/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

CoreWeave's (CRWV) stock has lost momentum after an extraordinary rally earlier this year, declining more than 18% over the past week and more than 40% from its 52-week high. While the sharp pullback may appear to have created an attractive entry point, investors should think twice before rushing in.

The AI infrastructure provider's rally was driven by a string of major customer wins. During the first quarter, CoreWeave added Anthropic as a customer to support the development and deployment of its Claude family of AI models. The company also expanded its relationship with Meta (META), securing multiple new orders, including a previously announced $21 billion agreement.

CoreWeave’s partnerships with leading AI model developers and top AI companies significantly strengthen its competitive position and are expected to materially expand its contracted backlog, providing greater visibility into future revenue growth.

However, CoreWeave continues to pursue an aggressive expansion strategy that requires enormous capital investments, resulting in substantial cash burn and rising financial risk. Those concerns have weighed on investor sentiment despite the company's robust business momentum.

So, does the recent selloff present a compelling buying opportunity, or is the market correctly pricing in the risks? Here's what investors need to know.

CoreWeave Delivers Solid Q1, but Losses Continue to Mount

CoreWeave delivered another quarter of exceptional revenue growth, highlighting that demand for AI infrastructure remains robust despite growing concerns about the sustainability of AI spending. More importantly, the company's expanding customer base suggests its growth is becoming less dependent on a handful of customers.

In the first quarter, CoreWeave generated $2.1 billion in revenue, up 112% year-over-year (YoY) and 32% sequentially, driven by continued deployment of new computing capacity. Customer demand remained exceptionally strong, with the company signing more than $40 billion in new customer commitments during the quarter.

Those bookings lifted CoreWeave's contracted revenue backlog to $99.4 billion, representing nearly 50% sequential growth and almost four times the level reported a year ago. Importantly, 36% of that backlog is expected to be recognized within two years and 75% within four years, providing strong revenue visibility.

Customer quality also improved. Commitments from non-investment-grade AI startups and foundation model developers now account for less than 30% of the backlog, while new contracts continue to average roughly five years. The company now also has 10 customers with commitments exceeding $1 billion each, indicating that demand is becoming more diversified.

However, profitability remains a significant challenge. Adjusted net loss widened to $589 million from $150 million in the same quarter last year as CoreWeave continues investing aggressively to expand capacity.

Management also raised its full-year capital expenditure guidance to $31 billion to $35 billion, citing higher component costs. This indicates continued pressure on margins in the near term.

The Bottom Line: Here’s Why to Stay Cautious on CRWV Stock

CoreWeave continues to post impressive top-line growth, driven by a rapidly expanding backlog, new blue-chip customer wins, and deeper relationships with existing clients. Further, management stated that Q1 marked the low point for margins, with sequential improvement expected through the rest of the year.

Looking ahead, CoreWeave expects second-quarter revenue of $2.45 billion to $2.6 billion and raised its 2026 annualized revenue run-rate target to $18 billion-$19 billion. Management also reaffirmed its confidence in surpassing $30 billion in annualized revenue by the end of 2027, with more than 75% of that target already backed by signed contracts.

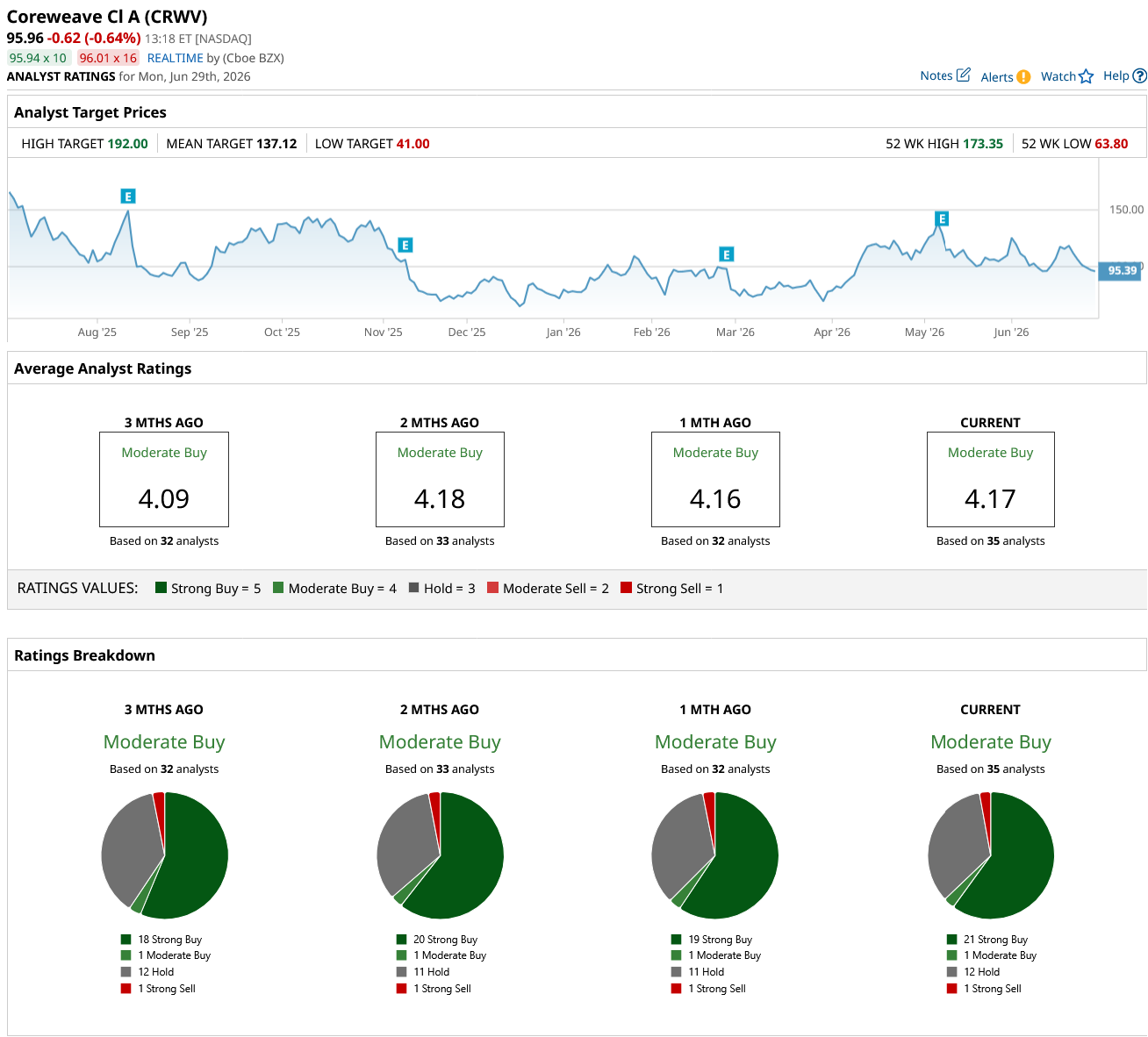

Wall Street analysts currently maintain a “Moderate Buy” consensus on CRWV stock. However, while its growth prospects remain impressive, massive capital expenditures, widening losses, and the potential for future dilution from capital raises continue to weigh on the stock, even as revenue grows rapidly.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)