With a market cap of $12.4 billion, Pentair plc (PNR) is a global water solutions company that develops and supplies products and systems for fluid treatment, water filtration, and pool management across regions including the United States, Europe, China, Latin America, and Australia. Through its Flow, Water Solutions, and Pool segments, the company offers a broad portfolio of pumps, filtration systems, water treatment products, and pool equipment under multiple well-known brands.

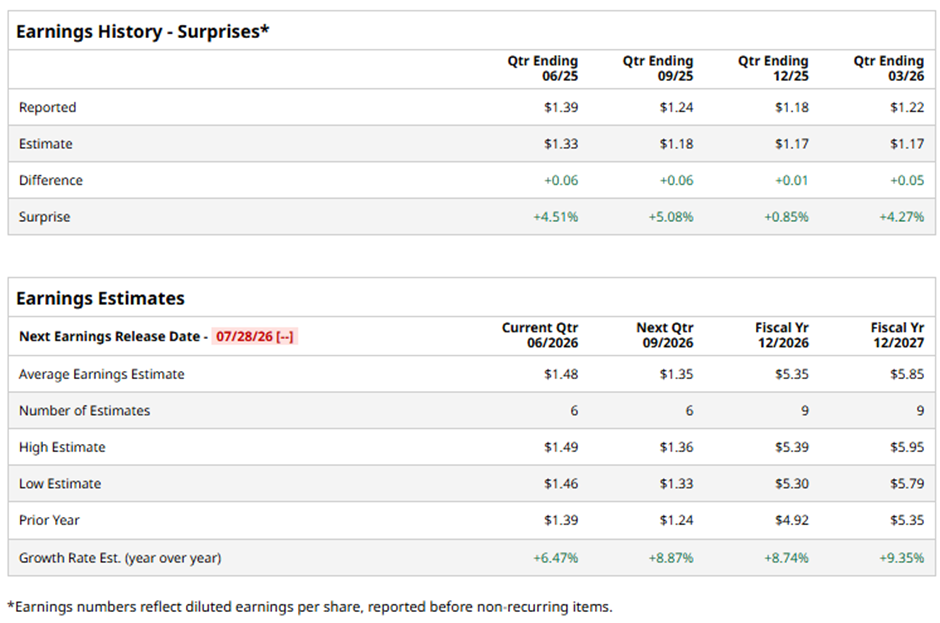

The London-based company is expected to release its fiscal Q2 2026 results soon. Ahead of the event, analysts project PNR to report an adjusted EPS of $1.48, a 6.5% rise from $1.39 in the year-ago quarter. The company has exceeded Wall Street's bottom-line estimates in each of the last four quarters.

For fiscal 2026, analysts forecast Pentair to post adjusted EPS of $5.35, up 8.7% from $4.92 in fiscal 2025. Moreover, adjusted EPS is expected to grow 9.4% year-over-year to $5.85 in fiscal 2027.

Shares of Pentair have decreased 27.5% over the past 52 weeks, underperforming the broader S&P 500 Index's ($SPX) 20.2% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 24.1% gain over the same period.

Shares of Pentair tumbled 10.2% on Apr. 28 despite reporting solid Q1 2026 results as investors were disappointed by the company’s cautious outlook and weak cash flow trends. Although Pentair posted sales of $1.037 billion (up 3%), adjusted EPS of $1.22 (up 10%), and expanded adjusted ROS by 100 basis points to 25.0%, management said its full-year forecast assumes “limited to no U.S. residential recovery,” signaling continued softness in an important end market.

Investors were also concerned that operating cash flow worsened to negative $67 million versus negative $39 million a year earlier, while free cash flow declined to negative $86 million from negative $56 million, overshadowing the company’s updated full-year adjusted EPS guidance of $5.30 - $5.40.

Analysts' consensus view on PNR stock is cautiously optimistic, with an overall "Moderate Buy" rating. Among 20 analysts covering the stock, 11 suggest a "Strong Buy," two "Moderate Buys," four give a "Hold," one has a "Moderate Sell," and two provide a "Strong Sell" rating. The average analyst price target is $101.26, suggesting a potential upside of nearly 32% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)