/Microchip%20Technology%2C%20Inc_%20microchip%20die%20extracted-by%20SweetBunFactory%20via%20iStock.jpg)

Headquartered in Eindhoven, the Netherlands, NXP Semiconductors N.V. (NXPI) designs and manufactures semiconductor products for automotive, industrial, mobile, and connected devices.

With a market cap of nearly $69 billion, NXP has built a broad portfolio that includes microcontrollers, processors, wireless connectivity solutions, analog and interface products, radio frequency devices, security controllers, and advanced sensors.

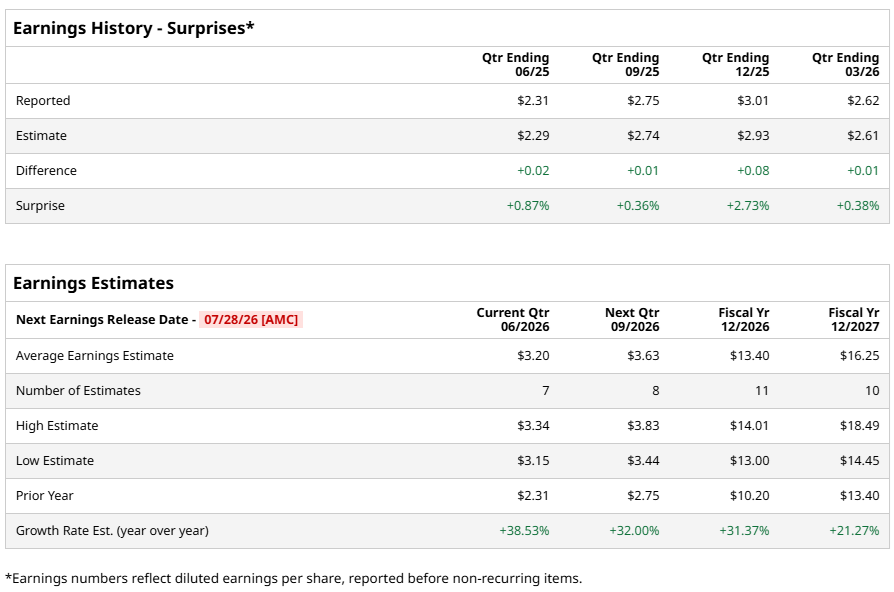

The company is scheduled to report its Q2 FY2026 earnings after the market closes on Tuesday, July 28. Wall Street expects diluted EPS of $3.20, representing a 38.5% jump from the $2.31 reported in the same quarter last year. NXP has also made a habit of clearing the earnings bar, having topped analysts' expectations in each of the last four quarters.

Furthermore, analysts expect full-year FY2026 diluted EPS to reach $13.40, reflecting a 31.4% year-over-year increase. They also see room for another leap in FY2027, with diluted EPS projected at $16.25, marking a 21.3% increase from the previous year.

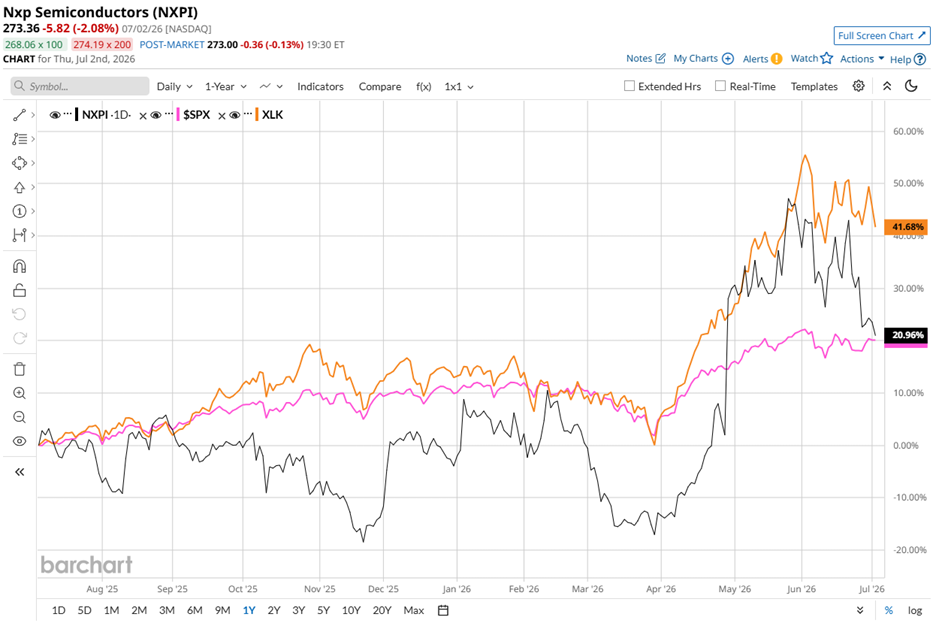

The stock has rewarded shareholders, although the race has not been one-sided. NXPI stock has gained 18.3% over the past 52 weeks, while the broader S&P 500 Index ($SPX) delivered a slightly stronger return of 20.2% during the same period.

This year tells a different story. NXPI stock has climbed 25.9% in 2026 so far, comfortably ahead of the benchmark index, which advanced 9.3%.

The technology sector, however, has moved at an even faster pace. The State Street Technology Select Sector SPDR ETF (XLK) surged 42.4% over the past 52 weeks. Even on a year-to-date basis, the fund has edged past NXP Semiconductors with a gain of 25.4%.

Much of the recent optimism stems from NXP Semiconductors' Q1 FY2026 performance. After the company reported Q1 results on April 28, investors wasted no time piling in, sending the stock up 25.6% in the very next trading session.

Revenue climbed 12.2% year over year to $3.18 billion, beating analysts' estimate of $3.16 billion. Adjusted EPS rose 15.5% from the year-ago level to $3.05, ahead of the Street’s estimate of $2.97. Strong demand from automotive customers, combined with solid performance in Industrial and Internet of Things, drove the strength, supported by new product launches.

Looking ahead, management expects Q2 FY2026 revenue between $3.35 billion and $3.55 billion, with a midpoint of $3.45 billion. They also project margins to continue expanding, supported by a favorable product mix and rising adoption of Software-as-a-Service, such as edge artificial intelligence (AI).

Wall Street remains firmly in NXP Semiconductors' corner. The stock carries an overall “Moderate Buy” rating. Out of 28 analysts covering the company, 18 recommend “Strong Buy,” two assign a “Moderate Buy,” seven maintain “Hold,” while one analyst continues to rate the stock “Strong Sell.”

Price targets also suggest analysts see more room to run. The average price target of $310.19 represents potential upside of 13.5%. Meanwhile, the Street-High target of $400 points to a possible gain of 46.3% from the current price level.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)