The S&P 500 ($SPX) has put up a decent but unexciting 8% gain so far in 2026, with most of the heavy lifting coming from a few big names. Dividend stocks are quietly doing more, and Watsco (WSO) is a good example of that shift. WSO stock is up 22% year-to-date (YTD) and still offers a forward dividend yield above 3%.

The macro backdrop makes that combo even more interesting. The Federal Reserve is holding the federal funds rate in the 3.5% to 3.75% range. Meanwhile, officials under new Fed Chair Kevin Warsh are signaling that more hikes are possible as inflation remains sticky.

This environment tends to favor companies tied to essential replacement demand, and Watsco fits that description well. The natural next question is: What exactly allows this under‑the‑radar name to pull that off? Let’s dive in.

Watsco’s Dividend and Solid Numbers

Watsco is a Miami, Florida‑based distributor of heating, ventilation, air conditioning, and refrigeration equipment, supplying contractors in residential and commercial markets across the U.S. and abroad. The core of the business is steady replacement and upgrade demand, not one‑off projects.

The payout story is a big part of why WSO stock matters in 2026. The company's board approved a regular quarterly dividend of $3.30 per share in April. This represents a 10% increase and lifts the annual rate to $13.20, which works out to a forward yield of 3.29%.

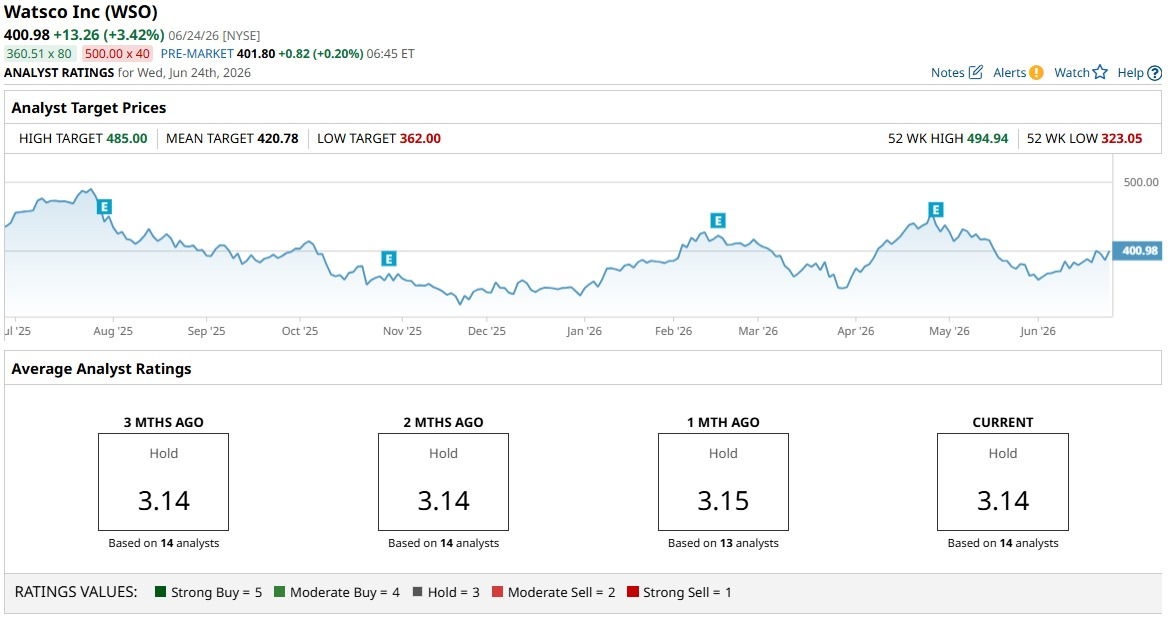

Watsco shares trade near $411 as of June 26, with a YTD gain of 22% and a decline of 5% in the past 52 weeks.

The company is valued at about $16.7 billion by market capitalization. WSO stock also trades at 33.2 times trailing earnings and 30 times cash flow versus sector medians of 22 times and 15 times, respectively, showing investors are paying a clear premium.

The latest earnings update for the March 2026 quarter helps explain that premium. Revenue came in at $1.53 billion versus the analyst estimate of $1.48 billion, essentially flat versus last year but still representing a 3.4% beat. That signals that Watsco is at least holding its ground on the top line.

The firm also delivered adjusted EPS of $1.87 against a $1.69 consensus estimate, a 10.7% upside surprise that points to solid cost control and margin discipline. The same report showed adjusted EBITDA of $129.3 million versus forecasts of $113.7 million, implying an 8.4% margin and confirming that profitability is tracking ahead of what analysts expected.

That performance kept the operating margin at 7.2%, roughly in line with the same quarter a year earlier, so earnings quality looks consistent rather than stretched. Net income of $79.07 million for the quarter was up more than 10% year-over-year (YOY), backing the case for a higher dividend and supporting WSO stock’s premium valuation.

Watsco also reported operating cash flow of -$18.9 million and net cash flow of -$40.6 million. Operating cash flow fell 103% sequentially from $569.6 million, while net cash flow still improved 56%, pointing to working-capital and timing effects.

A Strategic Expansion

Watsco is still leaning on its buy‑and‑build playbook to grow. The company recently closed the acquisition of Jackson Supply Company, a long‑time HVAC distributor founded in 1972 with $230 million in 2025 sales.

This deal brings 25 locations and about 5,000 contractor customers across key Sun Belt markets, including Texas, Arizona, Oklahoma, Louisiana, Mississippi, Alabama, and Tennessee. Those states rank among the fastest‑growing regions in the country and are heavy HVAC users.

Jackson Supply will keep its own name and existing management team. That approach preserves local culture and vendor ties, while giving the business access to Watsco’s technology, logistics, and purchasing scale.

This acquisition strengthens Watsco’s position in high‑growth markets and creates room to drive more organic sales and margin improvements over time.

Analysts Have Cautious Expectations

Earnings expectations for Watsco are more muted than the share price might suggest. The next earnings release is set for July 29, and the consensus EPS estimate for the June quarter stands at $4.29. That compares with $4.52 in the same quarter a year earlier, which works out to a 5% YOY decline.

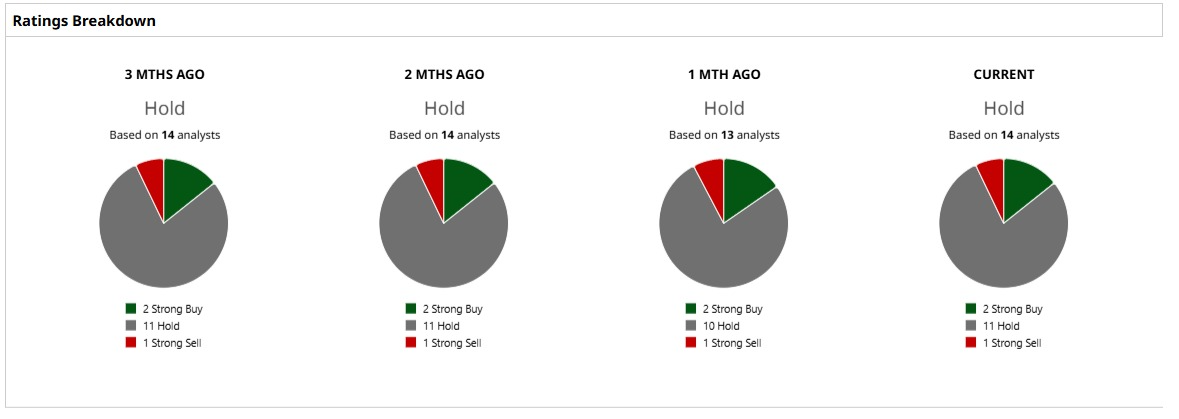

Analyst sentiment lines up with that cooler outlook. The consensus rating from 14 analysts is “Hold,” a neutral view rather than a strong buy or sell call. The average 12‑month price target for WSO stock is $420.80, implying about 2% potential upside from current levels.

Conclusion

Watsco looks more like a steady, dependable winner than a flashy short‑term trade. The business is growing earnings, backing a $13.20 annual dividend, and keeping the yield above 3%, while already beating the S&P 500 this year. Analyst estimates still call for slower near‑term growth and only modest upside from here, so the more likely path is a gradual move higher over time rather than another sudden jump.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)