With a market cap of $28.2 billion, CenterPoint Energy, Inc. (CNP) is a public utility holding company, operating across Electric, Natural Gas, and Corporate segments. It provides electric transmission and distribution services in Indiana, along with natural gas sales, transportation, and distribution to residential, commercial, and industrial customers across several U.S. states.

Companies valued at $10 billion or more are generally considered “large-cap” stocks, and CenterPoint Energy fits this criterion perfectly. The company serves millions of customers and maintains extensive infrastructure, including substations and intrastate pipelines.

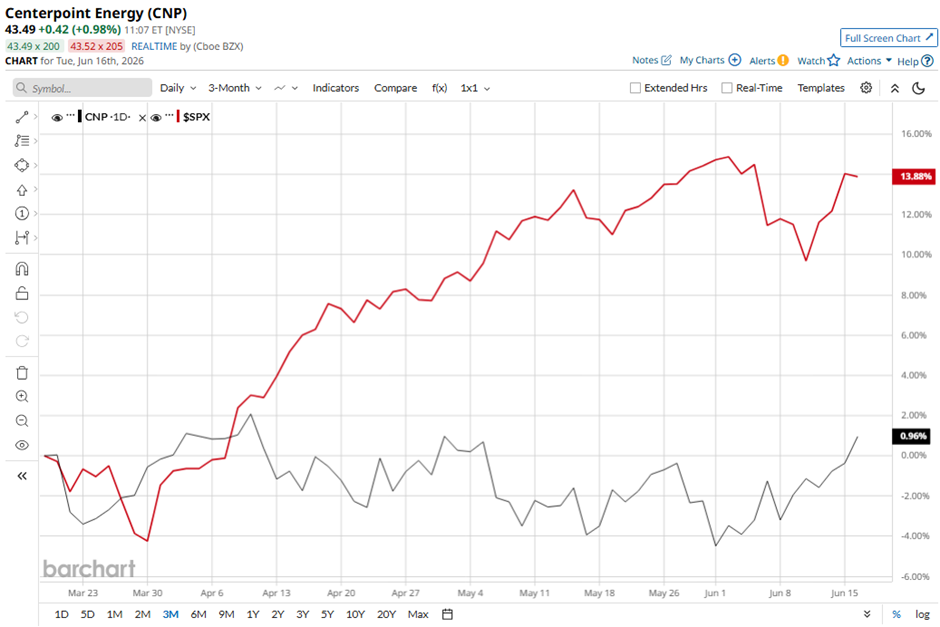

Shares of the Houston, Texas-based company have fallen 2.3% from its 52-week high of $44.47. CNP stock has decreased 1.3% over the past three months, lagging behind the S&P 500 Index’s ($SPX) 12.7% gain during the same period.

Longer term, the stock has returned 21.1% over the past 52 weeks, underperforming the 25.1% return of the SPX over the same time frame. However, CenterPoint Energy’s shares have gained 13.6% on a YTD basis, exceeding SPX's 10.3% rise.

The stock has been trading above its 200-day moving average since last year.

Shares of CenterPoint Energy rose 2.5% on Apr. 23 after the company reported strong Q1 2026 results, with adjusted EPS increasing to $0.56, driven primarily by growth and regulatory recovery that contributed $0.11 per share of favorable earnings impact. Investors were further encouraged by management's decision to reaffirm its 2026 adjusted EPS guidance of $1.89 - $1.91, with the midpoint implying approximately 8% earnings growth over 2025 results.

The stock also benefited from a major growth update at Houston Electric, where CenterPoint announced 12.2 gigawatts of firmly committed industrial load and increased its data centre outlook to 8 gigawatts, expected to be energised by 2029, including 3.5 gigawatts already under construction.

In comparison, rival The Southern Company (SO) has lagged behind CNP stock. SO stock has returned 8.7% on a YTD basis and 6.6% over the past 52 weeks.

Despite the stock’s underperformance relative to the SPX over the past year, analysts are moderately optimistic with a consensus rating of "Moderate Buy" from 18 analysts. The mean price target of $46.06 is a premium of 5.9% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)