/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Credo Technology (CRDO) is up 77.9% year-to-date (YTD). The last few days have been tough for investors, with the stock down nearly 12% so far this week. The volatility would scare investors, especially considering how the market could just collapse if memory demand alone stabilizes. If you’re a CRDO shareholder and were rethinking holding the stock, BNP Paribas provided exactly the reason to continue doing so.

BNP Paribas analyst Karl Ackermann recently maintained a positive outlook on Credo, expecting it to remain a key beneficiary of the AI infrastructure buildout. The analyst cited the adoption of Credo’s copper and optical connectivity solutions by hyperscalers as a reason for his bullish view. He noted that products such as Active LED cables and OmniConnect gearboxes have tripled Credo’s total addressable market (TAM) to over $10 billion in just 18 months. Ackermann further highlighted that Credo is involved with five of the six largest cloud computing companies, including Amazon (AMZN), Microsoft (MSFT), Meta (META), Oracle (ORCL), and xAI, a subsidiary of SpaceX (SPCX), stressing the firm’s growing importance in the AI supply chain.

Another significant point raised was the emerging Neocloud providers, estimated to account for 20% of Credo’s revenue over time. This aligns with CEO Bill Brennan’s confidence in the recent earnings call that Neocloud could approach 20% of the firm’s revenue. By fiscal 2027, the company is also expected to have three to four hyperscale firms making up 10% of revenue each. A more diversified customer base reflects a healthier position compared to being overly reliant on one firm, accounting for approximately 34% of Credo’s revenue last quarter.

The company also has exceptional supply chain visibility, with hyperscale customers providing Credo with demand forecasts 12 to 36 months in advance and placing orders three to six months ahead. The clear future revenue predictability is something that gives Credo a serious competitive advantage over its peers.

About Credo Stock

Founded in 2008 and headquartered in San Jose, California, Credo is a semiconductor company that provides high-speed connectivity solutions for AI data centre infrastructure. Its product portfolio includes Active Electrical Cables, digital signal processors (DSPs), and optical transceivers. The company serves hyperscale cloud providers, optical module manufacturers, and original equipment manufacturers.

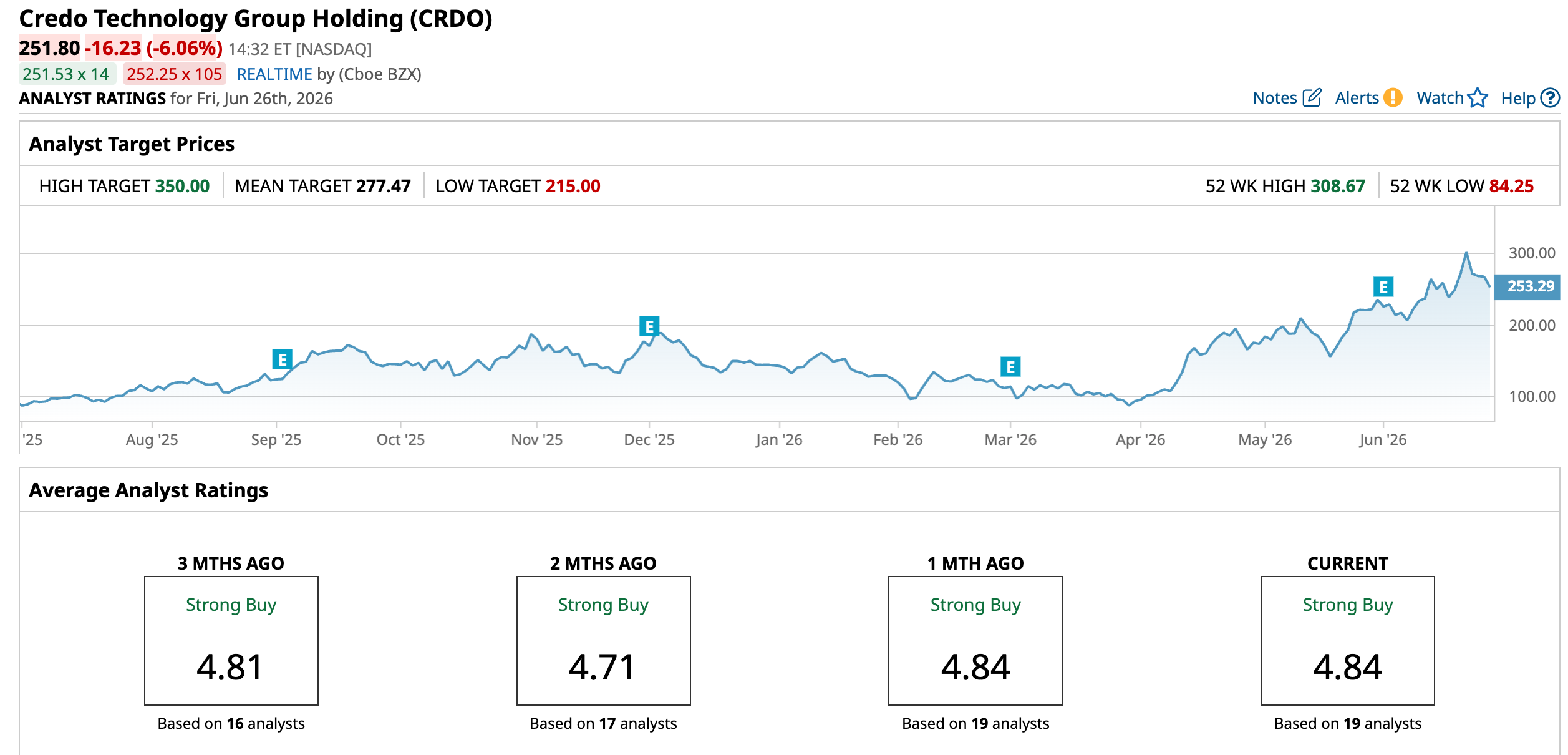

Over the last 12 months, Credo Technology’s stock has surged 169%, vastly outperforming the S&P 500 Index’s ($SPX) 20.1% gain during the same period. The rise has been driven by the extraordinary revenue growth due to accelerating demand for AI data center connectivity solutions. The stock recently hit its 52-week high after the DustPhotonics acquisition further strengthened investor confidence in the firm.

Credo’s valuation looks expensive by most traditional measures. The forward price-to-earnings GAAP of 55.63 times sits significantly above the sector median of 32.85 times. The price-to-sales ratio of 20.39 times makes the firm look even more overpriced, being more than six times the sector median of 3.27 times.

The EPS growth trajectory offers justification for the premium, with analysts expecting healthy growth of 77% and 46% in 2027 and 2028, respectively, and slowing down but still growing positively in the coming years.

The standout feature is the firm’s capital structure, with just $25 million in debt compared to $1.44 billion in cash despite spending $750 million on the DustPhotonics acquisition. For a high-growth semiconductor company with more than a $50 billion market cap, this is an exceptional balance sheet, which explains why Wall Street analysts expect investors to buy the company's stock despite trading at a premium.

Credo Records Another Stellar Year

Credo Technology reported its fourth-quarter fiscal 2026 earnings on June 1. The firm beat the analyst consensus on both key metrics. A record revenue of $437 million was reported, surpassing the $432 million consensus, and up 157% year-over-year (YOY). The fiscal 2026 revenue also more than tripled to over $1.3 billion. The non-GAAP EPS of $1.16 also comfortably beat the $1.03 consensus, representing a 231% YOY increase. The non-GAAP net income also increased more than 5 times to $662 million. The firm also reported a record free cash flow of $177.5 million and ended the quarter with $1.4 billion in cash. The CEO stated that fiscal 2026 marked another defining year for Credo.

For the next quarter, CFO Daniel Fleming stated that revenue of $465 million to $475 million and a gross margin of 67% to 69% is expected. While the company expects the first half growth to be modest, a significant inflection in the second half is expected due to optical products contributing to over $600 million in revenue, driving over 80% full-year revenue growth. CEO Brennan believes that the firm’s close relationship with its supply chain partners should help achieve the aggressive second-half ramp. He further mentioned that the fiscal 2027 scale-up revenue is just the beginning, with fiscal 2028 expected to be even more substantial, expressing confidence in the firm’s continued growth.

What Are Analysts Saying About Credo Stock

Stifel Nicolaus analyst Tore Svanberg increased Credo Technology’s price target from $250 to $350 while maintaining a “Buy” rating, following two days of meetings with Credo’s CEO and CFO. Stifel believes that the firm’s vertically integrated approach across copper and optical connectivity offers a competitive advantage over its peers. Similarly, Bank of America Securities analyst Vivek Arya also increased his price target from $252 to $340 while maintaining a “Buy” rating, following the strong Q4 results.

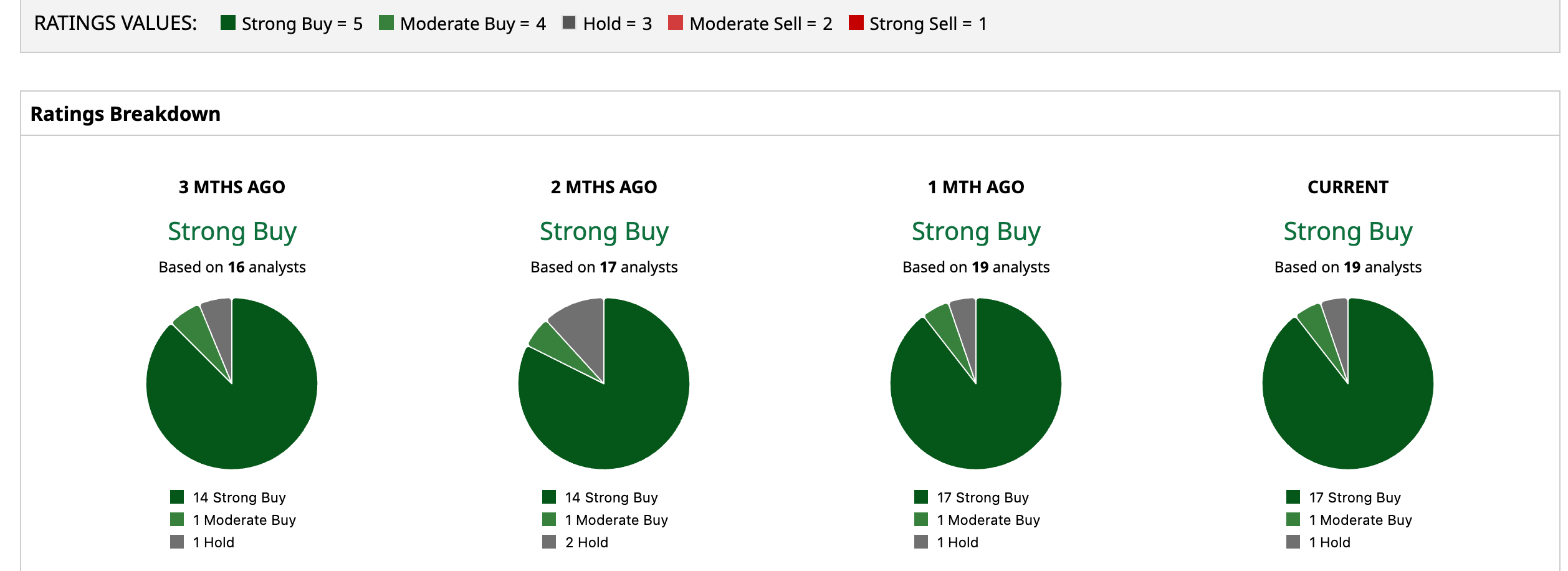

Based on the 19 Wall Street analysts, Credo Technology holds a “Strong Buy” rating, with the mean price target of $277.47 representing a possible upside of 10.2%. Further, the Street-high target price of $350 implies a climb of 39% for the stock over the next 12 months.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)