SanDisk Corporation (SNDK) has come a long way from the days when it was best known for portable storage devices. Since its spin-off from Western Digital Corporation (WDC) in early 2025, the company has reinvented itself, shifting its focus toward enterprise storage solutions built for artificial intelligence (AI).

Money that once flowed almost exclusively into names such as Nvidia Corporation (NVDA) and Broadcom (AVGO) has increasingly found its way into memory chip makers. SNDK stock has gained 737.7% in 2026. Momentum reached another level on June 22, when shares touched a fresh 52-week high of $2,354.39 after climbing 4.1% during the trading session.

Morgan Stanley (MS) said SanDisk believes AI is “fundamentally changing” the NAND market. The view stems largely from the growing demand for inference. Analyst Joseph Moore explained that expanding large language model (LLM) key-value (KV) cache requirements and larger context windows are creating storage needs that dynamic random-access memory (DRAM) simply cannot handle on its own.

As a result, NAND is moving higher in the memory hierarchy. The backdrop becomes even more favorable as cloud computing is expected to become the largest end market for NAND later this year. That shift already appears in SanDisk’s numbers.

Its data center segment surged 233.4% sequentially to $1.47 billion in Q3 FY2026, driven by strong demand for triple-level cell (TLC)-based enterprise solid-state drives (SSDs) built for performance-intensive AI workloads.

Quad-level cell (QLC) Stargate solutions, which have been under hyperscaler qualification for over a year, are now expected to begin shipping for revenue in Q4, adding another layer of growth on top of the TLC momentum already underway.

About SanDisk Stock

Based in Milpitas, California, SanDisk develops and manufactures storage solutions powered by NAND flash technology. With a market cap of roughly $323.5 billion, the company offers a broad portfolio that spans SSDs, embedded storage products, memory cards, universal serial bus (USB) drives, wafers, and other storage components.

SanDisk’s shares have skyrocketed 4,131.6% over the past 52 weeks and surged 182.8% in the last three months. The rally hardly slowed from there. Investors enjoyed a 34.36% gain over the past month, but the stock has slipped 5.75% in the last five trading sessions.

The remarkable run has encouraged investors to place a hefty premium on the company’s future. SNDK stock is currently trading at 34.13 times forward adjusted earnings and 17.17 times sales. Both valuations sit above industry averages, reflecting Wall Street’s confidence that the company has meaningful room to grow despite its eye-popping rise.

SanDisk Surpasses Q3 Earnings

SanDisk gave investors plenty to cheer about when it reported Q3 FY2026 results on April 30. The stock climbed 3.04% on the day of the announcement and carried that momentum into the following session, advancing another 8.25%.

Revenue surged 251% year-over-year (YOY) to $5.95 billion, topping Wall Street's $4.55 billion estimate. Non-GAAP EPS amounted to $23.41, running well ahead of the $14.36 analyst estimate. The bottom line marked a dramatic turnaround from the small loss recorded in the same quarter a year earlier.

Delving deeper, non-GAAP gross profit soared 1,111.9% YOY to $4.7 billion. Non-GAAP operating income jumped to $4.2 billion from just $2 million in the comparable period last year. Meanwhile, non-GAAP net income reached $3.7 billion, reversing a $43 million net loss posted during the prior year quarter.

The company’s financial position strengthened alongside earnings. SanDisk ended the quarter with $3.7 billion in cash and cash equivalents and completely eliminated its debt burden after repaying its term loan in full.

Looking forward, management has added fuel to the bullish narrative with an upbeat Q4 FY2026 forecast. The company expects revenue between $7.75 billion and $8.25 billion, while non-GAAP EPS is projected to range from $30 to $33.

On the other hand, analysts also expect EPS to surge 158,950% YOY to $31.81 in Q4. Full-year FY2026 earnings estimates stand at $64.01, implying growth of 3,496.1%, with projections calling for another 180.9% jump to $179.82 in FY2027.

What Do Analysts Expect for SanDisk Stock?

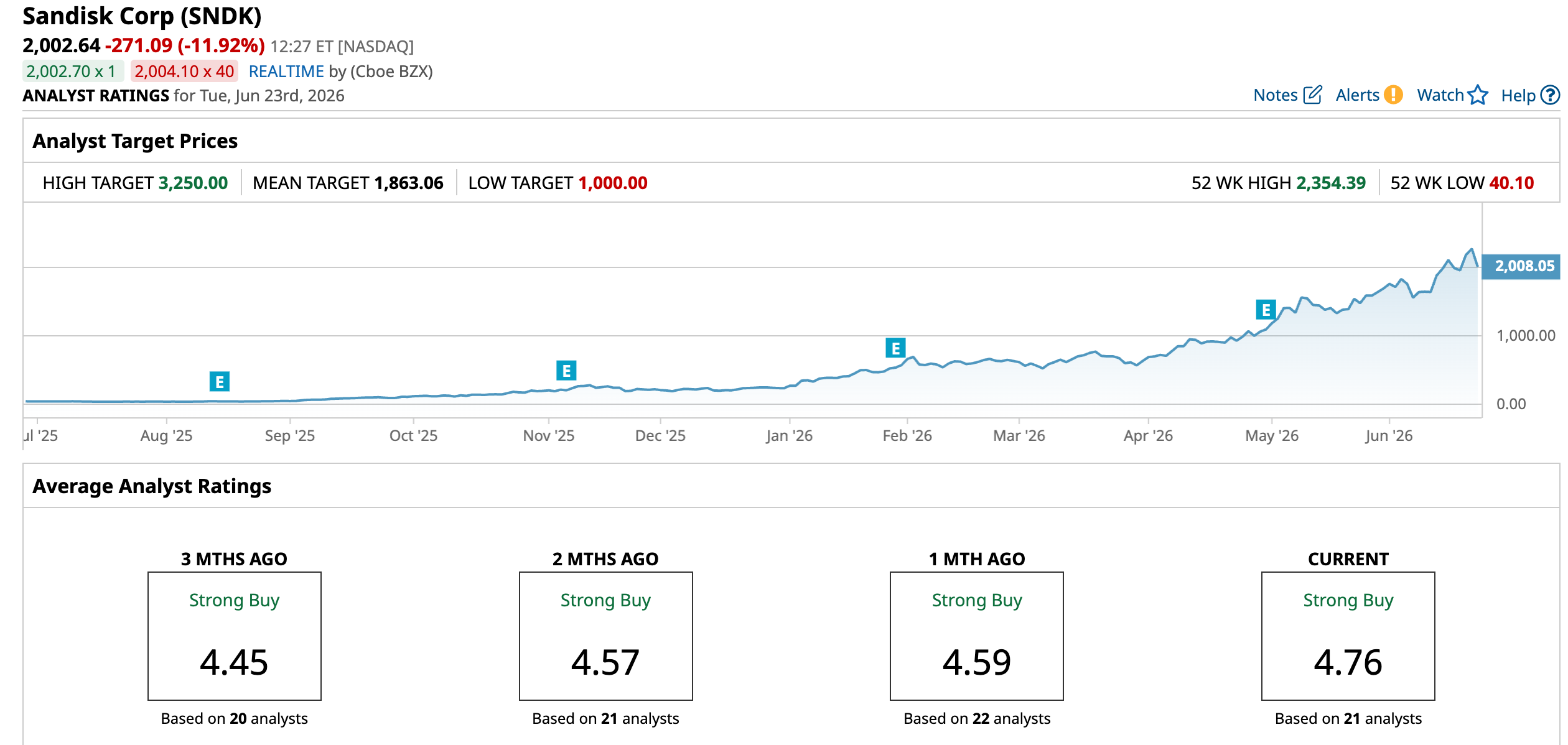

Wall Street’s confidence in SanDisk remains hard to miss. Morgan Stanley analyst Joseph Moore maintains an “Overweight” rating on the stock and has assigned a price target of $1,750, reflecting his positive view of the company’s long-term prospects and its position within the rapidly evolving memory market.

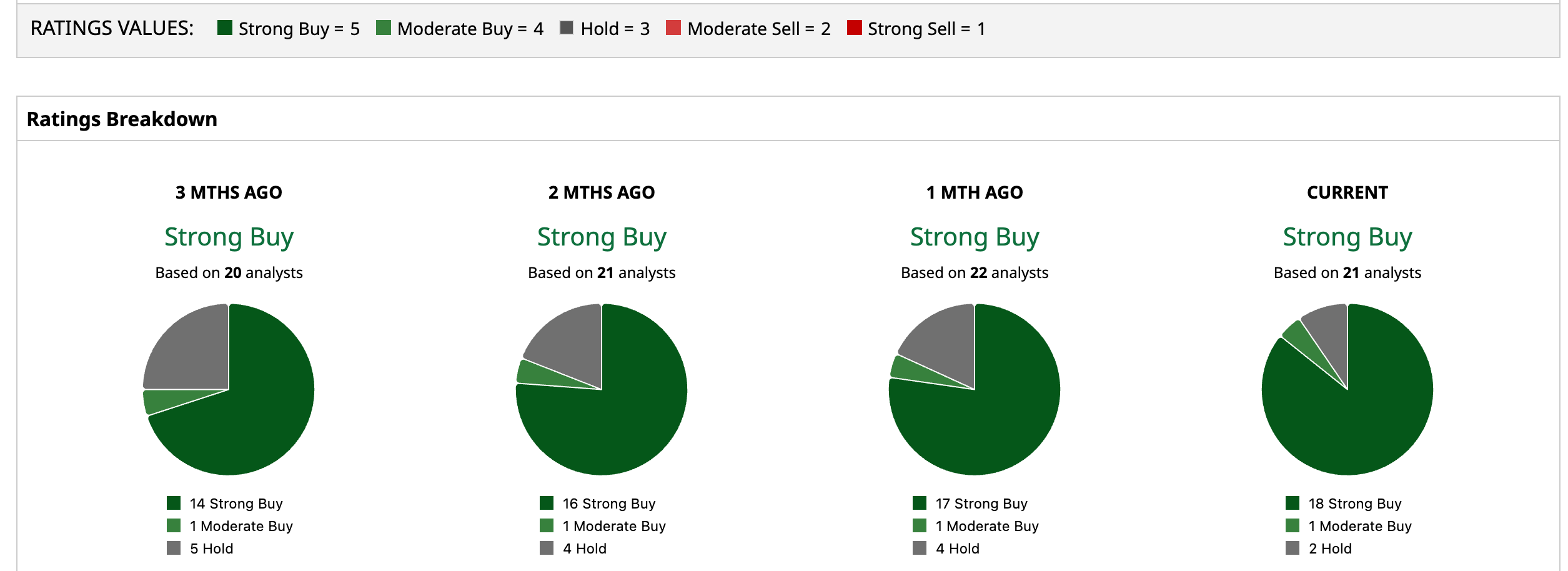

The bullish sentiment stretches well beyond a single firm. SanDisk currently holds an overall “Strong Buy” rating. Of the 21 analysts covering the stock, 18 recommend “Strong Buy,” one rates it “Moderate Buy,” and two suggest investors simply “Hold” their positions.

What makes the story even more intriguing is that SanDisk has already sprinted beyond Wall Street’s average price target of $1,863.06. Even after the stock’s remarkable run, however, some analysts still see additional upside ahead. The Street-High target of $3,250 suggests a gain of 62.3% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)