Grain markets bulls are still on the ropes ahead of two big upcoming events that make up what is arguably the most important two-week trading stretch of the year. First comes Tuesday’s USDA planted acreage and quarterly grain stocks reports, which combined make one of the biggest USDA data releases of the year for the grains. Second, the calendar turns to July late this week, quickly followed by the U.S. Independence Day holiday. History shows that grain trading in the few days following the Fourth of July holiday can be pivotal and volatile, including potentially accelerating or reversing existing price trends.

Corn Crop Entering Key Pollination Stage of Growth

December corn (ZCZ26) on Friday fell 1 1/2 cents to $4.41 1/2 and for the week was down 2 1/2 cents. The beleaguered corn market bulls at least showed somewhat of a pulse late last week, despite Friday’s mild losses. Last Thursday’s technically bullish key reversal up on the daily bar chart in December corn is one clue that a market bottom is in place. Still, very good growing conditions over most of the Corn Belt will likely limit gains in the near term. However, corn traders are closely monitoring a heat dome that is presently enveloping the eastern Midwest right during the beginning of the key pollination stage for much of the U.S. corn crop. As of late Sunday, weather forecasters were predicting the heat dome would not last more than a few days. However, veteran grain traders know that weather patterns in the U.S. Midwest in the summertime can and do change rapidly.

Tuesday’s USDA planted acreage updates see growing trader notions that U.S. planted corn acres won’t be reduced much. The USDA quarterly grain stocks report Tuesday is expected to show U.S. corn supplies of 5.408 billion bushels, up 16.5% from a year earlier. This would represent the largest June 1 corn stocks since 1988. Traders will keep watching the weekly USDA crop progress report on Monday afternoon.

The closely followed annual Pro Farmer crop tour in late August will be a main late-growing-season market factor for corn. As the growing season progresses, there are concerns that excessive early season moisture could result in higher disease pressure later, especially if high temperatures arrive soon, though markets have given little weight to those worries so far.

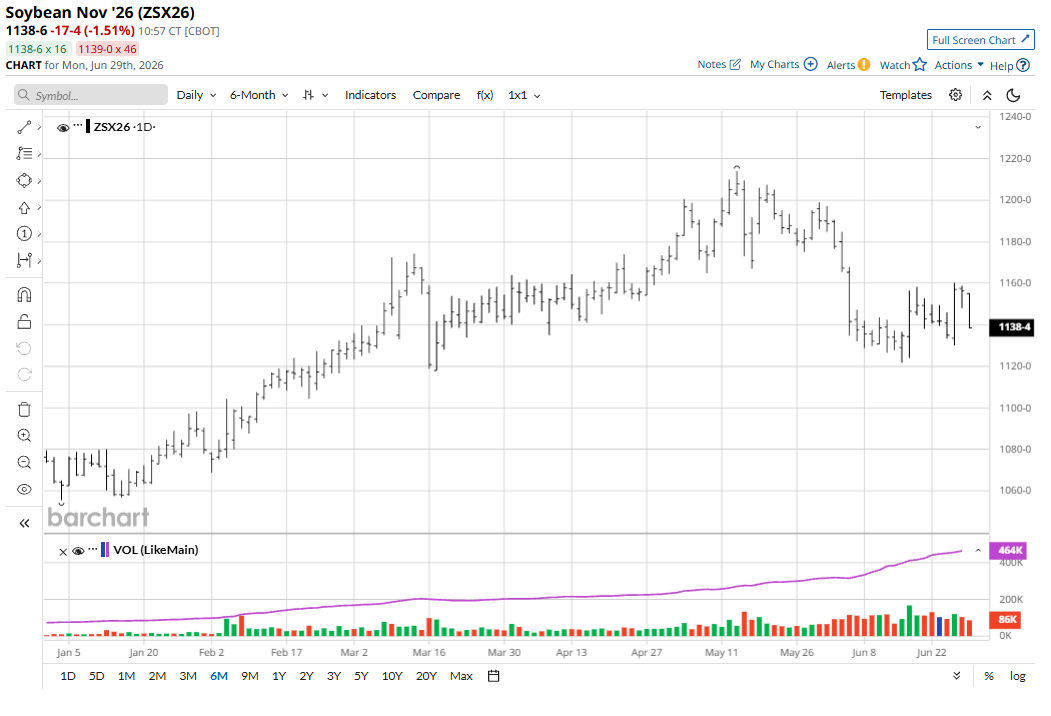

Soybean Bulls Showing Signs of Life, Too

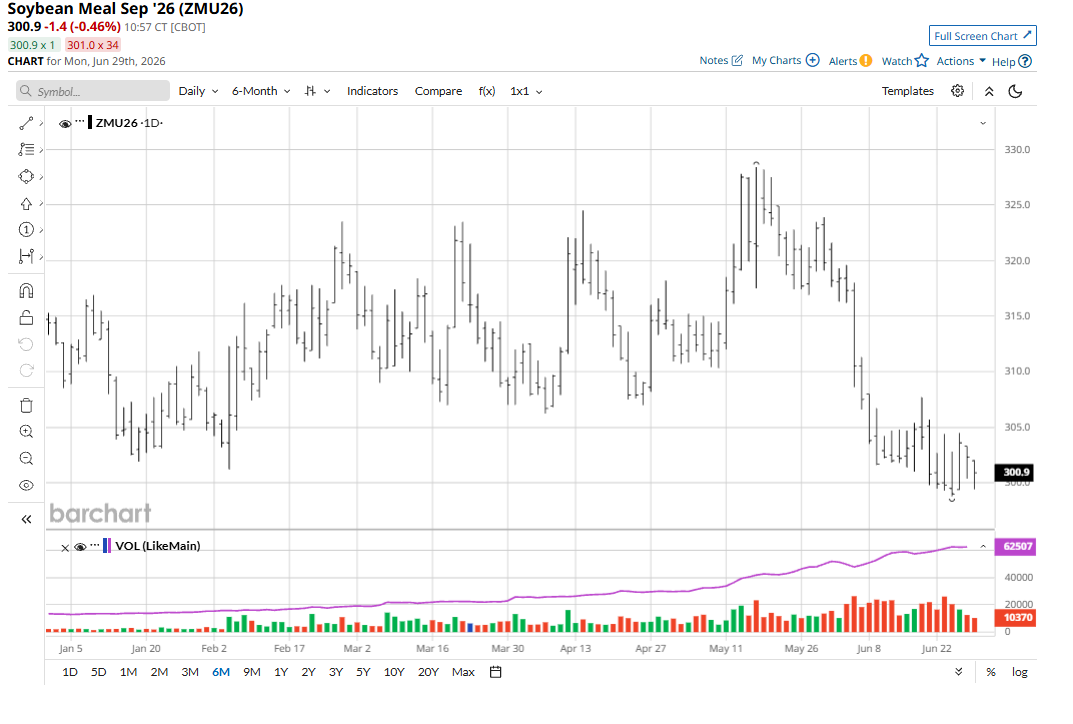

November soybeans (ZSX26) on Friday fell 3/4 cent to $11.56 1/4 but for the week were up 13 1/2 cents. The soybean bulls had a good week as they negated a price downtrend on the daily chart and are now working on a price uptrend. Worrisome for the bean bulls is the still-anemic soybean meal (ZMU26) futures market. Weather in the Midwest still leans price-bearish for the soy complex markets, but traders are closely monitoring the heat dome presently stationed over the Corn Belt and favoring the eastern half.

Tuesday’s USDA planted acreage update has traders expecting U.S. bean acres to be up slightly from the late-March estimate from the agency. The USDA quarterly grain stocks report is likely to show the average soybean stocks estimate of 1.046 million bushels, up 3.8% from a year ago. This would represent the largest June 1 soybean stocks since 2020.

August is arguably the most important growing month for most of the U.S. soybean crop. That means there is still time for a weather-market scare to pop up in soybeans. Focus will also be on the annual Pro Farmer crop tour that occurs in late August.

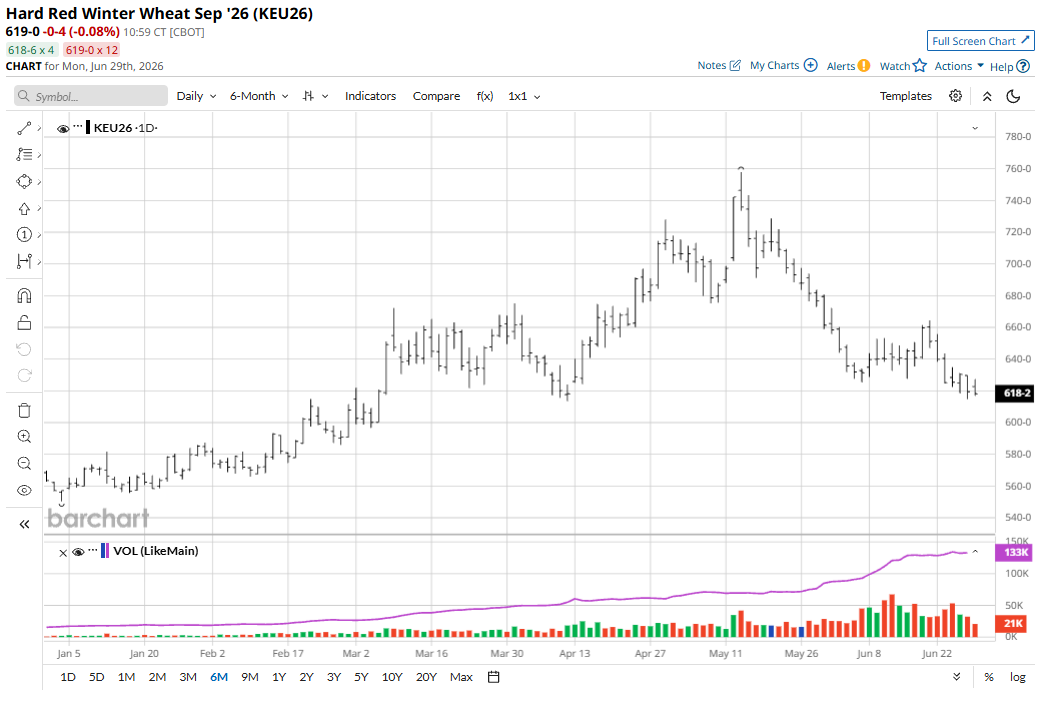

Winter Wheat Futures Markets Languishing

September soft red winter wheat (SRW) (ZWU26) futures on Friday fell 11 3/4 cents to $5.89 3/4 and for the week were down 24 1/4 cents. September hard red winter wheat (HRW) wheat (KEU26) futures lost 11 cents to $6.19 1/2, hit a 2.5-month low, and for the week were down 31 3/4 cents.

The winter wheat futures markets on Friday saw technically bearish weekly low closes, setting the table for some follow-through, chart-based selling pressure early this week. Harvest-related commercial hedge pressure is starting to weigh more heavily on the winter wheat futures markets.

Tuesday’s U.S. acreage and quarterly grain stocks reports from USDA are likely to show U.S. all wheat acres to be virtually unchanged from the late-March planting intentions report, according to a Reuters survey of analysts. For U.S. wheat stocks, the average estimate of 934 million bushels is up 9.3% from a year ago and would be the largest June 1 wheat stocks since 2020.

Monday afternoon’s weekly USDA crop progress reports and the U.S. winter wheat condition ratings will be closely scrutinized by wheat traders. The USDA is likely to release its final condition rating of the crop this week as harvest should eclipse the 50% complete threshold.

Wheat traders are closely monitoring a major heat wave in parts of Europe that has damaged crops there. Portions of France are too dry and hot, and rain is needed for spring crops. Winter grains are going to be too advanced to recover if and when rain falls, weather reports said.

U.S. winter wheat harvest is in full swing and will move north in the coming weeks. Harvest-season hedging pressure has a firm grip on winter wheat markets for now, with bullish supply concerns developing in Europe so far unable to offer any traction. That could change, however.

Tell me what you think. I read every one of your emails. My email address is jim@jimwyckoff.com. I enjoy getting feedback from all of you, my valued Barchart readers.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)