With a market cap of $11.6 billion, Camden Property Trust (CPT) is a real estate investment trust (REIT) that owns, develops, acquires, and manages multifamily apartment communities across the United States. The Houston, Texas-based company focuses primarily on high-growth markets in the Sun Belt region.

Companies worth $10 billion or more are generally described as "large-cap stocks." Camden fits right into that category, with its market cap exceeding this threshold, reflecting its substantial size and influence in the residential REIT industry.

Camden Property Trust's portfolio consists of apartment communities located in states such as Texas, Florida, North Carolina, Georgia, Arizona, Tennessee, and Colorado. In addition to managing existing properties, Camden develops new apartment communities and selectively acquires assets to expand its portfolio. Its strategy emphasizes markets with strong job growth, favorable demographics, and rising housing demand.

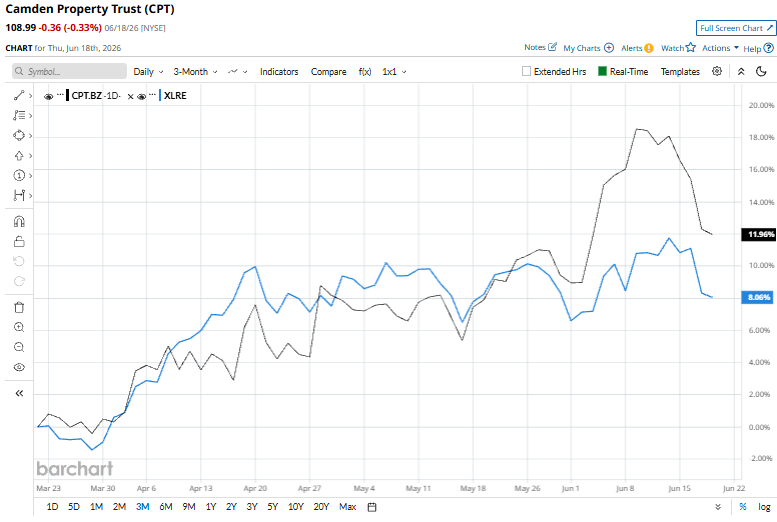

Despite its notable strengths, CPT stock is down 7.2% from its 52-week high of $117.50. Meanwhile, the stock soared 8.6% over the past three months, outpacing the State Street Real Estate Select Sector SPDR Fund’s (XLRE) 4.4% gain over the same time frame.

Camden's longer-term performance has been underwhelming. The apartment REIT is down 1% year-to-date and has lost 5.7% over the past 52 weeks, sharply trailing XLRE’s 8.7% gain in 2026 and 4.8% return over the same one-year period.

However, beneath the lackluster price action, signs of a turnaround are emerging. Since late April, CPT has reclaimed its 50-day moving average and moved above its 200-day moving average in mid-May, suggesting bullish momentum is beginning to build.

On May 14, shares of Camden Property Trust slipped more than 1% after Scotiabank downgraded the apartment REIT to "Sector Underperform" from "Sector Perform" and set a $95 price target. The downgrade reflected concerns over the company's near-term growth outlook, as elevated apartment supply in several of its Sun Belt markets is expected to pressure occupancy levels and rent growth, creating headwinds for earnings performance.

When compared to its peer, CPT has outpaced Invitation Homes Inc.’s (INVH) 15.9% plunge over the past 52 weeks.

Among the 25 analysts covering the CPT stock, the consensus rating is a “Moderate Buy.” Its mean price target of $114.31 suggests a 4.9% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)