/Tecnology%20grey%20and%20black%20laptop%20on%20surface%20by%20Ales%20Nesetril%20via%20Unsplash.jpg)

Intel Corporation (INTC) is a Santa Clara-based global semiconductor and technology giant founded in 1968 and the inventor of the world's first commercial microprocessor. Intel is executing one of the most ambitious corporate turnarounds in technology history, reinventing itself as an AI-era CPU and foundry powerhouse.

AI-driven business lines now account for approximately 60% of Intel's revenue, up 40% year-over-year (YoY), while landmark partnerships with Nvidia (NVDA), Alphabet's (GOOG) (GOOGL) Google, Tesla's (TSLA) Terafab project, and a $5 billion U.S. government commitment are supercharging its manufacturing revival. With Intel 18A yields ahead of expectations and 14A design commitments emerging in H2 2026, Intel's foundry comeback story is rapidly shifting from narrative to execution.

Intel Stock's Stellar Run

INTC stock has delivered a staggering total return of approximately 485% over the past 12 months, with a year-to-date (YTD) total return of approximately 230% in 2026, placing it firmly in the top 1% of all S&P 500 ($SPX) performers, while the broader index returned approximately 22% over the past year. The best single trading day came on April 24, 2026, when INTC surged 23.6% following its blowout Q1 earnings, breaking through its dot-com era all-time high for the first time since the year 2000.

Against the S&P 500 Information Technology Index ($SRIT), INTC has dramatically outpaced the broader tech sector in 2026, marking one of the most breathtaking single-year recoveries in large-cap semiconductor history.

Intel Posted Strong Results

Intel reported Q1 2026 revenue of $13.6 billion, up 7% YoY, surpassing analyst consensus of $12.36 billion by approximately $1.2 billion, marking its sixth consecutive quarter of exceeding its own guidance, while non-GAAP EPS of $0.29 obliterated the Street estimate of $0.01 by a staggering $0.28. Data Center and AI revenue surged 22% YoY to $5.1 billion, beating the $4.41 billion estimate, while Intel Foundry revenue rose 16% to $5.4 billion, with Xeon 6 selected as the host CPU for NVIDIA's DGX Rubin NVL8 systems, a pivotal AI infrastructure design win.

Non-GAAP gross margin came in at 41.0%, a remarkable 650 basis points above guidance, reflecting improved manufacturing yields, pricing actions, and a richer product mix. On a GAAP basis, Intel reported a net loss of $0.73 per share, primarily driven by $4.07 billion in restructuring charges, including a goodwill impairment at Mobileye (MBLY). Intel repurchased its 49% Ireland Fab 34 minority interest from Apollo Global for $14.2 billion, consolidating full ownership of a critical advanced manufacturing asset as it accelerates its domestic foundry buildout.

For Q2 2026, Intel guided revenue of $13.8–$14.8 billion, far ahead of the $13.03 billion analyst consensus, and non-GAAP EPS of $0.20 versus the $0.09 Street estimate. CEO Lip-Bu Tan stated, "The next wave of AI will bring intelligence closer to the end user, moving from foundational models to inference to agentic. This shift is significantly increasing the need for Intel's CPUs and wafer and advanced packaging offerings." Tan added that agentic AI is pushing the total addressable chip market toward $1 trillion and that Intel is uniquely positioned to capture share as the CPU reasserts itself as the indispensable foundation of the AI era.

Intel Upgraded by BofA

Intel shares surged approximately 6% in premarket trading and are currently about 5% up in morning trading today after Bank of America delivered a double upgrade, moving the stock to “Buy” from “Underperform,” and raised its price target to $135 from $96, signaling an upside of 17% from the market rate. Analyst Vivek Arya cited growing confidence in Intel's ability to address industry-wide constraints in leading-edge wafer and advanced packaging capacity, alongside a significantly expanded agentic CPU total addressable market opportunity.

BofA now projects Intel's integrated device manufacturer earnings power at $6-plus per share by CY2030, up from its prior $3–$4 estimate, pointing to Cadence's 14A node IP sign-up and Terafab engagements as key data points reinforcing Intel's long-term external foundry credibility and ecosystem sustainability.

Should You Get INTC Stock?

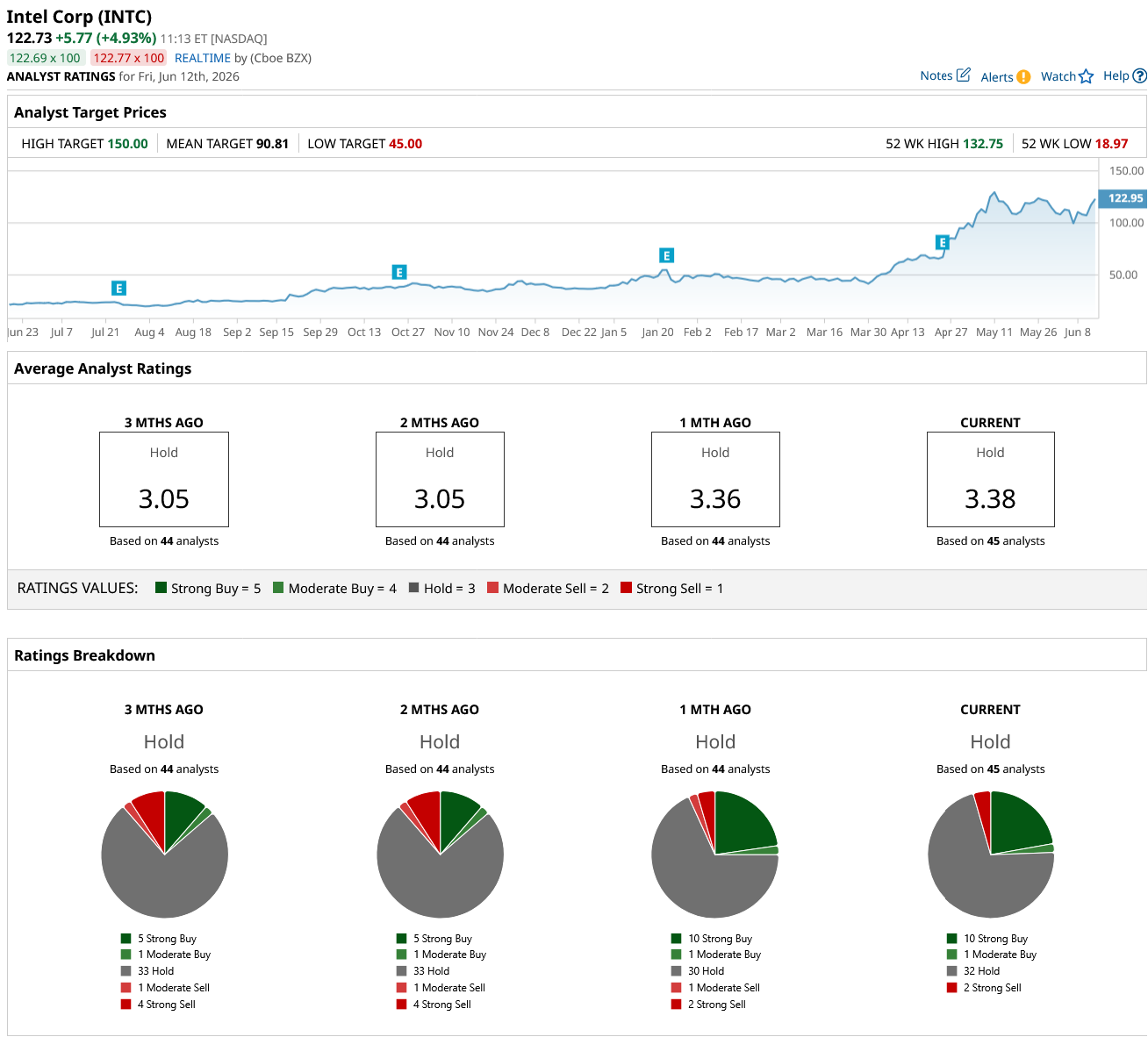

BofA's double upgrade to “Buy” with a $135 price target is a significant de-risking moment for Intel, reflecting growing institutional conviction in its agentic CPU and foundry opportunity. However, the broader Wall Street consensus remains firmly cautious. INTC stock carries a "Hold" rating across 45 analyst ratings, comprising 10 "Strong Buy," one "Moderate Buy," 32 "Hold," and two "Strong Sell," with a mean price target of $90.81, implying approximately 26% downside from current levels.

For investors, INTC is a high-conviction turnaround story, but one where the stock's extraordinary 230% YTD run demands disciplined patience and selective entry points.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)