For 130 years, the Dow Jones Industrial Average ($DOWI) has served as Wall Street’s exclusive club, a place where America’s biggest corporate names earn a seat at the table. But membership is never permanent. Since its launch in 1896 as a modest collection of 12 industrial companies, the index has been reshuffled more than 50 times as the economy evolved, making room for new winners while showing others the door.

Now, another change is set to arrive. Before the opening bell on June 29, telecom giant Verizon Communications (VZ) will officially exit the 30-stock Dow, with Google parent Alphabet (GOOG) (GOOGL) stepping into its place. The move marks the first adjustment to the blue-chip benchmark since Nvidia (NVDA) and Sherwin-Williams (SHW) joined the index in late 2024.

At first glance, the switch feels like a snapshot of the way in which corporate America has changed. A company built around wireless networks and steady cash flows is making way for a tech titan whose businesses sit at the center of artificial intelligence (AI), cloud computing, digital advertising, and the broader digital economy.

For investors, the change means that Dow-tracking funds will sell Verizon’s shares and buy Alphabet. While Verizon’s business is unlikely to change overnight, its departure raises the question of how one of America’s telecom heavyweights actually became expendable in one of Wall Street’s most prestigious indexes. Let’s take a closer look at what pushed Verizon to the sidelines and why the Dow decided it was time for a new face.

About Verizon Stock

Verizon Communications is one of the world’s largest communications providers that keeps the modern world connected. Whether it’s making a phone call, streaming a movie, working remotely, or running a large business network, Verizon’s technology helps power those everyday activities. Its wireless, broadband, fiber, and enterprise services reach millions of consumers and businesses, including 99% of Fortune 500 companies.

Founded in 2000 and headquartered in New York City, Verizon carries a market capitalization of $190.74 billion, making it one of the biggest players in the telecom industry.

As technology evolves, Verizon is betting heavily on the future. The company is combining AI with its expanding 5G network to improve performance, streamline operations, and create better customer experiences. Yet despite those efforts, the stock has spent much of the past few years navigating choppy waters. Over the past 10 years, VZ stock slipped 18.2% and has shed 19.1% over the last five years.

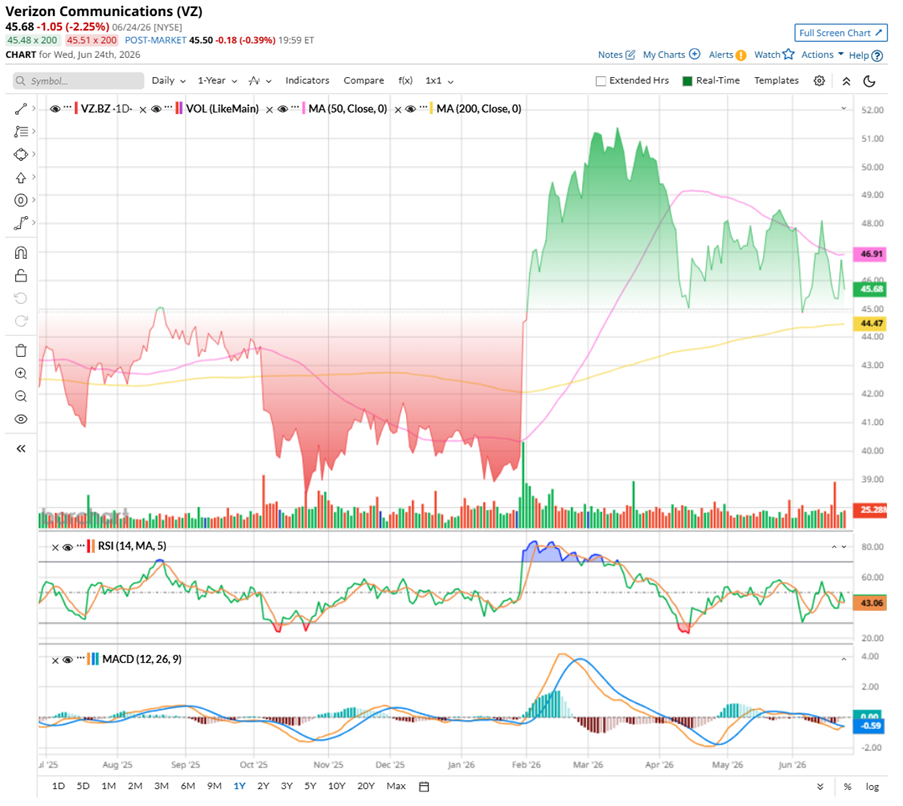

The stock hit a 52-week high of $51.68 in March before running out of steam. Since then, it has pulled back 11% and fallen 8.65% over the last three months. However, 2026 has not been all bad news. VZ stock remains up 13% year-to-date (YTD) and has gained 9.25% over the past 52 weeks.

The technical picture tells a similar story. VZ stock trades above its 200-day moving average, suggesting the longer-term trend remains intact. However, the stock has slipped below its 50-day moving average, indicating that short-term momentum has weakened, and some investors may be taking a wait-and-see approach.

The 14-day RSI is hovering near neutral at 46, suggesting the stock is neither overbought nor oversold. Meanwhile, the MACD line remains slightly above the signal line, but both are below zero, while the histogram stays negative. The bears have not fully taken control, but the bulls have not exactly grabbed the wheel either.

VZ stock looks like a bargain on the shelf. Trading at just 9.41 times forward earnings, it is priced below its sector peers, making it a quietly compelling pick for value hunters in telecom. Even so, the stock is trading above its own historical valuation range, suggesting the market has already started pricing in some operational improvement.

When it comes to income investing, Verizon continues to be one of the market’s reliable cash machines. The telecom giant has increased its dividend for more than 20 consecutive years, and management has made it clear that rewarding shareholders remains a top priority even as the company invests in growth and transformation. In June, Verizon declared a quarterly dividend of $0.7075 per share, payable on Aug. 3, which works out to an annualized payout of $2.83 per share.

That translates into a hefty 6.06% dividend yield, far above the SPDR S&P 500 ETF’s (SPY) 1.03% yield. With a forward payout ratio of 56.76%, Verizon appears to be walking a fine line, returning meaningful cash to investors while still keeping enough fuel in the tank for network investments and debt reduction. The company backed up that commitment by distributing roughly $2.9 billion in dividends during the first quarter alone.

Why Verizon Ended Up Losing Its Seat at the Dow Table

For years, Verizon looked like a safe pair of hands inside the Dow. It paid a healthy dividend, generated reliable cash flow, and rarely made headlines for the wrong reasons. But on Wall Street, standing still can sometimes feel like moving backward.

One problem was hiding in plain sight. The Dow is not weighted by a company’s size, but by its stock price. That means Verizon’s roughly $46 share price gave it very little influence over the index, despite being one of America’s largest telecom companies. One can say that Verizon was riding in the back seat while other Dow members steered the car.

The bigger issue was growth, or the lack of it. Since joining the Dow in 2004, Verizon’s stock has delivered relatively modest gains of roughly 35%. While technology giants were sprinting ahead, Verizon was moving slowly. The company remained dependable, but that does not always win a spot in an index that wants to reflect where the economy is headed.

Then there’s the balance sheet. Verizon has spent years writing big checks, from its multibillion-dollar spectrum purchases to its recent Frontier acquisition. Those deals strengthened its network, but they also piled more weight onto an already heavy debt load. Plus, the company also spends billions maintaining and upgrading its infrastructure while also paying out a sizable dividend.

That’s where the pressure starts to build. Verizon still generates plenty of cash, but a growing share of that money is being pulled in different directions – dividends, network investments, acquisitions, and rising interest costs. With less financial breathing room, investors are increasingly asking whether the company can keep all those plates spinning forever.

So, Verizon was not pushed out because it suddenly became a bad business. It simply stopped looking like the kind of company the Dow wants to showcase. In a market increasingly driven by AI, cloud computing, and digital platforms, Verizon’s steady-but-slower story no longer fits the script. The Dow decided it was time to turn the page.

A Closer Look at Verizon’s Q1 Results

If Verizon’s exit from the Dow tells one story, its first-quarter earnings report, released in April, tells another. Investors could have easily focused on the revenue miss, but the market chose to look beyond that speed bump. Total operating revenue rose 2.9% year-over-year (YOY) to $34.44 billion, but landed slightly below Wall Street’s expectations. Part of that shortfall came from Verizon pulling back on aggressive promotions and issuing customer credits after a major January network outage.

Adjusted EPS jumped 7.6% annually to $1.28, beating expectations and marking Verizon’s strongest quarterly profit growth since 2021.

Meanwhile, Verizon added 55,000 postpaid phone customers during the quarter, its first positive first-quarter result in that category since 2013. For a business that has spent years fighting intense competition, that was a welcome sign that its customer-retention efforts may finally be bearing fruit.

The broadband business was also impressive, with Verizon adding 341,000 broadband customers, including 214,000 fixed wireless subscribers and 127,000 fiber customers. That growth pushed its next-generation connectivity footprint to roughly 16.8 million fixed wireless and fiber connections.

Also, VZ made progress in cleaning up its balance sheet. After closing the Frontier acquisition, Verizon has already paid off about half of the acquired debt and expects to wipe out most of the remainder before year-end. Meanwhile, it repurchased $2.5 billion worth of stock and remains on track to exceed its full-year buyback goal.

Verizon continued to generate healthy cash during the first quarter, with free cash flow rising 4% YOY to $3.8 billion. The company also ended the quarter with a solid $8.4 billion cash cushion. However, debt remains a key area to watch. Verizon carried $172.5 billion in total debt at quarter-end, including $142.5 billion in unsecured borrowings. Its unsecured debt stood at roughly eight times trailing 12-month net income, while net unsecured debt equaled 2.6 times adjusted EBITDA.

The quarter gave management enough confidence to raise its full-year outlook. They estimate adjusted EPS growth of 5% to 6% and believe postpaid phone additions will land in the upper half of its target range of 750,000 to one million customers. That would be roughly two to three times better than what the company achieved in 2025.

So, while Verizon may be losing its spot in the Dow, the company’s operating performance suggests it is far from throwing in the towel. Analysts tracking the company anticipate its Q2 EPS to be $1.27, up 4.1% YOY, on revenue of roughly $35.4 billion. For fiscal 2026, EPS is anticipated to rise 5.5% YOY to $4.97, and then rise by another 5.6% annually to $5.25 in fiscal 2027.

What Do Analysts Expect for Verizon Stock?

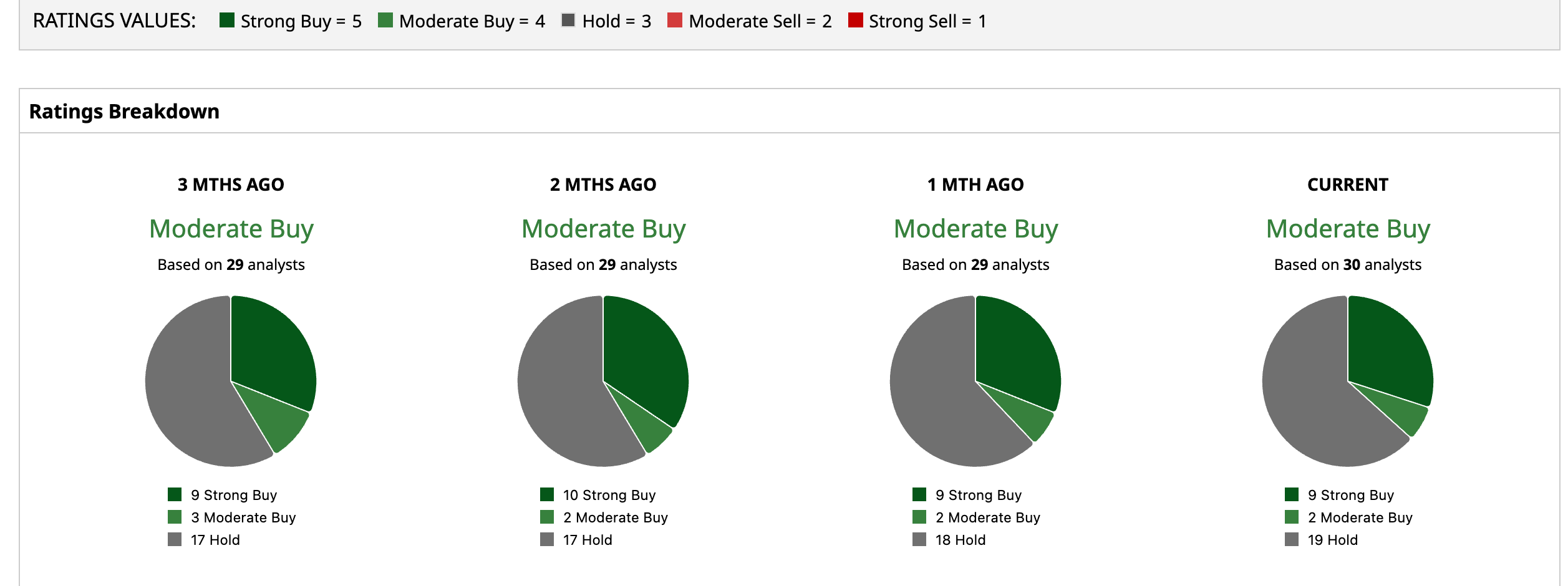

Despite losing its seat at the Dow table, Verizon is not exactly being sent to the penalty box by investors. VZ stock has a “Moderate Buy” consensus, and of the 30 analysts monitoring the telecom stock, nine suggest a “Strong Buy,” two recommend a “Moderate Buy,” and a majority of 19 analysts are playing it safe, advising a “Hold.”

The average analyst price target for VZ is $51.96, indicating a potential upside of 12.9%. The Street-high target price of $71 suggests that the stock could rally as much as 54.3% from here.

Final Thoughts on Verizon

So where does VZ stock go from here? The answer is not exactly black and white. On one hand, stronger subscriber growth, improving earnings, and its hefty 6% dividend give income investors reasons to stick around. On the other hand, slowing stock momentum, a sizable debt load, and its removal from the Dow could keep a lid on near-term gains. For now, Verizon looks like a stock caught between two stories - one about stability and income, the other about proving its transformation is finally paying off. The next few quarters may determine which story wins.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)