/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

We’ve just seen the biggest IPO in history, and it’s a space stock.

And, look, I get the hype.

Rockets are launching more often, satellite networks are expanding, defense spending is moving toward orbit, and investors are once again imagining a much bigger space economy.

But before buying into the excitement, I think investors need to ask much simpler questions: how do these companies actually make money, and is it really a good time to buy?

And beyond that, the obvious question is: which stocks should you consider?

Because space may sound futuristic, but the businesses are surprisingly practical. Some companies sell launches. Some sell connectivity. Some sell satellite components. Others depend heavily on government and defense contracts.

So, today, I’ll cover the space subsector, the headwinds, tailwinds, and perhaps more importantly, how and which companies stand to benefit most from the hype.

Commercial money now drives 71% of the space economy

As the (very wise) words of legendary investor Warren Buffett go, “Never invest in something you don’t understand.” The motto has guided me for my 25+ years in investing, and it’s the first thing I consider before hitting “buy.”

But one doesn't really need to study the complete ins and outs of a business before buying. At least, not yet. Long-term investors can start by figuring out how the business makes money, today.

Now, sure, it’s easy to fall into the trap that “space companies” are the ones that are pushing to become the next Weyland-Yutani from “Alien” or the CEC from “Dead Space.” I’m telling you right now that, no, we're not close enough to that kind of technology. Not in 2026, anyway.

But despite any futuristic images that may be conjured up, today's space economy is remarkably practical. Much of it revolves around communications, Earth observation, national security, and the infrastructure required to support those activities.

Right now, the best way I think we can categorize companies in the space sector is akin to how we do it with energy companies: they can be upstream or downstream operators.

Upstream companies build and launch space assets. These are the rockets, satellites, spacecraft buses, sensors, propulsion systems, the works. On the other hand, downstream companies monetize the services that those assets provide, like broadband, imagery, weather data, navigation, defense surveillance, analytics, communications, and research access.

Think of them like this: upstream companies are those making the “picks and shovels,” while downstream companies are the service providers. One group builds the highways to space, while the other generates revenue from the traffic moving across them.

Of course, the line isn't always perfectly clear. Some companies operate, Exxon-style, across both segments. A satellite operator, for example, might manufacture portions of its own hardware while also selling communications services directly to customers. And that ties directly into the next question: how does the company monetize its business?

Is it rocket launches, which can represent large, one-time revenues, or satellite service subscription models, which could provide stickier recurring revenue?

Another important distinction is who the customer actually is.

The usual suspects are your commercial and government contracts. Think defense & space agencies, plus national security programs – all with deep pockets, who often provide the early demand that allows these companies to scale.

Space launches: A look back to 2025

Back in the day, only a few governments with “blank check”-writing abilities could launch rockets into space.

Today, the space industry is enjoying a trend of declining launch costs, which could be a major catalyst for growth.

With infrastructure in place and launch cadence increasing across the board, the economics of deploying satellites and conducting missions are becoming increasingly attractive. Government clients have always been there, but commercial demand is also stepping in to fuel further expansion.

In fact, the Satellite Industry Association reported a historic 296 launches that deployed over 4,434 satellites into space in 2025 alone. That represents a 65% increase year over year. And if we’re going by dollar value alone, the commercial satellite industry accounted for roughly $303 billion, or 71% of the world’s space business.

But let’s not discount government spending just yet. The fact is, nations are increasingly viewing space as critical infrastructure. Missile warning systems, surveillance systems, navigation, and weather monitoring increasingly require connectivity beyond your usual cellular service. This creates a tangible demand for rocket launches, satellite manufacturing, low-Earth orbit constellations, and secure communication links.

Speaking of communication links, satellite connectivity is a major catalyst for the sector. For the longest time, communications via space satellites have been facilitated by specialized equipment like satphones.

Today, several space companies are pushing for a global mobile coverage layer. That means satellite-grade connectivity on your smartphone, so no dead zones anywhere for Verizon’s “Test Man” to worry about.

Beyond those admittedly cool concepts, a global mobile layer has practical applications in emergency messaging, disaster response, and military operations.

So, the market is big and is growing as we speak. But is now really the best time to invest in space stocks?

Why SpaceX lost $657 million on launches in 2025

I opened the previous section by noting that space launches are getting cheaper. That’s 100% true. But that doesn’t mean they’re dirt-cheap, or that anyone can build a rocket. The space industry is still one of the most capital-intensive in the world.

The upfront investments for building infrastructure and parts can be, well, astronomical. Businesses often spend years in the red while they get engineering, manufacturing, and testing right. Even then, there’s no assurance that anyone’s going to buy the rocket launch.

So, even companies with promising technology can struggle if they run out of capital before reaching profitability.

The market might love the story during growth cycles – which, frankly, we’re seeing right now. But if capital markets tighten, these companies can be forced to dilute shareholders, slow deployment, take on expensive debt, or delay programs.

Another headwind for the space industry is timelines.

Anyone who’s been monitoring space stocks for the past few years isn’t new to the concept of delay. Rockets can be delayed. Launch windows can move. Regulatory approvals can take longer than expected. Manufacturing yields can disappoint. Ground infrastructure can lag. Customer programs can be pushed out.

And as any of those potential scenarios happen, the company’s stock usually takes a hit, making the overall ride rocky and volatile. Even worse, certain programs can outright fail, resulting in a significant loss of both money and reputation for the company.

Another risk often overlooked in favor of business-side headwinds is what scientists call the Kessler effect. It states that at a certain point, objects in low Earth orbit become so numerous that collisions between satellites are inevitable. Individual debris from broken satellites travels at incredible speeds, breaking through other objects and triggering a chain reaction that causes multiple impacts, resulting in millions of dollars in damage and inhibiting future launch missions.

But every investment has its own risk-reward profile. These are very real concerns, yes, but the overall opportunity seems to outweigh them by a significant margin.

The space market could reach $1.1 trillion by 2034

So the next question becomes: How big is the opportunity, really?

After all, even the best business model has limits if the market itself is too small.

The global space technology market was valued at just over $600 billion in 2025 and is expected to grow at a 7.2% compound annual growth rate (CAGR), reaching approximately $1.1 trillion by 2034.

So, yes, the sector is ripe with opportunities, and investors are excited about it.

We can see that plainly in SpaceX’s stock market debut: the biggest IPO in history by a wide margin, several times oversubscribed, and up nearly 20% in its first day.

And that’s where I’m starting my list.

Space stock #1. Space Exploration Technologies Corp (SPCX)

SpaceX used to be a pure rocket-launch company, but with Starlink, it has successfully pivoted into a satellite internet operator. It’s essentially a combination of an upstream and a downstream space company.

SpaceX makes money by using rockets to build space infrastructure, then monetizes that infrastructure through subscriptions, government contracts, and launch services.

Regarding Starlink, at the end of March 2026, SpaceX reportedly disclosed that it had about 10.3 million subscribers across 164 countries or markets. Those subscribers connected to roughly 9,600 Starlink broadband and mobile satellites in low Earth orbit for their internet needs.

Many of these customers can be much more valuable than ordinary home internet users. Think airlines, cruise ships, military units, oil platforms, or mining sites. All will pay far more than a household because connectivity is critical to their operations. And it’s not limited to the internet: SpaceX is also monetizing satellite-to-phone connectivity, which could turn the company into a telecom provider with global coverage.

But, of course, we can’t talk about SpaceX without covering its rockets. SpaceX makes money launching satellites, cargo, astronauts, and other payloads into orbit. Well, I say it “makes” money, but the fact is, the segment operates at a loss. The company’s Space segment reported a loss from operations of $657 million in full-year 2025 and $662 million in Q1 2026 alone.

But if we’re looking at the bigger picture, these losses are necessary. Space launches may be expensive, but building the infrastructure is already giving SpaceX major benefits. Setting up and launching Starlink’s global constellation of satellites, which is basically the moneymaker, could be even more expensive if the company went to a third-party launch provider.

Now, what I don’t like about SpaceX is that its artificial intelligence (AI) strategy feels like a major leap outside of the company’s original core competency. The company acquired another Musk-led startup, xAI, before going public, adding a large and expensive AI business to an already complicated mix of rockets, Starlink, defense contracts, and future space-infrastructure bets.

There are also rumors of merging Tesla with SpaceX, another Musk-led company with a murky vision. If you’re an optimist, you can say it might accelerate innovation and provide Tesla with direct exposure to the space industry. But for me, it just exposes both companies' weaknesses to each other.

Still, despite the murkiness in the overall vision, having the infrastructure and capacity for internal launches is one of SpaceX’s biggest selling points. That means the company can put satellites in orbit faster and more frequently, while competitors that depend on third-party contractors for launches still need to go through the hoops of business deals and other negotiations.

But that’s where SpaceX’s arguably biggest competitors in the market come into play.

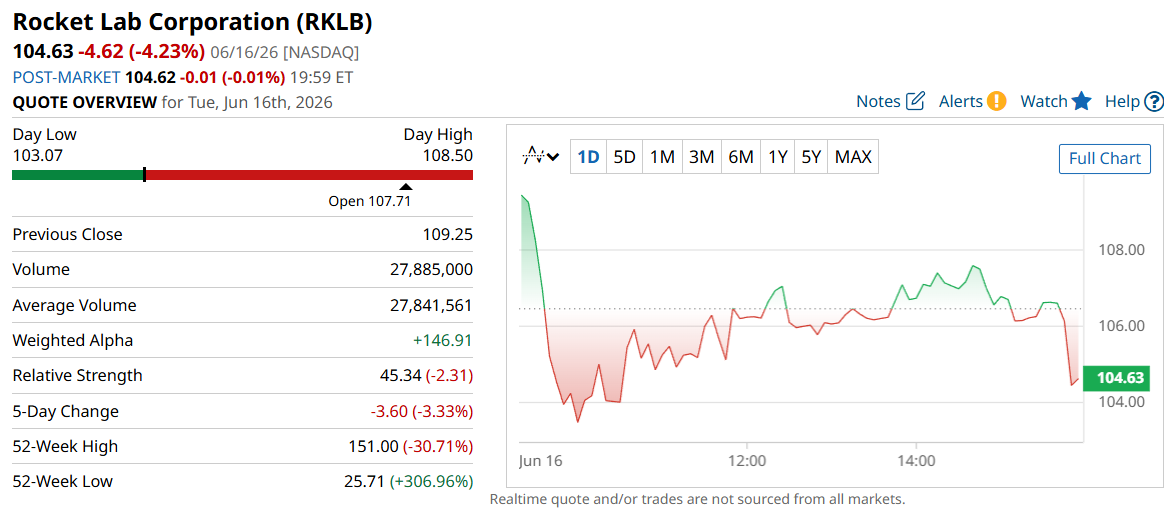

Space stock #2. Rocket Lab (RKLB)

Rocket Lab started out looking mostly like a small-launch company, but it’s increasingly becoming a broader end-to-end space infrastructure company. It doesn’t own an internet network to monetize, but the company is doing something that SpaceX still hasn’t managed yet: controlling the value chain.

Rocket Lab makes money through two main businesses: Launch Services and Space Systems. Launch Services is the rocket side of the business, led by Electron for small orbital payloads and HASTE for hypersonic test missions. There’s also the newer, but oft-delayed Neutron Rocket, which directly competes with medium-sized lifts in the market.

However, Space Systems is the more interesting side of the business. This segment covers spacecraft design, satellite manufacturing, solar power, reaction wheels, star trackers, radios, separation systems, optical systems, propulsion, and on-orbit mission management.

Essentially, Launch Services is all about selling rockets, while Space Systems is about everything that goes into building and operating what those rockets carry. And this vertically integrated business model is already working.

Q1 2026 revenues reached $200.3 million, growing 63.5% year over year, with product revenue contributing $127.5 million, or roughly 64% of total revenue.

Meanwhile, defense is becoming a major part of Rocket Lab’s narrative. Late last year, Rocket Lab won an $816 million Space Development Agency contract to design and manufacture 18 satellites for the Tracking Layer Tranche 3 program under the Proliferated Warfighter Space Architecture.

That said, Rocket Lab is still not profitable. In Q1 2026, Rocket Lab posted an operating loss of $56.0 million and a net loss of $45.0 million. The company is growing, make no mistake about that, but that kind of growth comes at a cost. A major reason for that is Neutron, Rocket Lab’s medium-lift rocket currently in development.

Neutron is designed to move Rocket Lab beyond small launches and into larger constellation deployments, national security missions, and exploration payloads. The result would be an expansion of Rocket Lab’s addressable market.

If Rocket Lab successfully brings Neutron online, it can compete for larger missions and potentially secure more valuable launch contracts. But we haven’t seen that yet, and the project is still mired with delays. But this is where Rocket Lab’s model starts to resemble SpaceX, at least in a lateral sense.

SpaceX uses rockets to deploy and support Starlink. Rocket Lab uses rockets to strengthen its end-to-end space systems platform. In both cases, launch is the critical, non-negotiable backbone of a larger infrastructure strategy, despite being an enormous investment.

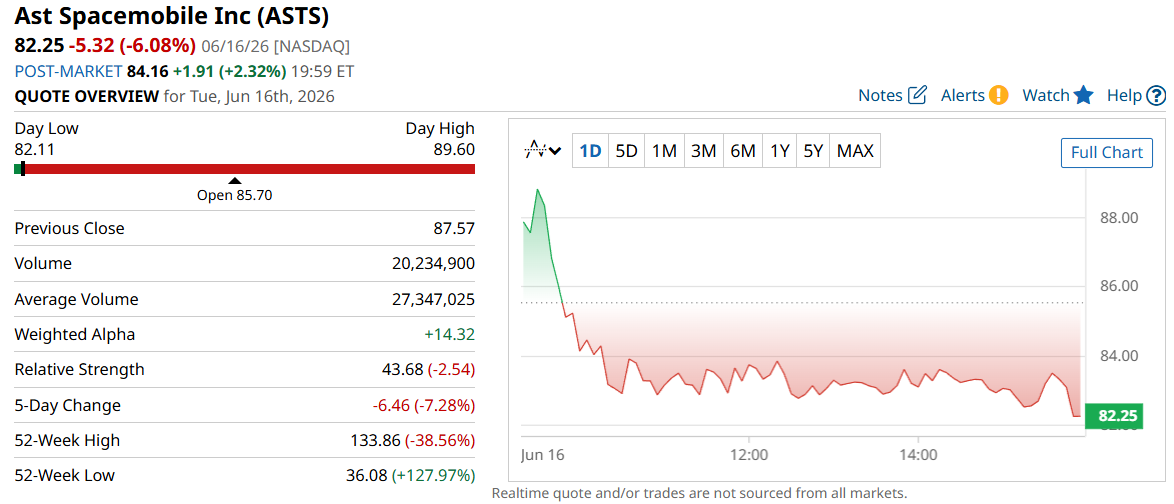

Space stock #3. AST SpaceMobile (ASTS)

AST SpaceMobile is a very different kind of space company from SpaceX or Rocket Lab. It isn’t primarily trying to sell rocket launches, satellite parts, or imagery. In fact, it doesn’t even build its own rockets. ASTS is trying to become a space-based cellular broadband infrastructure company.

The simplest way to frame it is this: AST SpaceMobile wants to turn satellites into cell towers in space.

Its goal is to provide direct-to-device connectivity to ordinary, unmodified smartphones. That means a user wouldn’t need a Starlink dish, a special satellite phone, or a dedicated terminal. The phone would connect directly to AST’s satellites using spectrum from mobile network operators. Right off the bat, that threatens SpaceX’s satellite-to-phone service.

But you may find it odd that AST is not scrambling to get subscribers to sign up for their services. Instead, the company is focusing on partnerships with mobile network operators, or MNOs. The company wants to plug into existing wireless carriers and help them extend coverage where terrestrial cell towers don’t reach. That includes rural areas, highways, mountains, oceans, disaster zones, aircraft, remote industrial sites, and underserved regions.

The company says to date, it has partnered with more than 50 mobile network operators globally, serving over 6 billion subscribers. Its biggest partners include AT&T (T), Verizon (VZ), and Vodafone (VOD).

And, honestly, this business model has advantages over consumer-grade, subscriber-based models. AST isn’t a new competitor looking to muscle in on AT&T’s or Verizon’s coverage areas. It doesn’t have to spend millions on building a brand, optimizing a retail billing system, or piecing together a direct sales operation from scratch.

The provider still owns the customer relationship. AST just provides the satellite layer and dead-zone coverage. The economics of these kinds of partnerships can be shared through wholesale capacity agreements, revenue-sharing structures, government contracts, and enterprise use cases.

So the monetization opportunity is simple: provide coverage to what existing providers cannot.

Beyond that, AST also has opportunities in defense. The company’s technology could be valuable to government and defense customers because it can potentially connect ordinary, unmodified smartphones in places where normal cell networks don’t exist, have been damaged, or are being intentionally disrupted.

On its Q4 2025 call, ASTS discussed 10 government contracts executed in 2025, including a $30 million U.S. Space Development Agency award tied to the EUROPA Tranche 2 program, as well as work connected to the Missile Defense Agency’s SHIELD IDIQ.

However, I want to make it clear that AST’s revenue remains embryonic amid a heavy investment phase. Q1 2026 top-line just reached $14.7 million, and while management says that full-year guidance is on track to reach between $150 to $200 million, operational expenses are still large relative to revenue. So profitability is not likely in the near future.

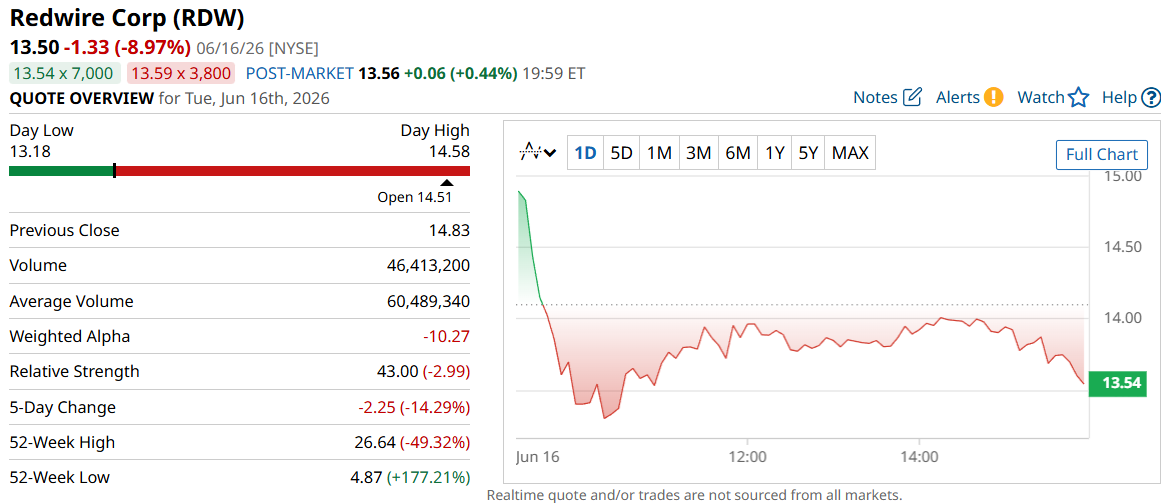

Space stock #4. Redwire (RDW)

Now, here’s an interesting pick for the space race, and the most straightforward candidate for a pick-and-shovel play in the sector.

Redwire is a space components and solutions provider. It doesn’t build rockets, but rather, it supplies the hardware, software, and systems to those who do. That includes things like deployable solar arrays, spacecraft structures, sensors, avionics, camera systems, robotic systems, microgravity payloads, digital engineering, and, of course, satellite components.

With Redwire’s acquisition of Edge Autonomy back in 2025, Redwire has also expanded into providing field-proven uncrewed airborne systems, or UAS technology. These are drones and autonomous flight systems that push Redwire further into the defense sector, where UAS is a core part of a modern military’s arsenal.

So, Redwire’s model is potentially more diversified than some pure-play space companies. It can sell into NASA and commercial space programs, but it can also sell into national security, defense, intelligence, and autonomous warfare markets.

Of course, there’s two sides to every pancake.

Militaries have deep, deep pockets, as do clients looking to launch rockets into space. In Q1 2026, Redwire reported a backlog of almost half a billion dollars. The company also has a reasonable revenue split between Space and Defense Tech, so it’s not overly dependent on any one facet of the business.

However, we can’t forget that defense and contract-based aerospace spending can be notoriously lumpy. Programs can slip, development costs can rise, fixed-price contracts can pressure margins, and revenue recognition doesn’t always move in a straight upward line. Make no mistake, Redwire is growing, but it isn’t near consistent profitability yet.

And, as you might have noticed, “not profitable” is a throughline in all of these picks, which exposes these stocks to potential volatility when they miss revenue targets or earnings guidance.

So, if you wanted a safer, more diversified exposure to space stocks, then have a look at the next candidate.

Why ARKX holds 12% in Rocket Lab & SpaceX combined

Now, if you’re more of an ETF enthusiast, these choices are for you.

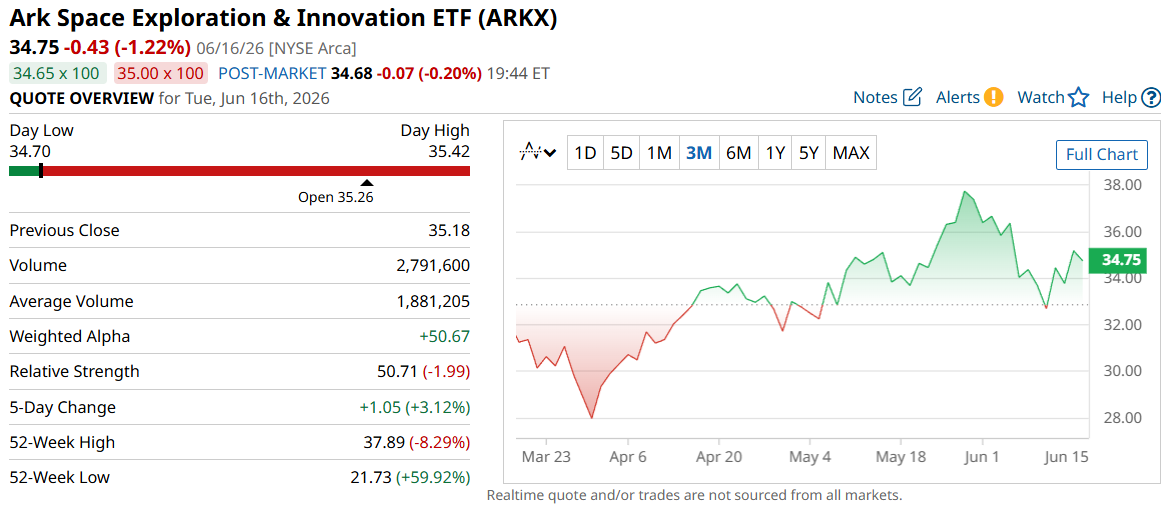

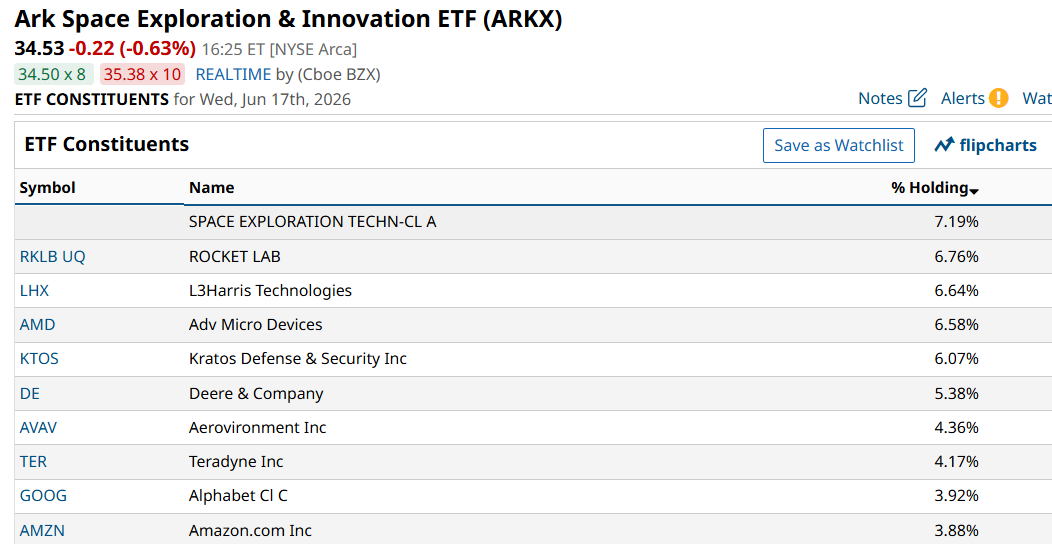

Space ETF #1. Ark Space Exploration & Innovation ETF (ARKX)

The ARK Space and Defense Innovation is one of the most popular space-centric ETFs in the market today. Managed by Cathie Wood’s ARK Invest, the fund invests in companies that stand to benefit from advances in space exploration, aerospace tech, and defense innovation.

Some of its biggest holdings are Rocket Lab (6.76%) and SpaceX (7.19%), but it doesn’t have Redwire or ASTS.

Also, I have to make it clear that ARKX is not a pure-play space ETF. It does have AMD (AMD), Google (GOOGL), and Amazon (AMZN) in the mix.

These names may have indirect exposure to autonomy, AI, robotics, logistics, aerospace, or space infrastructure. But that diversification could work in the fund’s favor. The fund is not simply at the mercy of the ebb and flow of the space sector or of negative catalysts that can bring pure-play space ETFs crashing; instead, the presence of AI and tech-adjacent stocks can cushion the blow.

On the other hand, it’s also exposed to the whims of the AI market. Ultimately, the decision to buy the shares will depend on the individual investor’s idea of balance.

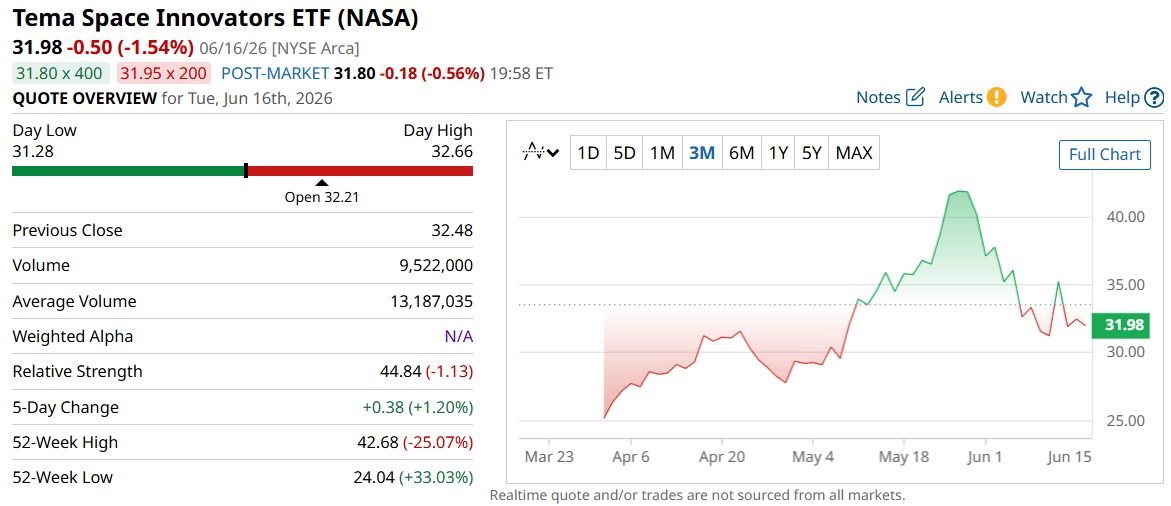

Space ETF #2: Tema Space Innovators ETF (NASA)

But if you really want a pure-play space ETF, or as close to it as possible, there’s also the Tema Space Innovators ETF (NASA). The ETF holds some of the biggest names in the space sector, and all of them are right at the top of their holdings list.

The ETF has a more targeted approach to the overall space economy, focusing on companies advancing space and space-adjacent technologies toward mainstream commercialization, while, of course, investing in the more established firms to provide stability.

More interestingly, it has no problems investing in private companies. In fact, before SpaceX even went public, this ETF had already ~10% of its AUM in private equity. If the fund’s focus remains on the space economy, then we can reasonably expect it to grow alongside it. The only question is how fast and how far the sector can grow.

The space winners may not be the flashiest names

The opportunity in the space sector is real. Launch costs are falling, satellite demand is rising, defense budgets are moving toward space, and companies like SpaceX, Rocket Lab, AST SpaceMobile, and Redwire are attacking the market from very different angles. Meanwhile, ETFs like ARKX offer investors a balanced exposure profile for those looking for built-in diversification.

But this is still a difficult market. Most of these companies are capital-intensive; many are not profitable; timelines can slip; and a single failed launch or delayed contract can change the story quickly.

That doesn’t mean investors should ignore space stocks. It means they need to be selective. The winners probably won’t be the companies with the flashiest vision. They’ll be the ones with real customers, durable funding, strong execution, and a business model that can survive long enough to scale.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)