/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)

Cathie Wood has spent years making one of the biggest bets on Elon Musk through Tesla (TSLA). So, when she recently sold a sizable chunk of Tesla stock, investors immediately took notice. The surprise was not that she was moving money around her portfolio. It was where that money went.

Instead of doubling down on Tesla, Wood turned her attention to another Musk-led company that has suddenly become Wall Street’s newest obsession: SpaceX (SPCX).

The timing is hard to ignore. SpaceX just pulled off the largest IPO in history, raising about $75 billion and attracting an astonishing $250 billion in investor orders. Shares surged 19.6% on their first trading day, pushing the company’s valuation to roughly $2.5 trillion now.

Wood moved quickly to capitalize on the excitement. ARK Invest purchased about 3.29 million shares of SpaceX worth roughly $444 million, while trimming positions in several holdings, including Tesla. The move has set up what some investors are calling the “Battle of the Musks.” Not because Musk is competing against himself, but because one of his biggest supporters appears to be shifting part of her bet from his electric-vehicle empire to his fast-rising space venture.

And when Cathie Wood makes a move like that, Wall Street pays attention. Her trades are closely watched for clues about where she sees the next big opportunity. With many investors wondering what prompted the shift, the answer could offer valuable insight into where she believes the next major wave of value creation in Musk’s empire will come from.

About SpaceX Stock

Founded in 2002, SpaceX started with an ambitious goal of making space travel more affordable and accessible. Today, from its headquarters in Starbase, Texas, the company builds and launches some of the world’s most advanced rockets and spacecraft. Its Falcon and Dragon programs have transformed commercial spaceflight, while Starlink delivers internet service across the globe. Beyond space, SpaceX is increasingly tied to Elon Musk’s broader technology ecosystem, which spans connectivity, AI, and next-generation digital infrastructure.

SpaceX’s stock market debut could hardly have gone better. After pulling off the largest IPO in history, shares of Elon Musk’s space and AI company surged 19.6% during their first full trading session. The rally was fueled by strong demand from both institutional and retail investors, instantly lifting SpaceX’s market value to roughly $2.5 trillion.

Investors credited the successful launch to a well-executed IPO process, robust demand, and, of course, Musk’s track record of building companies that capture Wall Street’s imagination. Yet beneath the excitement, a debate is already emerging. Are investors buying SpaceX for its long-term business prospects, or simply trading one of the market’s hottest new stocks? Todd Schoenberger, chief investment officer at Crosscheck Management, believes much of the activity may be driven by traders rather than long-term investors. That distinction could become important as the stock settles into life as a public company.

The shares did give back some gains after SpaceX announced plans to acquire Anysphere, the company behind the AI coding platform Cursor, in a deal valued at $60 billion. Still, investor enthusiasm remains strong.

The next catalyst could arrive quickly. Options trading is expected to begin as early as Tuesday, potentially bringing higher trading volumes and increased volatility. Meanwhile, SpaceX plans to gradually unlock shares for resale before the traditional six-month post-IPO lockup period expires. Rather than releasing a large block of stock all at once, the company will use a staged approach tied to performance targets.

Adding another layer of stability is the IPO's greenshoe option, a mechanism designed to reduce extreme price swings during the stock's early weeks.

Cathie Wood Makes a Big Bet on SpaceX

Cathie Wood did not waste much time after SpaceX’s blockbuster market debut. According to ARK Invest’s daily trading disclosures, the firm scooped up about 3.29 million SpaceX shares across four of its flagship ETFs, signaling a strong vote of confidence in Elon Musk’s newly public company.

The biggest purchase came from the ARK Innovation ETF (ARKK), which bought 1.69 million shares, giving the stock a 4.3% weighting in the fund. The ARK Autonomous Technology & Robotics ETF (ARKQ) followed with 736,442 shares, making SPCX 6.25% of the ETF’s weight. Meanwhile, the ARK Space Exploration & Innovation ETF (ARKX) purchased 538,341 shares, giving a weight of 7.19% to SPCX. The ARK Next Generation Internet ETF (ARKW) purchased another 308,636 shares, with SpaceX’s shares carrying a 3.38% of weightage.

The aggressive buying came even as some analysts cautioned that SpaceX’s valuation looks stretched. Still, Wood’s move suggests she sees significant long-term potential in the company’s growing presence across space, connectivity, and AI.

Behind the Revenue Growth and Rising Losses at SpaceX

A closer look at SpaceX’s financials shows a company that’s firmly in growth mode. Rather than focusing on maximizing profits today, management is pouring billions of dollars into building what it hopes will become a much larger business in the years ahead.

For the first quarter ended March 31, 2026, SpaceX generated $4.7 billion in revenue, up 15.4% year-over-year (YOY). The growth was driven primarily by an expanding Starlink subscriber base and increasing demand for AI-related products, including X and Grok subscriptions. Those gains were partially offset by slower growth in the Space segment, where fewer launch missions and the timing of government contracts weighed on results.

The bigger story, however, was spending. SpaceX reported an operating loss of $1.94 billion and a net loss of $4.3 billion during the quarter. Yet the company still produced $1.1 billion in adjusted EBITDA, highlighting the strength of its underlying operations. Much of the red ink came from massive investments. In Q1 alone, SpaceX spent $7.7 billion on its AI business, far exceeding the $1.33 billion invested in Connectivity and the $1.05 billion directed toward its Space operations.

The trend was similar throughout 2025. SpaceX generated $18.7 billion in revenue and $6.58 billion in adjusted EBITDA but posted a $2.6 billion operating loss and a $4.9 billion net loss. Capital expenditures reached extraordinary levels, including $12.7 billion for AI infrastructure, $4.18 billion for Connectivity, and $3.8 billion for Space.

In short, SpaceX is not losing money because demand is weak. It is losing money because it is spending aggressively to expand AI computing, grow Starlink, and strengthen its space business in pursuit of much bigger opportunities down the road.

SpaceX Is Becoming Much More Than a Space Company

One of the biggest takeaways from SpaceX’s S-1 filing was about AI. For years, investors viewed SpaceX primarily as a space company. But the latest filing suggests management increasingly sees the business as an AI infrastructure provider positioned to benefit from the massive surge in demand for computing power. More importantly, it already has customers willing to pay for that capacity.

The headline deal involves Google’s parent, Alphabet (GOOG) (GOOGL). Starting in late 2026, Google is expected to pay roughly $920 million per month to access SpaceX’s AI computing infrastructure, including around 110,000 Nvidia (NVDA) GPUs. That works out to more than $11 billion in annual revenue from a single customer.

Google is not the only one knocking on SpaceX’s door. The company has also signed a major AI infrastructure agreement with Anthropic. Combined, the two contracts are expected to generate about $26 billion in annual revenue and more than $70 billion over their lifetimes if executed as planned. Remarkably, those two AI deals alone could eventually bring in more revenue than SpaceX generated across its entire business in 2025.

The Google agreement is particularly noteworthy because Google is already one of the world’s largest builders of AI infrastructure. The fact that it is turning to SpaceX for additional computing capacity suggests demand for AI services is growing faster than even the industry’s biggest players can satisfy.

The filing also revealed another intriguing asset – SpaceX owns 18,712 Bitcoin (BTCUSD), worth well over $1 billion at current prices. That gives investors exposure not only to space exploration, satellite connectivity, and AI infrastructure, but also to cryptocurrency.

Wall Street's Take on SpaceX After the IPO

SpaceX’s stunning post-IPO rally has pushed its market cap above $2.5 trillion, but not everyone on Wall Street is convinced the numbers add up. According to satcom and wireless spectrum consultant Tim Farrar, much of the stock’s surge reflects investor faith in Elon Musk’s vision rather than the company’s current financial performance.

Farrar argues that SpaceX’s launch business, Starlink satellite internet network, and emerging AI initiatives do not yet justify a multi-trillion-dollar valuation on their own. Instead, investors appear to be betting that Musk can unlock entirely new growth opportunities and dramatically expand the company’s revenue base over the next several years.

That optimism is tied closely to Musk’s bold forecast that SpaceX could generate $1 trillion in annual revenue by 2030. To get there, however, the company would need to increase revenue roughly 50-fold from current levels, a challenge that even supporters acknowledge is ambitious.

Still, Farrar remains impressed by SpaceX’s competitive position. He noted that the company has achieved things in the space industry that rivals have struggled to match, even those with deep pockets. While questions remain about valuation, many analysts agree that SpaceX remains the clear leader in satellite internet and space infrastructure. The real debate is whether those markets can grow large enough to support Musk’s trillion-dollar ambitions.

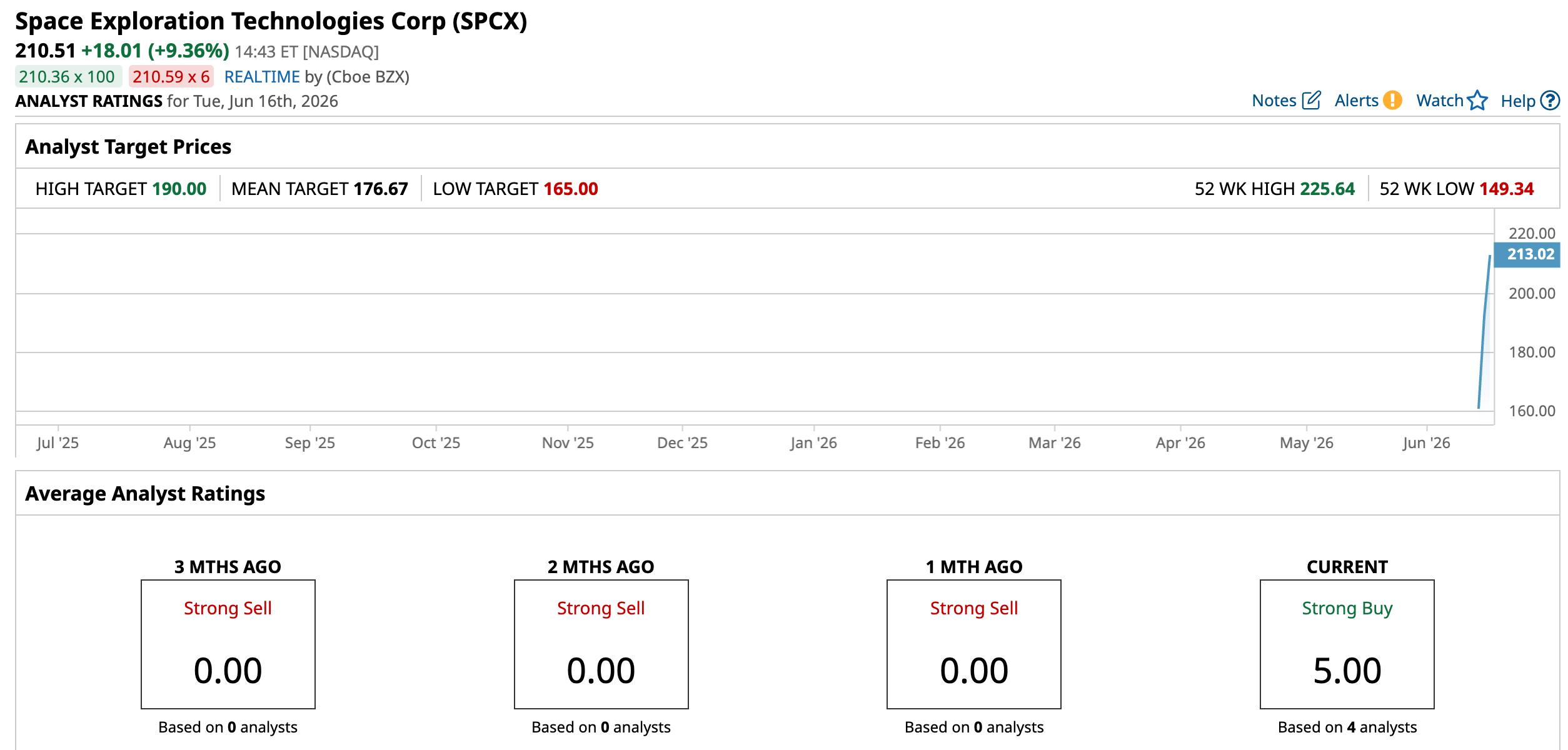

When analysts initiated coverage ahead of SpaceX’s IPO, price targets ranged from $165 to $195 per share. The stock quickly raced past New Street’s $165 target and briefly topped Wolfe Research’s $175 target during its first trading sessions. Shares remain within reach of Oppenheimer’s $195 target.

The most ambitious outlook comes from New Street. While its base-case valuation supports SpaceX’s market value, the brokerage firm outlined a long-term bull-case scenario of $330 per share by 2040. That projection assumes a $20 trillion space economy, with SpaceX capturing half the market.

New Street estimates SpaceX would need nearly $127.7 billion in AI revenue and $57.9 billion in connectivity services revenue by 2030, implying roughly 60% annual revenue growth over the next five years. And $9.7 billion in revenue is projected from space operations in 2030.

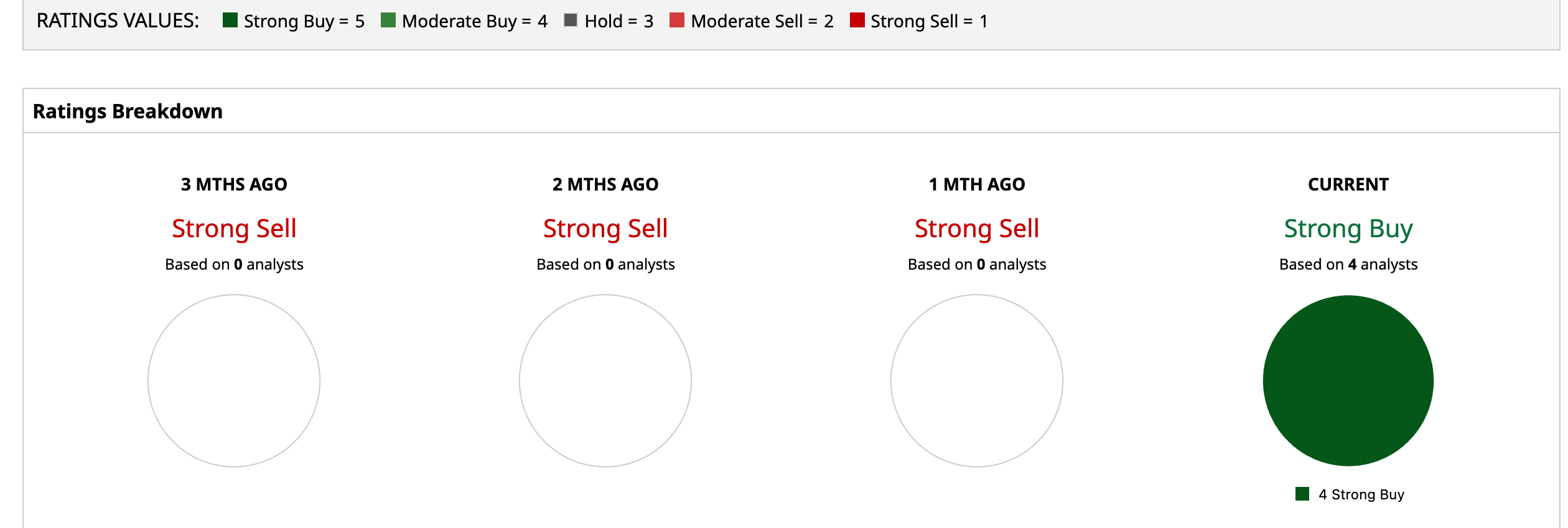

While opinions differ on how quickly SpaceX can grow into its valuation, analyst sentiment remains firmly bullish. SPCX currently has a unanimous “Strong Buy” rating from all four analysts covering the stock.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)