The tech sector took a hit on June 22, 2026. The Nasdaq 100 ($IUXX) dropped 3.29%, while the iShares Semiconductor ETF (SOXX) fell 7.88%. In Asia, South Korea’s Kospi slid over 10% as foreign investors pulled more than $2.5 billion from chip stocks. Sandisk (SNDK) lost 13.64%, Micron Technology (MU) lost 13.18%, while Samsung Electronics dropped more than 12%. The sell-off started in Asia and spread globally as investors began questioning whether heavy AI spending can really support current chip valuations.

But while chip stocks were falling, International Business Machines (IBM) moved the other way. The stock jumped 5.3% in midday training to lead the Dow Jones industrials after JPMorgan upgraded it to “Overweight” from “Neutral” and raised its price target to $291. The firm pointed to stronger confidence in software growth going into the second half of 2026, noting that software makes up about 45% of revenue but drives roughly two-thirds of total profit.

Software is already doing most of the heavy lifting, yet IBM still trades below many software-focused peers. If one upgrade can move the stock like this in a weak market, what happens next if the company keeps delivering or if expectations start to slip?

Inside the Latest Numbers

IBM has been shifting its business toward software, hybrid cloud, and consulting, with Red Hat and its automation tools playing a big role in that transition. But the stock hasn’t fully reflected that shift yet. Shares are down 10.49% over the past 12 months and off 11.23% year-to-date (YTD).

That shows up in valuation, too. International Business Machines trades at a forward price-to-earnings of 20.37 times, below the sector average of 23.44 times, suggesting the market is still not fully convinced about its growth path.

At the same time, it offers a 2.67% dividend yield, well above the tech sector average of 1.37%, backed by 31 straight years of dividend increases. The most recent payout was $1.690 on May 8, 2026, with a forward payout ratio of 55.60% and quarterly payments.

Looking at the latest results, execution has been steady. Q1 2026 revenue came in at $15.92 billion, ahead of the $15.71 billion estimate and up 9.5% year-over-year (YOY). Software brought in $7.05 billion, slightly beating expectations and continuing to lead the business.

Adjusted EPS was $1.91 versus $1.81 expected, while EBITDA reached $4 billion, above the $3.54 billion estimate, with a 25.1% margin. Operating margin improved to 11.7% from 10% a year ago, and free cash flow margin held at 13.9%, showing the company is still generating solid cash.

What’s Driving IBM’s Growth

IBM recently joined OpenAI’s Daybreak Cyber Partner Program, bringing advanced AI into cybersecurity through Project Lightwell. The company rolled out a new application security service that uses OpenAI’s models to find and confirm software vulnerabilities faster and more accurately. Instead of basic code scanning, it reviews application code more deeply and flags areas most likely to be exploited.

Also, the firm expanded its partnership with ServiceNow (NOW) to tackle two common problems holding back AI adoption, messy data and outdated systems. The joint effort combines IBM’s data and automation tools with ServiceNow’s platform to help companies upgrade existing systems instead of replacing them. And, it allows businesses to better use their data and automate IT operations more effectively.

At the same time, International Business Machines teamed up with Alphabet's Google Cloud (GOOGL) to help companies roll out AI faster. The new practice combines IBM’s consulting platform with Google’s Gemini tools, giving clients a way to build and manage AI solutions across different industries. IBM is using this setup to create ready-to-use AI tools for sectors like banking, telecom, energy, and healthcare, helping businesses automate tasks and improve decision-making across complex systems.

Wall Street’s New View

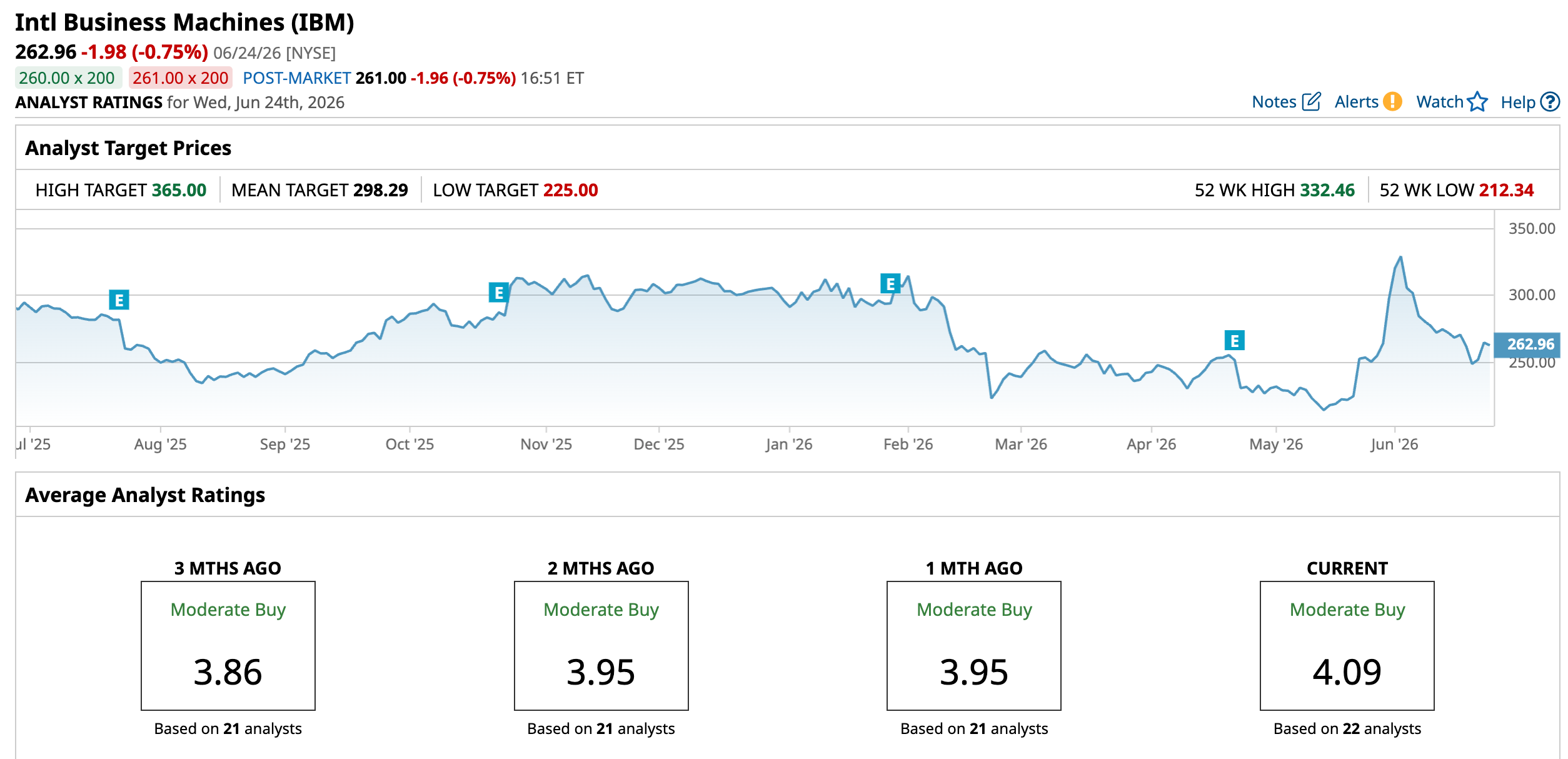

International Business Machines is set to report earnings on July 22, and expectations are steady. Analysts see $2.96 for the June quarter, up 5.71% from $2.80 a year ago. Estimates for the September quarter come in at $2.86, which would be 7.92% growth from $2.65. For the full year, earnings are expected to reach $12.39 in 2026, up 6.90%, pointing to consistent, moderate growth.

Barclays’ Raimo Lenschow started coverage with an “Overweight” rating and a $350 price target, calling the company a steady earnings grower with added upside from quantum computing. Still, his main case is built on the strength of the software business, not future bets.

Citi’s Fatima Boolani also initiated with a “Buy” rating and a $285 target, pointing to valuation, deal synergies, and AI as the main drivers. She also highlighted how AI workloads, especially in mainframes, are helping drive both software and hardware revenue.

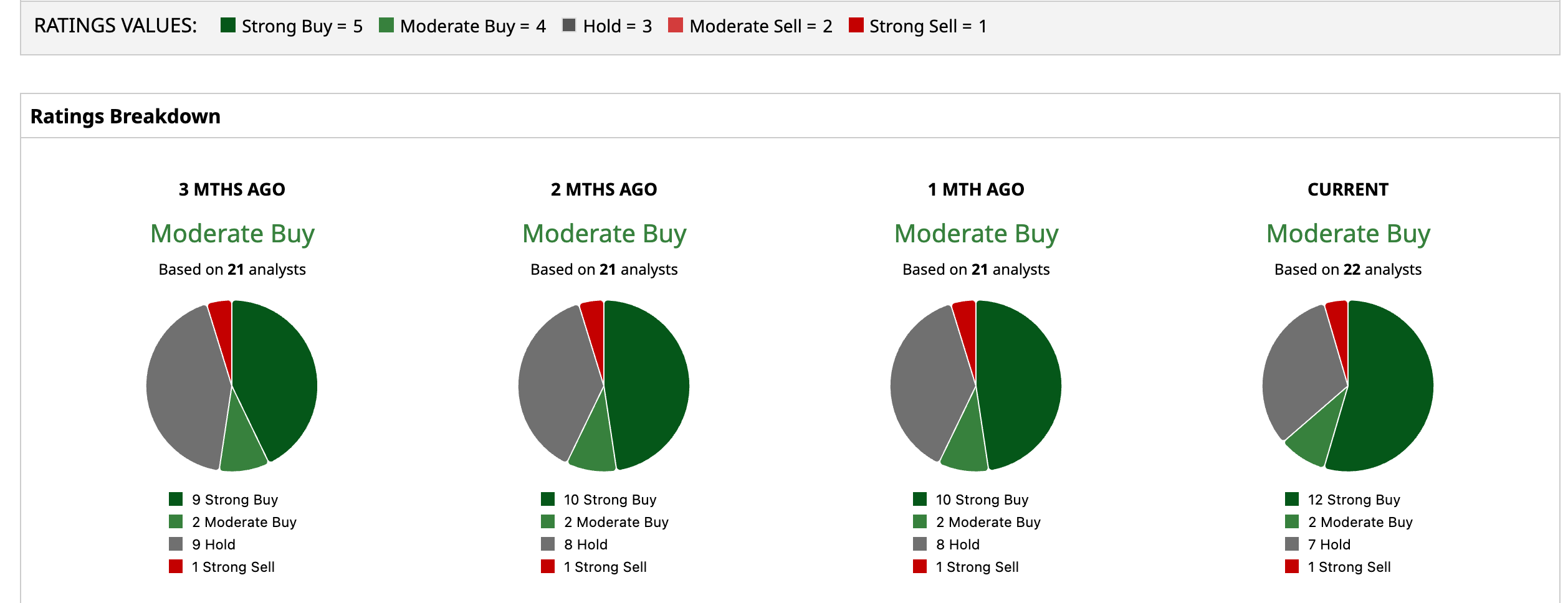

Overall, of 22 analysts covering International Business Machines a consensus rates it a “Moderate Buy,” with an average price target of $298.29. From current levels, that suggests 13.44% upside.

Conclusion

IBM’s recent jump looks less like a one-day reaction and more like a reflection of a business that is quietly getting its software story right. The numbers, partnerships, and analyst sentiment all point in the same direction, with software and AI steadily taking center stage. Even so, the upside likely depends on execution, especially as expectations around second-half acceleration build. If IBM delivers on that software momentum, share prices can rise higher from here. If not, the recent strength could fade. Right now, the path of least resistance still leans upward, but not without some volatility along the way.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)