Headquartered in Sunnyvale, California, Intuitive Surgical, Inc. (ISRG) builds robotic-assisted surgical systems along with precision medical technologies that help surgeons perform minimally invasive procedures.

Currently, commanding a market cap of approximately $142.5 billion, the company has earned its reputation through the da Vinci platform. It also provides advanced biopsy technology, surgical instruments, and hospital support services that help healthcare providers deliver more accurate and efficient patient care.

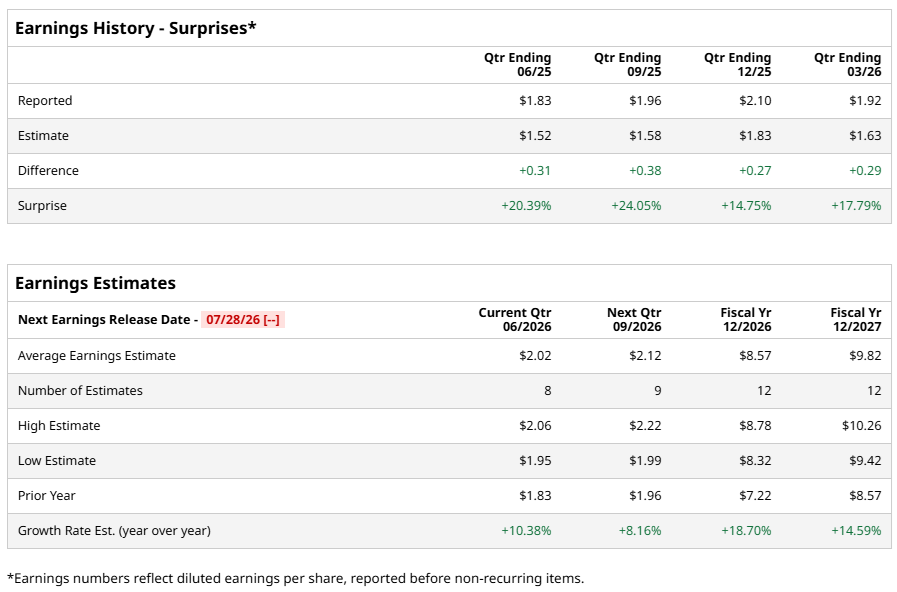

Investors now have their sights set on its fiscal 2026 second-quarter earnings report, scheduled to be released after the close on Thursday, July 16. Wall Street expects diluted EPS of $2.02, reflecting a 10.4% increase from the $1.83 the company reported in the same quarter last year. The company has also beaten earnings expectations in each of the last four quarters,

Analysts expect the momentum to continue. They project full-year FY2026 diluted EPS of $8.57, representing an 18.7% year-over-year increase. Expectations stretch even higher for FY2027, with diluted EPS forecasted to reach $9.82, marking a 14.6% jump from the previous year.

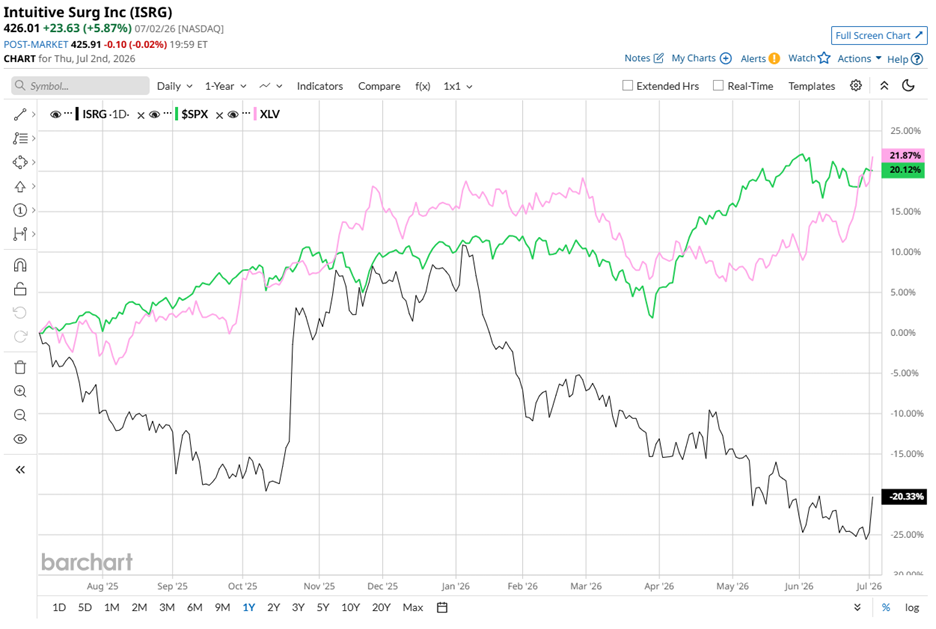

The share price, however, has marched to the beat of its own drum. ISRG stock slipped 21.2% over the past 52 weeks while the broader S&P 500 Index ($SPX) gained 20.2% during the same period. The pressure refused to let up in 2026, as ISRG stock dropped nearly 24.8% on a year-to-date (YTD) basis, while the benchmark index advanced 9.3%.

The healthcare sector paints a similar picture. The State Street Health Care Select Sector SPDR ETF (XLV) returned 21% over the past 52 weeks and added another 5.8% in 2026. Even with those gains, Intuitive Surgical found itself bringing up the rear.

Despite the rough stretch, investors changed their tune after the company's Q1 FY2026 earnings report. The stock jumped 7.2% on Wednesday, April 22, just one day after the results were released. Revenue climbed 23% year over year to $2.77 billion and topped analysts' expectations of $2.62 billion. Adjusted EPS rose 38.1% from the year-ago level to $2.50, sailing past the Street’s estimate of $2.11.

Management credited a 17% increase in total procedures to broad-based adoption of both the da Vinci and Ion platforms, as customers continued to expand minimally invasive care. The company also reported strong growth in after-hours procedures, non-urology procedures, and wider adoption of newer systems such as da Vinci 5. These factors pushed overall system utilization even higher.

Looking ahead, management projects worldwide da Vinci procedure growth of approximately 13.5% to 15.5% during FY2026. They also expect the non-GAAP gross profit margin to range between 67.5% and 68.5% of revenue in 2026.

Wall Street is backing the company despite the recent weakness in its share price. ISRG stock currently holds a “Moderate Buy” overall rating. Among 30 analysts covering the name, 19 rate the stock as a “Strong Buy,” two recommend a “Moderate Buy,” eight suggest a “Hold,” and one analyst assigns a “Strong Sell” rating.

To that end, the average price target stands at $572.41, implying potential upside of 34.4%. Meanwhile, the Street-High target of $750 implies a 76.1% gain from the current share price.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)