Artificial intelligence is running into a very real problem that no one can code away. It needs far more electricity than the current system can comfortably provide. Goldman Sachs estimates AI could require 2X today’s global data center power, with the AI cloud market reaching $267 billion by 2030 and “neoclouds” taking more than $50 billion of that.

The extra demand does not live on a slide deck. Power shortages and slow grid hookups are already showing up as real obstacles, and they risk slowing parts of what many see as a trillion‑dollar AI boom. In this setting, being able to drop in fast, reliable onsite power suddenly becomes valuable.

Bloom Energy (BE) is trying to step into that role. The company has expanded its partnership with Brookfield Asset Management (BAM) into a $25 billion framework focused on financing rapid, fuel‑cell‑based power for AI infrastructure projects.

For Bloom, the stakes are clear. If AI really does push data center power needs to double, and the grid cannot keep pace, does this $25 billion Brookfield deal make Bloom a genuine go‑to name for solving the power crunch?

Bloom Energy’s Financials

Bloom Energy builds solid‑oxide fuel‑cell systems that give businesses, communities, and data centers their own onsite power and hydrogen, using fuels such as natural gas, biogas, and hydrogen. The company is based in San Jose, California and sells within the U.S. and overseas.

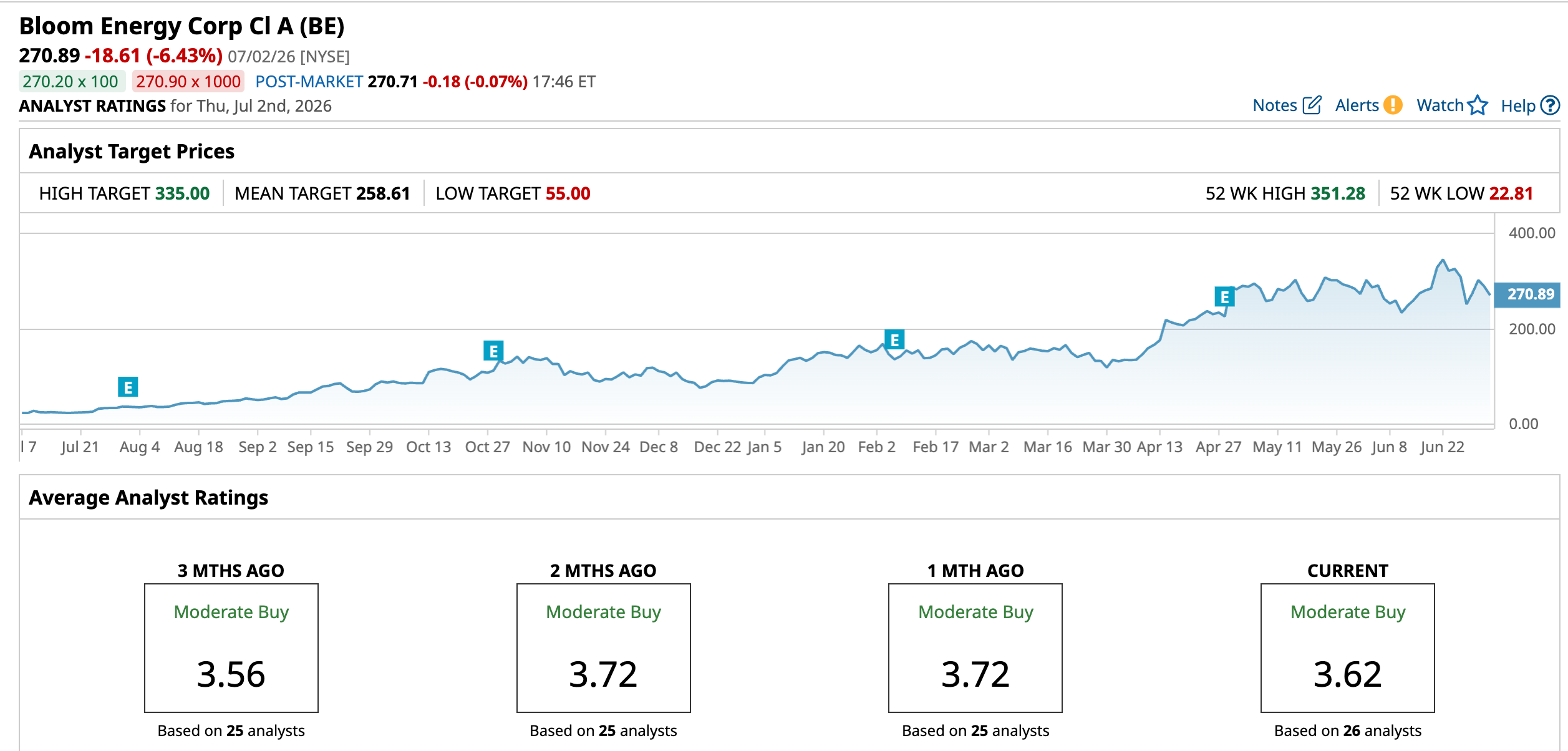

Currently, the year‑to‑date (YTD) gain is 211.76%, and the 52‑week move is 1,100.8%.

That kind of run shows up clearly in the valuation. Bloom’s market cap is $82.35 billion; its trailing price-to-earnings ratio is 253.95 times versus a sector median of 22.78 times, and its price-to-sales ratio is 29.94 times compared with a sector median of 1.99 times.

The latest quarter helps explain why expectations are this high. In the first quarter of calendar 2026, reported on April 28, revenue reached $751.1 million versus analyst estimates of $529 million, roughly 130% growth from the prior year’s $326 million.

It also reported adjusted EPS of $0.44 versus expectations of $0.13. The release detailed adjusted EBITDA of $143 million versus estimates of $54.08 million, equating to a +19% margin.

That same report noted a gross margin of 30.0% and a non‑GAAP gross margin of 31.5%, each up 2.8 percentage points year‑over‑year (YOY). BE also cited service gross margin rising to 13.3% and service non‑GAAP gross margin reaching 18.0%, both sharply higher than the prior year.

Bloom Energy disclosed operating income of $72.2 million and non‑GAAP operating income of $129.7 million. This is alongside a $73.6 million in cash flow from operating activities, pointing to an improvement of $184.3 million YOY.

Bloom Energy’s AI Deals

Bloom Energy’s latest deals show how its power systems are being plugged directly. Brookfield has agreed to expand its infrastructure partnership to a $25 billion financing framework, up from the original $5 billion set in October 2025.

This money is meant to fund specific projects that use Bloom’s fuel cells to power data centers, not general corporate borrowing. Through Brookfield’s wider AI‑focused fund, which is aiming for about $100 billion in total deployments, Bloom is effectively being positioned as an on-site power provider.

There is also help coming from the policy side. The Trump administration has highlighted Bloom’s fuel‑cell technology in its push to support U.S. energy security and deal with growing data center power needs. That kind of recognition links Bloom’s systems with federal goals for steady, cleaner power and can make it easier for the company to be considered on regulated or government-connected sites.

On the customer front, a bigger partnership with Oracle (ORCL) adds another clear piece. Oracle is planning to use up to 2.8 GW of Bloom fuel‑cell capacity to help power its data centers. That scale creates a multi‑year view of demand tied to one major enterprise and cloud provider, not just short‑term pilots.

All together, these agreements leave BE stock supported by specific partners, hard dollar figures, and defined gigawatt targets, rather than vague promises.

How Wall Street Is Now Pricing Bloom’s AI Ambitions Into BE

Earnings expectations for Bloom Energy have stepped up noticeably. The next earnings release is scheduled for July 30, and the current quarter for June 2026 carries an average EPS estimate of $0.20 versus a prior‑year figure of ‑$0.03. That implies a YOY growth rate of 766.67%.

For price targets, the tone is similar. Evercore ISI raised its price target on Bloom Energy to $295 from $179 and reiterated an “Outperform” rating. Barclays lifted its price target to $254 from $177 while maintaining an “Equal Weight” rating. These targets came following BE’s stronger‑than‑expected quarterly numbers.

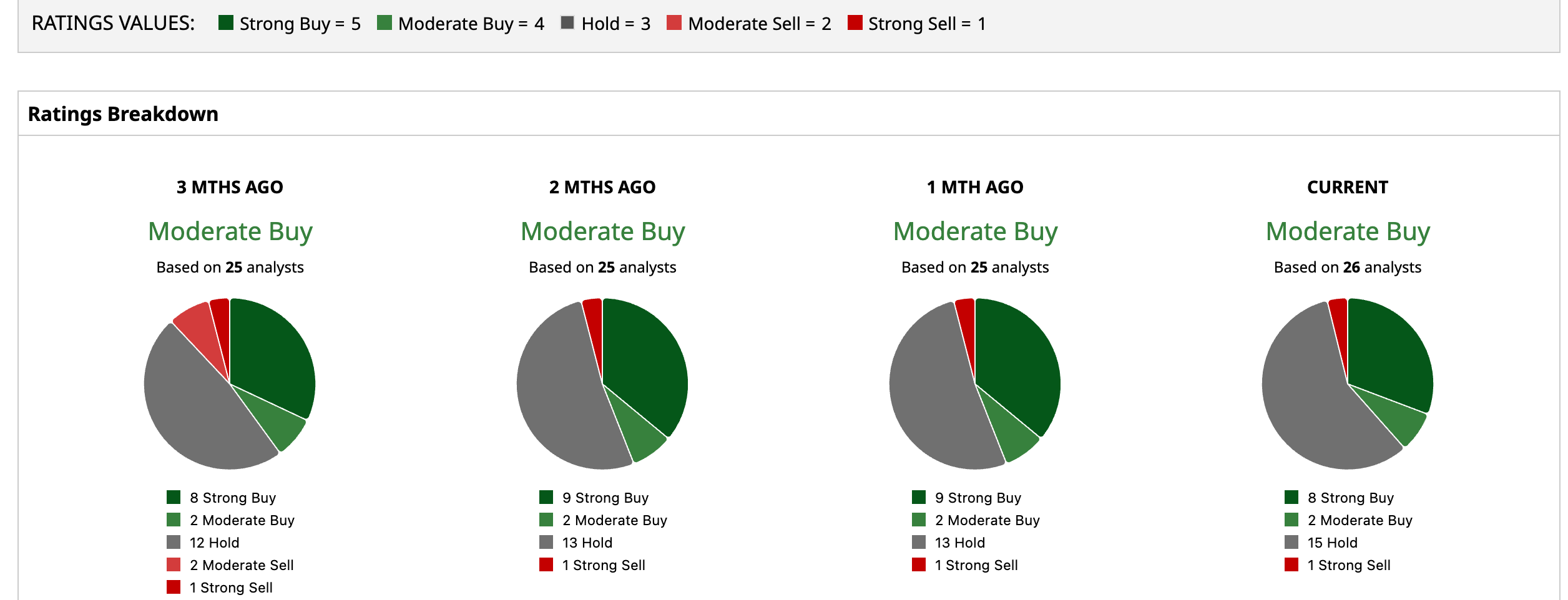

The broader view from analysts sits in the middle. Across 26 analysts, BE carries a “Moderate Buy” consensus rating, which leans positive without being unanimous. The average price target of $258.61 implies a 4.5% downside from the current price, but the Street-high price target of $335 shows the stock can climb 23.67% higher from here.

Conclusion

In the end, Bloom Energy’s $25 billion Brookfield framework, the Trump administration backing, and the Oracle 2.8 GW plan collectively put BE at the center of the AI power story rather than on the sidelines. That makes a gradual upside in the stock more likely than a deep, sustained drop, even if the pace of gains slows after the recent run. Where BE goes from here will largely hinge on whether those headline deals keep converting into visible revenue margin and cash flow in the coming quarters.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)