/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Commvault Systems (CVLT) is an enterprise cyber resilience and data protection company originally founded in 1988. Under CEO Sanjay Mirchandani, the company has pivoted from a legacy backup software provider into a cloud-native, AI-enabled unified resilience platform built for the ongoing agentic enterprise era. Commvault keeps customers ready by unifying data security, identity resilience, and cyber recovery on one platform, serving enterprises across hybrid, multi-cloud, SaaS, and on-premises environments.

Thoma Bravo has emerged as a potential buyer in recent weeks, with the private equity firm exploring options with Goldman Sachs (GS), adding a compelling M&A premium to an already strong fundamental growth story.

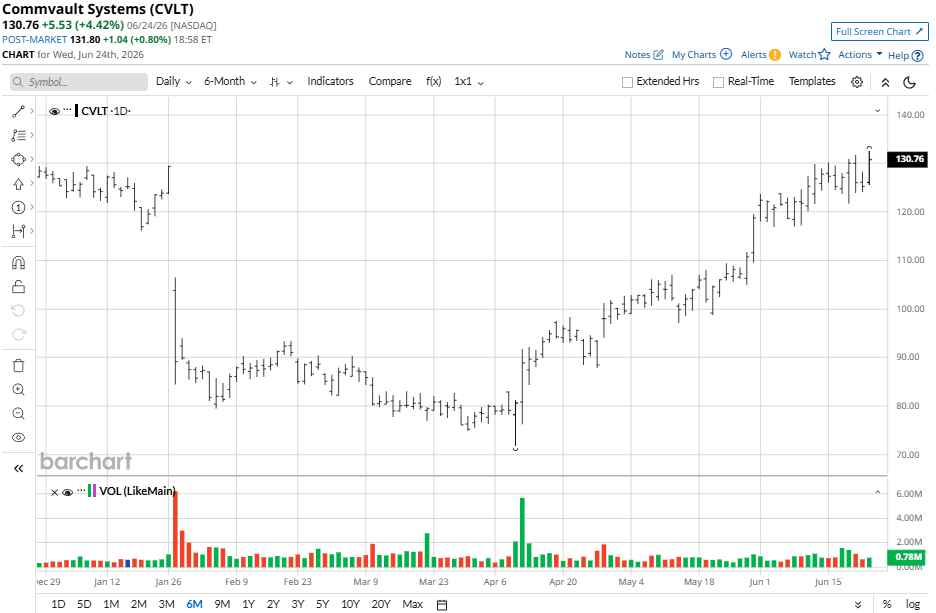

Commvault Is Recovering Lost Ground

Commvault stock’s 52-week range of $71.75 at the low end to $200.68 at the high end tells investors the story of how the stock peaked on AI cyber resilience momentum before suffering a brutal setback. CVLT stock plummeted 31% in a single session in January 2026 after an annual recurring revenue (ARR) mix shift disappointed investors, triggering a wave of securities class-action lawsuits and analyst price cuts.

Against the Nasdaq Composite’s ($NASX) 9% year-to-date (YTD) gain, CVLT stock is now fairly in-line with the broader market index, however. Recent Thoma Bravo takeover rumors and a Microsoft (MSFT) partnership are starting to reignite interest in the stock, with shares up 71% in the past three months.

Commvault Posts Mixed Results

Commvault reported its fourth-quarter results on April 28, 2026, posting revenue of $312 million and beating analyst estimates of $306.5 million. Adjusted EPS for the quarter came to $1.28, easily thumping past the $1.09 estimate set by analysts. SaaS revenue increased 43% year-over-year (YOY) to $93 million, subscription-based revenue climbed 20% to $208 million, while large enterprise segment revenue from transactions exceeding the $100,000 mark surged 9%, driven by an accelerating multi-product adoption cycle and higher deal volume.

Gross margin expanded to 81.8%, reflecting SaaS hosting efficiency, while 48% of SaaS customers now use more than one product from the company. Free cash flow for the quarter reached a record $132 million, with total ARR growth coming to 21% YOY to $1.12 billion. Identity-resilience and data-security ARR accounted for nearly 33% of the firm's net new ARR during the quarter.

Management is bullish for the ongoing quarter with guidance targeting 18% to 19% growth in subscription ARR, continued SaaS momentum, and strong capital returns, with AI and identity resilience identified as the primary market tailwinds. That's a forward-looking setup that management believes positions Commvault as the indispensable cyber-resilience partner for enterprises navigating an increasingly AI-driven and threat-rich digital landscape.

A Multiyear Deal With Microsoft

Commvault recently announced a multiyear strategic agreement with Microsoft (MSFT), strengthening its 25-year partnership. As per the agreement, Microsoft will offer Commvault's AI and cyber-resilience technologies as a native independent software vendor (ISV) service directly on Microsoft Azure, enabling Azure customers to seamlessly integrate Commvault's data recovery, application restoration, and identity-resilience capabilities without the need for complex third-party integrations.

The partnership effectively makes Commvault's cyber-resilience platform plug-and-play for Microsoft's vast enterprise customer base, a distribution advantage that could meaningfully accelerate ARR growth and SaaS adoption in fiscal 2027. CEO Sanjay Mirchandani described the deal as taking a 25-year partnership "to the next level," underscoring Commvault's ambition to become the default cyber-resilience layer across the Azure ecosystem.

How Should You Play CVLT Stock?

With the Microsoft Azure native ISV partnership transforming Commvault into a plug-and-play cyber-resilience solution for one of the world's largest enterprise cloud ecosystems, and Thoma Bravo takeover interest adding meaningful M&A optionality, the investment case for CVLT stock is more compelling than its share price suggests.

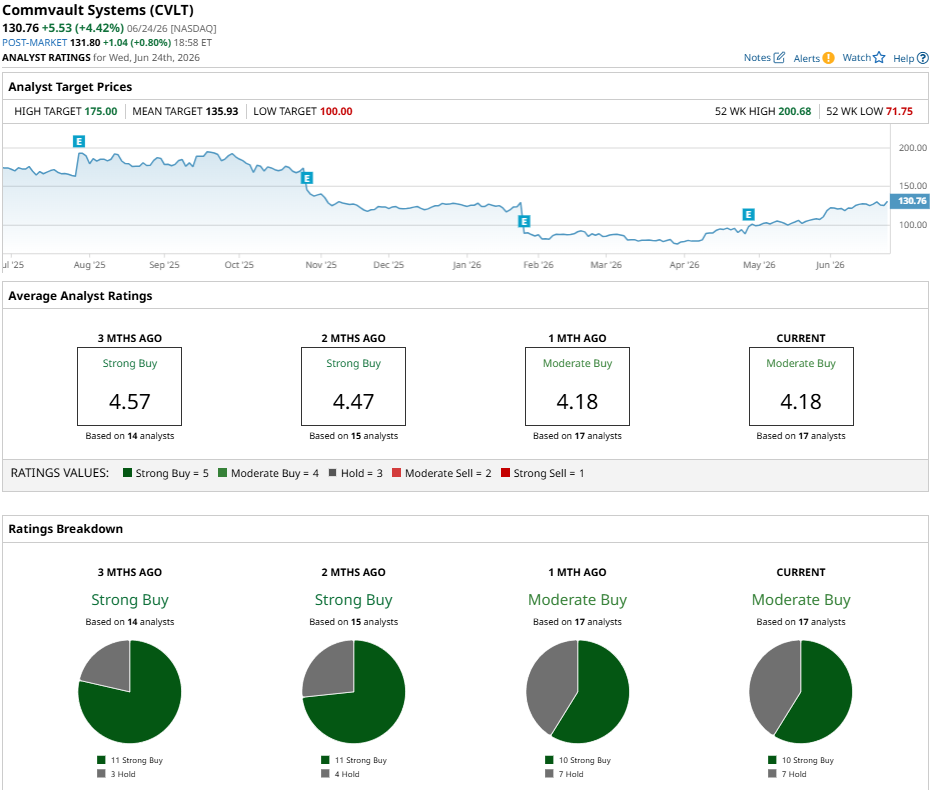

Wall Street's consensus rating stands at a "Moderate Buy" based on 17 analysts with coverage. That breaks down to 10 "Strong Buy" ratings and seven "Hold" ratings. The mean price target of $135.93 has already been surpassed, while the high target of $175 suggests potential upside of 27% from current levels. For contrarian investors, Commvault's early 2026 selloff may represent one of the most attractive entry points in the AI cybersecurity space today.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)