/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

Apple (AAPL) is once again betting on innovation. The tech giant has quietly acquired the team behind Play, the award-winning app that captured the 2025 Apple Design Award for Innovation, signaling Apple's continued focus on enhancing its developer and design ecosystem. According to a statement from the European Commission, Apple will “acquire certain assets from and have the right to offer employment to and hire certain employees of Rabbit 3 Times, Inc. d/b/a Play.” While the acquisition was completed in February, it only came to light recently after a mandatory four-month waiting period.

Before disappearing from the App Store, Play had built a loyal following as a sleek, easy-to-use prototyping platform that enabled designers to create rich, interactive app experiences using SwiftUI. With real-time collaboration across Mac and iPhone, the app simplified the process of designing, testing, and sharing app prototypes. As Apple folds this talented team into its ranks, could this strategic acquisition further strengthen Apple's long-term growth story, and is AAPL stock worth buying now?

About Apple Stock

Headquartered in Cupertino, Apple has grown into one of the world's most powerful and influential technology companies. Although iconic products such as the iPhone, Mac, Apple Watch, and AirPods have fueled its success, the company's greatest competitive advantage lies in the seamless ecosystem that connects them. By tightly integrating hardware, software, and services, Apple delivers a cohesive user experience that results in exceptional customer loyalty and encourages long-term engagement.

Today, Apple's business spans several of the world's fastest-growing technology markets, including smartphones, personal computing, digital content, and cloud-based services. At the same time, the company is expanding its footprint in emerging areas such as artificial intelligence, wearables, and mixed reality. This strategy underscores Apple's commitment to leveraging the strength of its ecosystem to unlock new growth opportunities while continuing to evolve beyond the products that first established its global leadership.

Even with a staggering market capitalization of $4.138 trillion, making it one of the world's most valuable companies, Apple's stock has delivered a relatively muted performance during the first half of 2026 compared to several of its mega-cap technology peers. While the shares have still outperformed the broader market, investor attention has increasingly shifted toward the company's slower-than-anticipated progress in AI and its growing reliance on external technologies, including Alphabet (GOOG) (GOOGL) Gemini platform, to strengthen its AI capabilities.

Despite concerns surrounding its AI strategy, Apple shares have still climbed 6.1% year-to-date (YTD), although that trails the S&P 500 Index's ($SPX) 9.45% gain during the same period. The stock's longer-term performance tells a much stronger story, soaring 40.58% over the past year and comfortably outperforming the broader market's 20.75% return. However, after hitting an all-time high of $317.40 on June 8, Apple has pulled back, with shares now trading 9.44% below its record peak.

A Look Inside Apple’s Q2 Financials

Apple reminded investors why it remains one of the world's most dominant technology companies with a blockbuster fiscal second-quarter 2026 earnings report released on April 30. The company delivered its strongest March quarter ever, handily beating Wall Street estimates and sending shares 3.24% higher in the next trading session. The standout performance was fueled by broad-based strength across Apple's business.

Total revenue climbed 17% year-over-year (YOY) to a record $111.2 billion, comfortably ahead of analysts' expectations of $109.48 billion, as strong demand for iPhones combined with another exceptional quarter for the company's high-margin Services segment. Leading the charge was the iPhone franchise, which generated $57 billion in revenue, a 22% increase from a year earlier. The launch of the iPhone 17 lineup, including the mid-cycle debut of the iPhone 17e, resonated strongly with consumers, while premium Pro models continued to enjoy robust demand.

Apple's Services business was equally impressive, reaching a new all-time high of $31 billion in quarterly revenue, up 17% from the prior year. Growth was driven by continued momentum across the App Store, Apple Music, iCloud, advertising, and cloud services, supported by Apple's expanding installed base, which has now surpassed 2.5 billion active devices worldwide.

Growth wasn't limited to Apple's flagship businesses. The launch of the M4-powered iPad Air helped lift iPad revenue by 8%, while Mac sales increased 5.7%, supported by the introduction of the MacBook Neo. Regionally, Greater China delivered one of the quarter's biggest surprises, with revenue soaring to $20.5 billion from $16 billion a year earlier, reinforcing its status as Apple's third-largest market behind the Americas and Europe.

The company's financial performance was equally impressive. Gross margin expanded to a record 49.3%, up from 47.1% a year ago, reflecting Apple's ability to drive both pricing power and operational efficiency. Earnings per share rose 21.8% to $2.01, comfortably topping the consensus estimate of $1.92. CFO Kevan Parekh also noted that Apple generated more than $28 billion in operating cash flow during the quarter, setting new March-quarter records for both cash flow and earnings per share.

Beyond its stellar operating performance, Apple continued to reward shareholders. The board authorized an additional $100 billion share repurchase program, signaling management's confidence in the company's long-term outlook. It also raised the quarterly dividend by 4% to $0.27 per share, extending Apple's long track record of returning significant capital to investors.

What Do Analysts Think About Apple Stock?

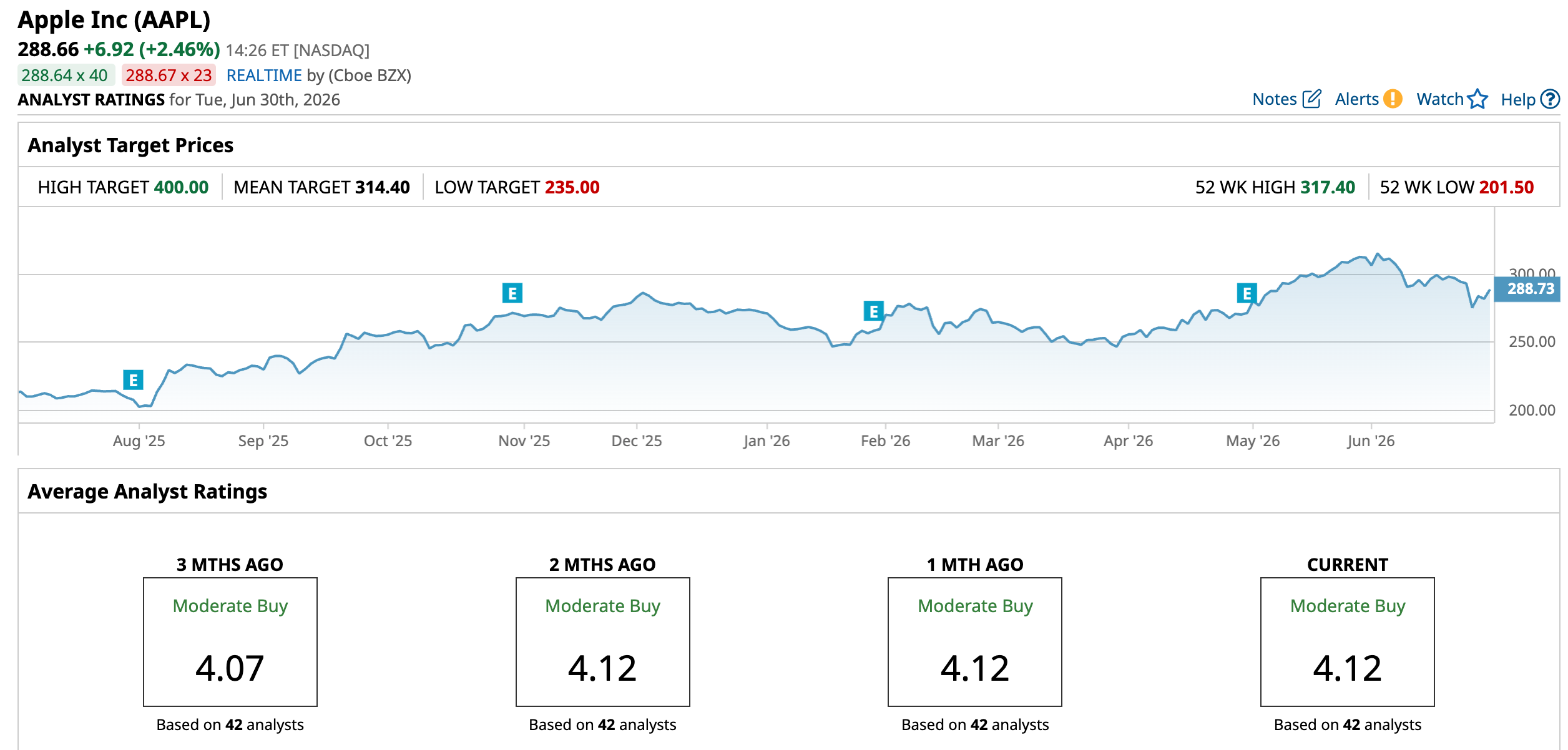

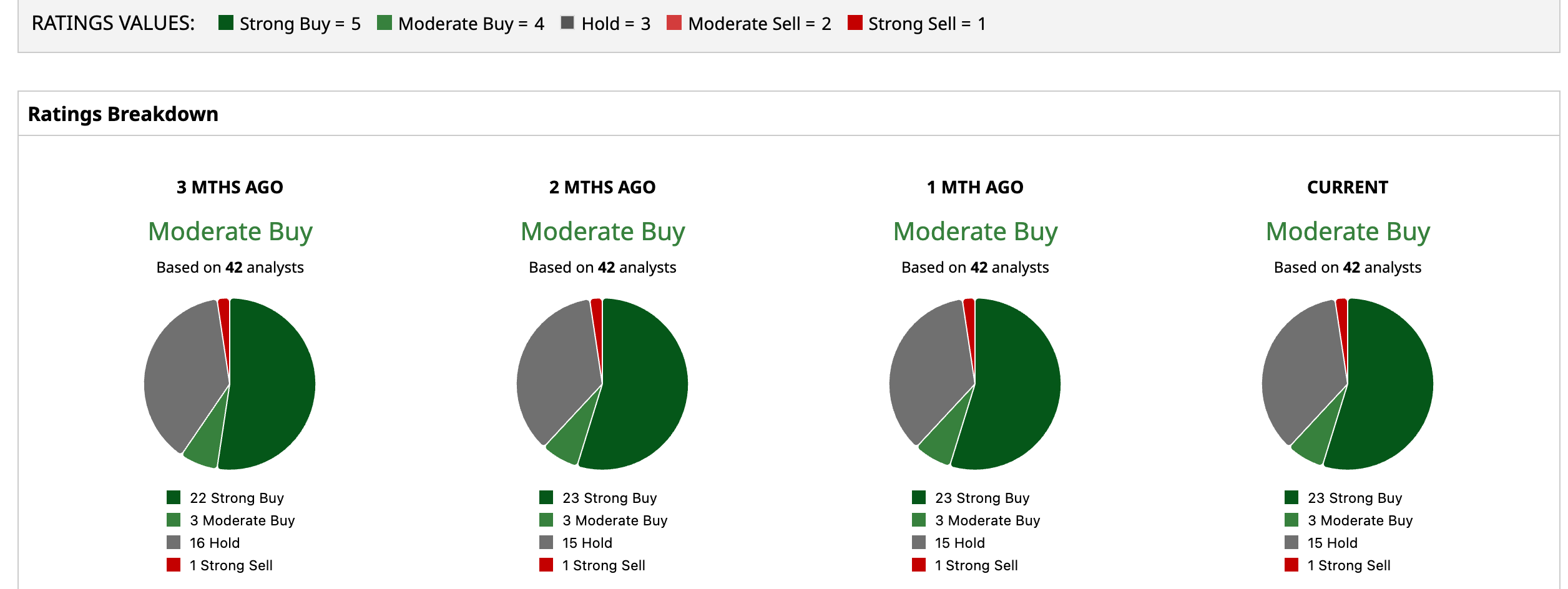

Overall, Wall Street continues to maintain a favorable view of Apple, with the stock earning a consensus "Moderate Buy" rating. Among the 42 analysts covering the company, 23 recommend a "Strong Buy," three rate it a "Moderate Buy," 15 advise investors to "Hold," and only one has a "Strong Sell" recommendation. Analysts also see further upside ahead, with the average price target of $314.40 implying a potential gain of 8.9%, while the Street-high target of $400 suggests the stock could rally as much as 38.6% from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)