U.S. equities opened sharply lower today, pressured by an accelerating global selloff in Big Tech and AI-linked semiconductor stocks, alongside a meaningful shift in macroeconomic expectations. The Invesco QQQ Trust (QQQ) is down more than 2.8% as investors rapidly de-risk high-multiple growth exposure following a wave of weakness that began overnight in Asia and spread across Europe.

The epicenter of the decline is a broad-based unwind in AI and semiconductor names, driven by growing skepticism around the sustainability of massive capital expenditures tied to artificial intelligence infrastructure. South Korea’s Kospi Index plunged 10%, triggering a temporary trading halt, with memory chip leaders Samsung and SK Hynix each falling more than 12%. Japan’s Nikkei 225 Index dropped 3.6%, led by heavy losses in SoftBank, while European semiconductor leader ASML (ASML) is also under pressure, adding to the downside momentum in global chip stocks and weighing heavily on U.S. tech sentiment.

Compounding the weakness, a sharp 16% decline in SpaceX (SPCX) shares wiped out approximately $400 billion in market value in a single session — one of the largest drawdowns on record — raising concerns that valuations across high-growth, AI-adjacent sectors may have become overstretched. At the same time, a more hawkish tone from Federal Reserve Chair Kevin Warsh has further rattled markets. Signals of a potential rate hike as soon as September, combined with stronger-than-expected economic data, are creating a double headwind for growth stocks by compressing equity risk premiums while increasing the relative appeal of cyclical sectors.

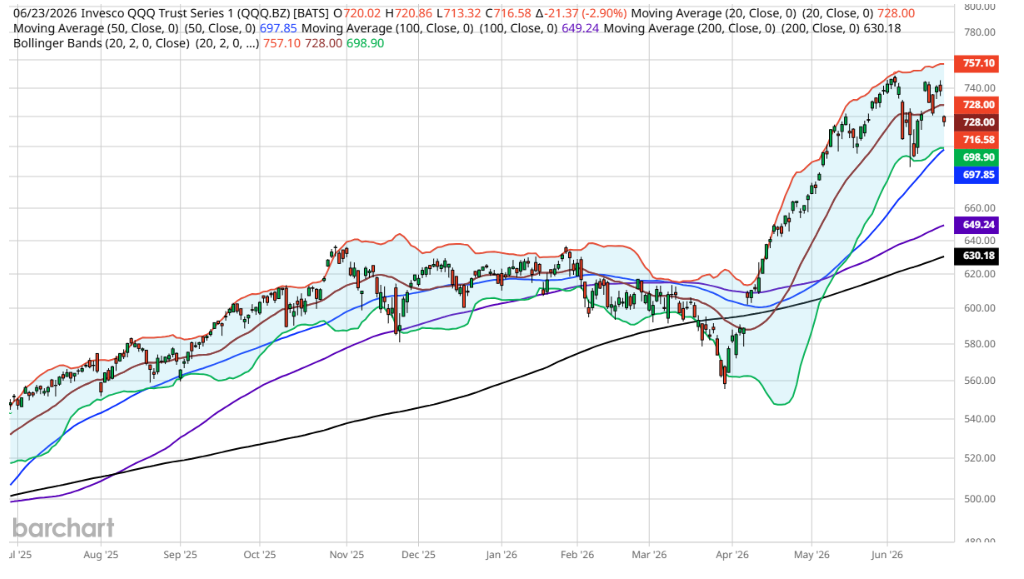

From a technical perspective, the focus now shifts squarely to key support levels on the Nasdaq. The first line of defense comes in at the 50-day moving average near 28,695, which also aligns with the lower Bollinger Band — creating a confluence zone that often attracts short-term buyers in trend-following markets. A decisive break below that level would likely accelerate downside momentum, opening the door for a retest of the June 6 swing low at 28,202. That level represents a critical pivot in the current uptrend structure; a failure there would shift the intermediate-term trend from consolidation to potential trend reversal.

Adding to the crosscurrents, oil prices have eased, with Brent crude (CBQ26) pulling back toward $76 per barrel following signs of geopolitical progress, including potential U.S. sanction waivers on Iranian crude exports.

While lower energy prices are broadly disinflationary, the immediate market reaction reflects a broader risk-off tone, particularly in crowded momentum trades. As markets head into the session, traders will be watching whether these technical levels can stabilize price action or if continued liquidation in semiconductors forces a deeper reset, with upcoming earnings from Micron on June 24 likely serving as the next key catalyst.

– Read more from Barchart’s Senior Market Strategist John Rowland, CMT, here.

On the date of publication, Barchart Insights did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)