/Genuine%20Parts%20Co_%20parts%20by-%20kadmy%20via%20iStock.jpg)

Sometimes, the quiet performers deserve just as much attention as the headline grabbers. Genuine Parts Company (GPC) now finds itself in the spotlight as investors prepare for its next earnings report.

Headquartered in Atlanta, Georgia, the company distributes automotive and industrial replacement parts through an extensive network. With a market cap of nearly $18.2 billion, it supplies vehicle parts, tools, equipment, and maintenance products under the National Automotive Parts Association (NAPA) brand.

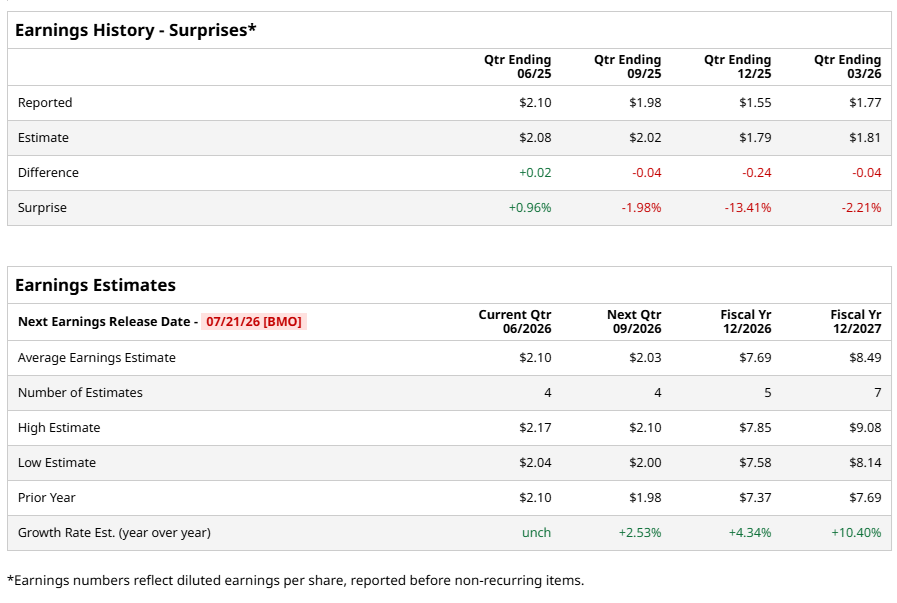

The next big checkpoint arrives before the opening bell on Tuesday, July 21, when Genuine Parts is scheduled to report its fiscal 2026 second-quarter results. Wall Street expects diluted EPS of $2.10, matching the $2.10 the company reported in the same quarter last year.

Even so, Genuine Parts still has something to prove, as it has beaten earnings estimates only once in the last four quarters. Looking beyond one quarter, analysts continue to see the company moving in the right direction.

They expect Genuine Parts to deliver full-year fiscal 2026 diluted EPS of $7.69, which represents a 4.3% increase from the previous year. Furthermore, analysts project fiscal 2027 diluted EPS of $8.47, reflecting another 10.4% year-over-year increase.

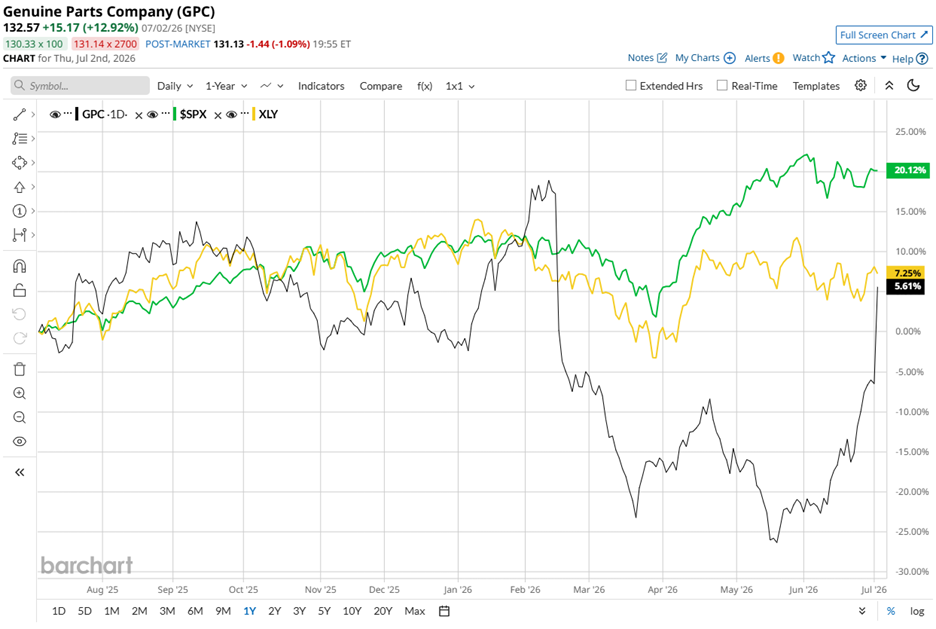

The stock, however, has taken a slower road. GPC stock climbed 4% over the past 52 weeks. The performance looks modest beside the broader S&P 500 Index ($SPX), which rallied 20.2% during the same period.

The gap narrows when the lens is shifted to 2026. GPC stock has advanced 7.8% year-to-date (YTD). The benchmark S&P 500 Index has still performed slightly better, with a 9.3% gain, although the difference looks far less dramatic than in the longer-term comparison.

The story changes once the company lines up against its own peers. The State Street Consumer Discretionary Select Sector SPDR ETF (XLY) returned 6.5% over the past 52 weeks. In 2026, the sector slipped 1.9%, while Genuine Parts moved in the opposite direction.

The resilience showed up clearly in the company's first quarter results announced on April 21. Strong execution across both the automotive and industrial businesses helped the company clear the bar on both revenue and earnings. Investors welcomed the update, sending the stock 2.1% higher on the day.

Revenue increased 6.8% year over year to $6.26 billion, ahead of analysts' estimate of $6.18 billion. Adjusted EPS reached $1.77, topping the Street’s estimate of $1.75. Additionally, the company reaffirmed its full-year 2026 guidance, now projecting total sales growth between 3% and 5.5% and adjusted diluted EPS of $7.50 to $8.00.

Wall Street has not thrown caution to the wind, although it continues to lean in the company's favor. Genuine Parts carries an overall “Moderate Buy” rating. Among 12 analysts covering the stock, five recommend “Strong Buy,” while seven suggest “Hold.”

Analysts have currently assigned the stock an average price target of $134, implying potential upside of 1.1%. Meanwhile, the Street-High target of $156 implies a possible 17.7% gain from the current share price.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)