/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

Autodesk Inc. (ADSK) stock has tanked recently, spurring unusually large put option activity today in this software company stock. But is ADSK too cheap? After all, its free cash flow and FCF margins are very high. In fact, ADSK could be worth 22% more at $242 per share.

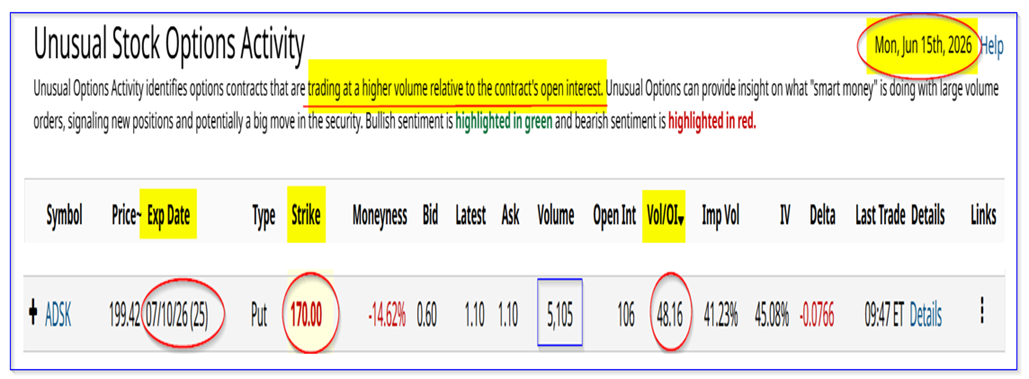

ADSK is at $198.78 in midday trading today, bouncing up from a 1-year trough of $198.30 on June 12. That could be why some investors are selling short huge amounts of out-of-the-money puts today.

This can be seen in today's Barchart Unusual Stock Options Activity Report. It shows that over 5,100 put option contracts have traded at the $170.00 strike price expiring July 10.

That strike price is also $30 below today's price, i.e., “out-of-the-money," or -15% below. Nevertheless, the midpoint is still $0.85, with $1.10 at the latest.

This means an investor who shorts this particular put contract, after securing $17,000 with their brokerage firm per put contract shorted, will immediately receive $85 in their account.

That works out to a three-week yield of 0.5%, and the investor has a potential buy-in point of $170-$0.85, or $169.15. That is 15.4% below today's price, an attractive entry point.

That is especially since Autodesk reported strong free cash flow (FCF) and FCF margins recently, as well as a strong FCF outlook.

Strong FCF Results and Acquisition

On May 28, Autodesk reported that its FY27 Q1 (ending April 30) rose 18% YoY to $1.934 billion. Moreover, its Q1 FCF hit $876 million, up 57.6%, representing 45.3% of its quarterly revenue.

That FCF margin was significantly higher than the year-ago FCF margin of just 34.05%, according to Stock Analysis. Its trailing 12-month (TTM) FCF was $2.729 billion, representing 36.35% of TTM revenue, a peak over the past 4 quarters.

However, also on May 28, the company announced a large acquisition of another software company in the maintenance management arena, which is different from Autodesk's typical design and utility type consumer software entities.

The market did not like this acquisition, which will cost $3.6 billion in cash, which Autodesk will fund through its own cash resources and borrowing. The latter is probably why the market did not like this, and ADSK fell.

FCF Forecasts

Nevertheless, Autodesk is one of the few companies that forecasts its free cash flow. They announced a forecast for FY27 (ending Jan. 2027) FCF between $2.725 billion and $2.8 billion, on a revenue forecast between $8.505 billion and $8.580 billion.

So, at the midpoint of each forecast, Autodesk's FCF margin will be 32.3%:

$2.7625b / $8.5425 billion = 0.3234

That is slightly lower than its TTM FCF margin of 36.35%.

However, analysts project a higher revenue of $9.7 billion for next year (ending Jan. 28). As a result, if management can maintain a 36.35% FCF margin, as it has over the past year:

$9.7b x 0.3635 = $3.53 billion FCF forecast

As a result, the FCF forecast this year by management ($2.76 billion) and analysts' forecasts for next year ($3.53b) will average $3.145 billion over the next 12 months (NTM).

Analysts can use this NTM FCF forecast to set a fair market value for ADSK stock.

ADSK Stock Price Targets

Yahoo! Finance shows that the Autodesk stock market cap today is $42.134 billion. That means if the company were to pay out 100% of its TTM FCF as a dividend, the yield would be 6.50%:

$2.729b / $42.134 billion = 0.0648 = 6.5% TTM FCF yield

As a result, applying this to the $3.145 billion NTM FCF:

$3.145b / 0.065 = $48.39 billion fair market value (FMV)

That is 14.8% higher than today's market cap of $42.134 billion. In other words, the ADSK price target is almost 15% higher:

$198.78 x 1.148 = $228.20 per share price target (PT)

Moreover, using analysts' FY28 revenue forecasts and the $3.53 billion FCF forecast, the market value and price targets (PT) are 29% higher:

$3.53b / 0.065 = $54.31 billion FMV, or +28.9%

$198.78 x 1.289 = $256.23 PT

So, the average PT of these two is $242.22, or +21.8% higher.

Analysts' PTs are Significantly Higher

Moreover, analysts have significantly higher PTs. For example, Yahoo! Finance shows that the average of 33 analysts is $319.27 per share. Barchart's mean analyst survey PT is $329.71.

Anachart's survey of 27 analysts is $330.24. AnaChart typically surveys more recent analyst recommendations than other surveys, so its survey tends to be more accurate.

The bottom line is that analysts have PTs 60% to 66% above today's price, much higher than my forecast. They may be assuming a better FCF yield metric, assuming the market improves the multiple.

For example, using a 6.0% FCF yield, instead of my 6.5% yield based on its historical metric, improves my FY 28 price target to a 40% higher price target ($277.50):

$3.5b / 0.06 = $58.83 billion fair market value (FMV)

$58.83 / $42.134 mkt cap today = 1.396

1.396 x $198.78 price today = $277.50 per share PT

Summary and Conclusion

The bottom line is that just a small increase in the valuation metric results in a huge increase in the price target. Going from 6.5% to 6.0% (less than a 10% move) led to a doubling of my PT.

This may also be why some investors today are shorting deep out-of-the-money (OTM) puts in ADSK. They are able to earn income for the next 3 weeks while setting up a potential lower buy-in.

Moreover, it's highly likely that sophisticated investors are using that short-put income to help fund at-the-money (ATM) or in-the-money (ITM) call options at later expiry periods. That way, they can gain exposure to any upside in ADSK, as shown by its higher price targets, at a lower cost.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)