/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

Nvidia (NVDA) stock has underperformed its peers so far this year despite dominating the artificial intelligence (AI) chip market. While shares of Advanced Micro Devices (AMD) have surged more than 150% and Intel (INTC) has rallied 256% in 2026, Nvidia stock has gained just 4.4%.

Although Nvidia has significantly underperformed its peers, the stock looks compelling on valuation, given the company's strong performance.

Nvidia continues to post exceptional revenue growth quarter after quarter despite tough comparisons. Moreover, strong demand, product innovation, and new avenues of growth strengthen its bull case.

In addition, Wall Street analysts have a consensus price target of $301.92 for NVDA stock, implying 54.7% upside potential over the next 12 months.

Nvidia’s AI Growth Story Remains Intact

Nvidia has strengthened its leadership in the AI infrastructure market, led by strong product demand and an expanding addressable market.

In the first quarter, Nvidia reported revenue of $82 billion, up 85% year-over-year (YOY) and 20% sequentially. Q1 was Nvidia’s third consecutive quarter of top-line growth acceleration. Further, Nvidia has reported sequential revenue growth for 14 consecutive quarters. This shows a strong demand for its products.

Nvidia’s data center segment is growing at a solid pace and remains the company's primary growth engine. In the data center business, revenue climbed 92% YOY to $75 billion, driven by continued investment from hyperscale cloud providers and leading AI developers. Within this segment, computing revenue rose 77% to $60 billion, while networking revenue nearly tripled to $15 billion, reflecting growing demand for high-speed interconnects that support increasingly large AI clusters.

Demand for Nvidia's next-generation Blackwell platform also remains robust. Its GB300 and NVL72 systems witnessed strong interest from hyperscalers and frontier AI developers seeking greater computing power for more sophisticated AI workloads.

Looking ahead, management expects the combined Blackwell and Rubin product families to generate around $1 trillion in cumulative revenue between 2025 and 2027. This outlook reflects that enterprise, cloud, and government spending on AI infrastructure are still in the early phases of a multi-year investment cycle.

Beyond GPUs, Nvidia is expanding into the CPU market through its upcoming Vera platform. As agentic AI drives demand for tightly integrated CPU-GPU architectures, the company sees an opportunity to participate in a CPU market worth an estimated $200 billion. Nearly all major hyperscale cloud providers and leading system manufacturers are already working with Nvidia to deploy Vera-based systems, with management expecting the CPU business to generate nearly $20 billion in revenue this year.

For the second quarter, Nvidia expects revenue of approximately $91 billion, indicating continued strong growth. With leadership across AI computing, networking, and now CPUs, Nvidia is evolving into a comprehensive AI infrastructure provider. As AI adoption accelerates globally, the company appears well-positioned to remain one of the biggest beneficiaries of the ongoing AI investment cycle.

Nvidia's Valuation Looks Attractive

Despite delivering explosive growth, Nvidia stock isn't trading at a premium. The stock currently trades at just 22.15 times forward price-to-earnings, a relatively modest valuation considering Wall Street expects earnings to surge 90.2% in fiscal 2027, followed by another 34.29% increase in fiscal 2028.

That makes Nvidia stand out against its competitors. AMD trades at a much higher 84.84 times forward price-to-earnings, while Intel's rally has driven its valuation higher at 202.55 times.

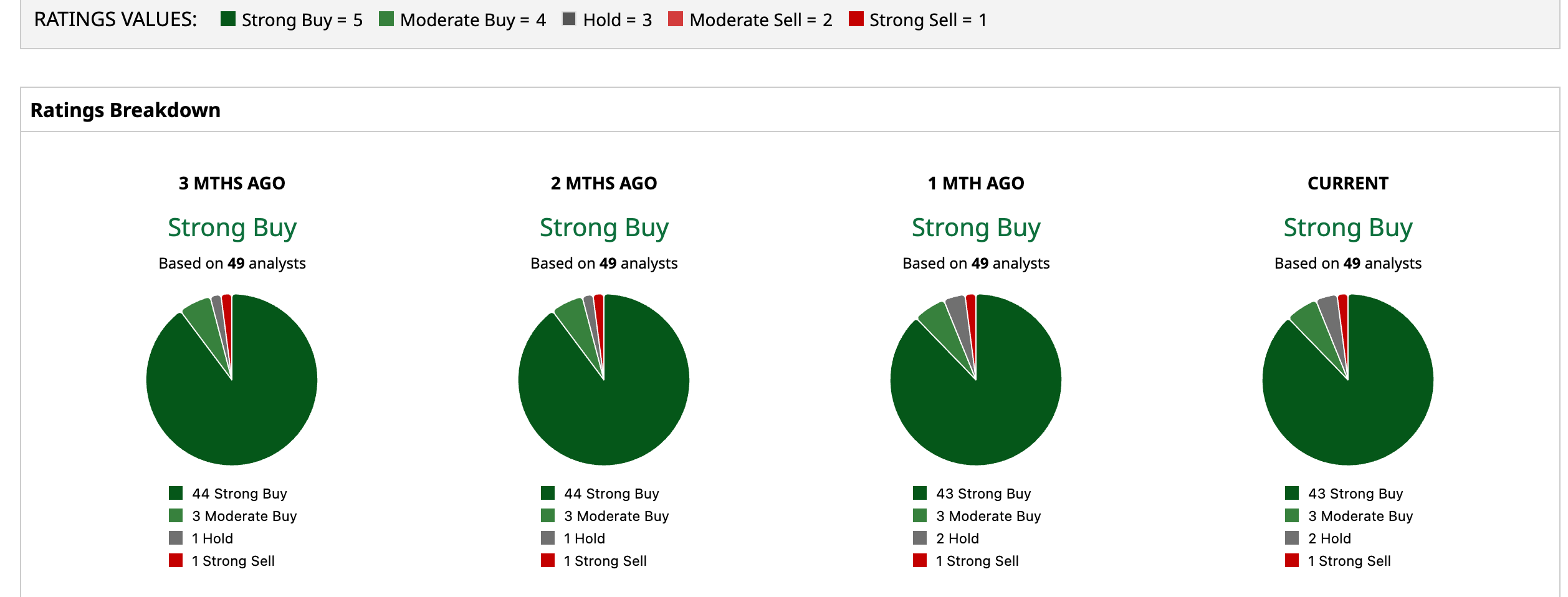

Nvidia Stock Is a Strong Buy

While Nvidia's muted stock performance in 2026 suggests that investor enthusiasm has shifted toward turnaround stories like Intel or alternatives such as AMD, the company's underlying fundamentals tell a different story. Nvidia continues to deliver industry-leading revenue growth, expand its AI ecosystem beyond GPUs, and capitalize on what remains a multi-year AI infrastructure buildout.

At the same time, its valuation looks attractive relative to both its growth trajectory and competitors. With analysts maintaining a “Strong Buy” consensus rating and projecting a 55% upside from current price levels, Nvidia appears to be a compelling investment.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)