Synchrony Financial (SYF) is a leading consumer financial services company that provides a broad range of credit and banking products to individuals and businesses across the United States. Headquartered in Stamford, the company partners with many of the nation's leading retailers, healthcare providers, and other businesses to offer financing solutions that support consumer spending and business growth. Through its digital banking platform and consumer lending offerings, Synchrony serves millions of customers while maintaining a strong presence in retail commerce and financial services.

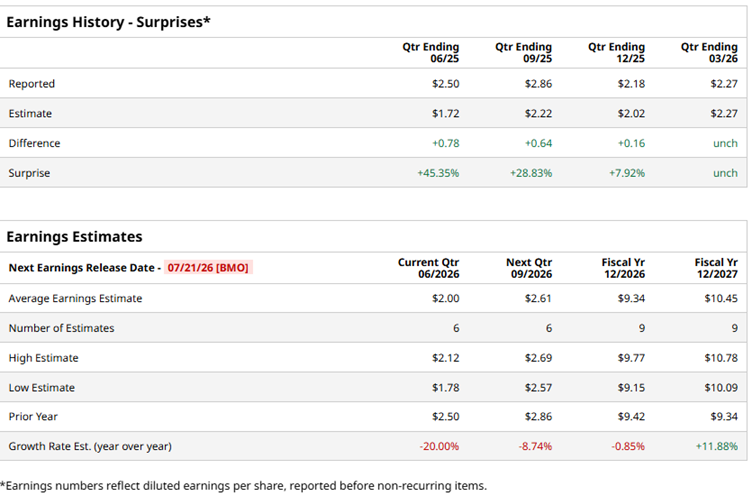

Currently valued at approximately $25.68 billion, Synchrony is scheduled to report its fiscal 2026 second-quarter results before the market opens on Tuesday, July 21. Ahead of the release, Wall Street expects the consumer financial services company to post earnings of $2.00 per share, marking a 20% decline from the year-ago quarter. Even so, Synchrony has demonstrated consistent execution, having met or exceeded analysts' earnings estimates in each of the last four quarters.

Looking beyond the upcoming report, analysts forecast full-year fiscal 2026 EPS of $9.34, representing a slight decline from the previous year. Earnings are then expected to return to growth in fiscal 2027, with EPS projected to climb 11.9% year over year to $10.45 per share.

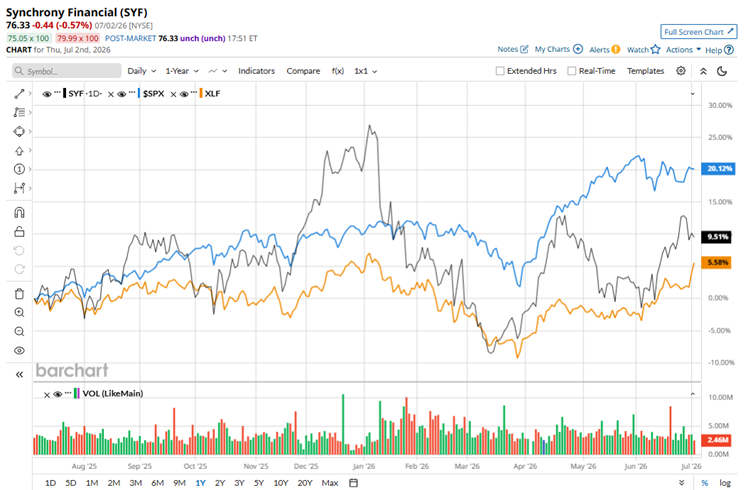

Synchrony's shares have delivered respectable gains over the past year, though they have trailed the broader market's rally. The stock has advanced 9.9% over the past 12 months, falling short of the S&P 500 Index's ($SPX) 20.2% return. However, it has comfortably outperformed its sector benchmark, with the State Street Financial Select Sector SPDR ETF (XLF) gaining just 5.7% over the same period, highlighting the company's relative strength within the financial sector.

Synchrony delivered a strong start to fiscal 2026 when it reported first-quarter results on April 21, reflecting resilient earnings growth and improving credit trends. The consumer finance company posted GAAP EPS of $2.27, up from $1.89 in the year-ago quarter, matching Wall Street's expectations. The quarter was supported by a 4% increase in net interest income to $4.6 billion, which helped lift the net interest margin by 76 basis points to 15.5%.

The improvement was primarily driven by higher yields on loan receivables and lower funding costs tied to declining benchmark interest rates, partially offset by lower yields on the company's liquidity portfolio. Meanwhile, provision for credit losses declined by $156 million to $1.3 billion, largely reflecting lower net charge-offs, although the comparison was partially offset by a $97 million reserve release recorded in the prior-year period.

Wall Street remains constructive on Synchrony’s outlook. The stock carries a consensus "Moderate Buy" rating based on recommendations from 23 analysts, including 13 "Strong Buy" ratings, one "Moderate Buy" recommendation, and nine "Hold" calls. The average price target of $89.13 suggests the stock could gain 16.8% from its current level, indicating analysts see additional upside ahead.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)