For nearly a century, Eversource Energy (ES) has been helping keep the lights on. Headquartered in Springfield, Massachusetts, the utility giant serves about 4.4 million customers with electricity and natural gas (NGN26) across Connecticut, Massachusetts, and New Hampshire. With a market cap of $26.2 billion, Eversource has grown into one of the region’s most important energy providers, operating an extensive network that powers homes, businesses, and communities every day.

That scale is a big reason Eversource wears the “large-cap” label. A customer base of millions, predictable revenue from regulated utility operations, and a dominant presence across New England have helped the company build a market capitalization well above the $10 billion threshold. Eversource has also sharpened its focus by exiting non-core businesses such as offshore wind and water utilities, strengthening its balance sheet and reinforcing its position as a stable, long-term player in the utility sector.

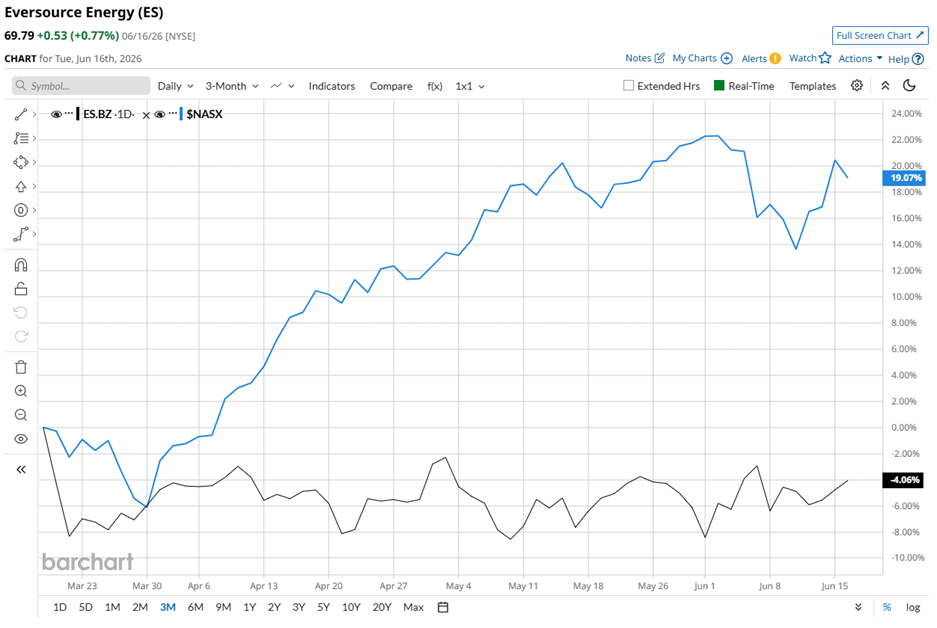

While the utility giant remains a dominant player, its stock has struggled to keep pace with the broader market. Shares are down 8.4% from their 52-week high of $76.41. Plus, ES stock dipped 3.7% over the past three months, trailing the Nasdaq Composite’s ($NASX) 17.7% surge during the same period.

So far in 2026, Eversource’s shares have delivered a modest 3.7% gain, but that performance looks a lot less impressive when stacked against the Nasdaq’s 13.8% year-to-date (YTD) rally. Taking a wider view, the gap becomes even more noticeable. Over the past 52 weeks, ES stock has climbed 10.4%, while the tech-heavy Nasdaq has raced ahead with a 35.5% return.

Adding to the cautious sentiment, the stock remains stuck below both its 50-day and 200-day moving averages, suggesting investors are still waiting for a stronger catalyst before getting fully back on board.

The main issue is that Eversource is facing headwinds on several fronts at once. The company recently lowered its 2026 profit outlook after federal regulators approved lower electricity transmission rates in New England, a decision CEO Joe Nolan criticized as “arbitrary and flawed.”

Meanwhile, the completion of its $2.4 billion water utility sale also weighed on earnings expectations. As a result, Eversource now expects adjusted EPS of $4.57 to $4.72, down from its previous forecast of $4.80 to $4.95.

Adding to the challenge, Eversource continues to spend heavily on grid upgrades as electricity demand rises from electrification trends and the rapid buildout of data centers. Those investments are necessary for long-term growth, but higher financing costs and regulatory pushback have made the road a bit bumpier, leaving investors waiting for clearer signs that the company's spending today will translate into stronger returns tomorrow.

By comparison, ES has slightly outpaced rival PPL Corporation (PPL), whose shares have gained 8.1% over the past 52 weeks and 3.3% so far in 2026.

Analysts are overall cautious on ES stock. The stock has a consensus “Hold” rating from the 16 analysts covering it. That’s a downgrade from the “Moderate Buy” rating two months back. The mean price target of $72.55 suggests a potential upside of 4.3% from current price levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)