the past decade) and at only a slight S&P premium, the lowest they have been since 2016.”

Nvidia's expanding automotive segment, projected to grow from $1.7 billion to $5 billion this fiscal year, provides an additional growth catalyst beyond its core AI business. However, investors should be mindful of near-term headwinds, including potential impacts from new tariffs and ongoing investigations into chip exports to China, which could create additional volatility.

Given NVIDIA's strong fundamentals, market leadership in AI, multiple growth drivers, and positive analyst sentiment, the current dip presents an attractive entry point for long-term investors who can tolerate short-term volatility and geopolitical risks. For risk management, investors might consider dollar-cost averaging into the position rather than making a single large investment, given the current market uncertainties and the stock's historically high volatility.

#2. PayPal (PYPL), down -20.94% YTD

PayPal stock is down nearly 28% from its December highs, and is now valued at a reasonable forward price-to-earnings (P/E) ratio of 13.84 - a discount of roughly 50% to its historical averages.

The company's financial metrics appear solid, with a healthy profit margin of 13.04%. PayPal's return on equity (ROE) of 23.67% demonstrates strong operational efficiency and effective use of shareholders' capital, while its return on assets (ROA) of 5.83% indicates decent profitability relative to its asset base.

The company's transformation under CEO Alex Chriss, including the launch of PayPal Open and ambitious plans to accelerate adjusted EPS growth, presents a compelling turnaround story. The focus on Venmo monetization, targeting $2 billion in revenue by 2027, and expansion into new market opportunities could provide significant growth catalysts.

However, investors should be aware that PayPal faces intense competition in the digital payments space and must execute flawlessly on its strategic initiatives to achieve its ambitious growth targets. The stock's current price point, combined with analysts' average price target of $93.11 (suggesting 37.9% upside potential), presents an attractive entry point for long-term investors willing to weather potential short-term volatility.

As with NVDA, risk-conscious investors may find it prudent to consider dollar-cost averaging into the position rather than making a large single investment, given the ongoing market uncertainties and the company's transformation phase.

#3. Alphabet (GOOG) (GOOGL), down -9.7% YTD

Based on the comprehensive analysis of Alphabet, the current dip presents an attractive buying opportunity for long-term investors. The company's strong fundamentals are evident in its impressive profit margin of 28.6% and return on equity of 32.48%, indicating efficient operations and effective use of shareholder capital.

Trading at a forward P/E ratio of 18.59, GOOGL appears reasonably valued compared to other tech giants, especially considering its market leadership position and growth potential. The company's robust financial health is further demonstrated by its healthy balance sheet, with more cash than debt, providing flexibility for continued investments in AI and other growth initiatives.

Wall Street analysts maintain a highly bullish stance on GOOGL, with an impressive consensus rating of “Strong Buy,” suggesting strong conviction in the company's future prospects.

While the recent 17.5% decline from all-time highs has concerned some investors, this correction appears to be primarily driven by broader market sentiment rather than company-specific issues, as Alphabet continues to deliver solid revenue growth across its core businesses.

The company's aggressive $75 billion capital expenditure plan for 2025 initially weighed on the stock, but demonstrates management's commitment to maintaining leadership in AI and quantum computing, which should drive long-term value creation. Recent innovations, including the launch of Gemini Code Assist and the Willow quantum computing chip, showcase Alphabet's continued technological advancement and competitive edge in emerging technologies.

Despite near-term challenges like the Chegg (CHGG) lawsuit and minor workforce adjustments, the company's core business remains exceptionally strong, with impressive growth in both Search and YouTube advertising, as well as a 30% expansion in its Cloud division.

Given these factors, along with the current price representing a significant discount from recent highs, investors should view this dip as an opportunity to accumulate shares in a world-class company that's well-positioned to benefit from long-term trends in digital advertising, cloud computing, and artificial intelligence.

/Facebook-you've%20been%20Zucked%20by%20Annie%20Spratt%20via%20Unsplash.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)