Only a handful of artificial intelligence (AI) companies are poised to dominate the next decade. Here are two names that stand out for their strong growth, expanding competitive advantages, and ability to capitalize on the massive AI infrastructure boom.

Let's take a closer look.

Top AI Stock #1: Microsoft (MSFT)

Unlike many new AI companies that are still in early monetization stages, Microsoft’s (MSFT) AI business is already generating steady, massive revenue. Microsoft is investing heavily in developing custom AI chips, cloud infrastructure, enterprise software, AI agents, developer tools, and productivity applications. This diversification could make Microsoft harder to disrupt over time.

Microsoft’s AI business surpassed $37 billion in annual revenue run rate in the third quarter of fiscal 2026, signifying a 123% year-over-year (YOY) increase. The cloud business, powered by Azure, remains one of the main reasons why the firm could be positioned for long-term AI dominance. Despite ongoing supply constraints, Azure and other cloud services revenue surged 40% YOY in the quarter. Notably, Microsoft Cloud revenue climbed to $54.5 billion during the quarter, up 29% YOY. Due to the aggressive demand, the company is now working to double its overall infrastructure footprint within the next two years.

While emerging AI players like Nebius (NBIS) are grabbing attention with eye-popping 684% growth, Microsoft continues to deliver double-digit gains every quarter. But that kind of sustained, predictable growth quarter after quarter at such a massive scale is a clear sign of a high-quality business. Total revenue jumped 18% YOY to $82.9 billion in Q3, while EPS surged 21% to $4.27 in the quarter.

The company expects to spend over $190 billion in capital expenditures in 2026 as it expands data-center capacity and AI infrastructure globally. At the end of the quarter, Microsoft had $78 billion in cash balance and more than $15 billion in free cash flow. Very few companies possess the financial strength to keep investing aggressively in AI infrastructure while retaining consistent growth.

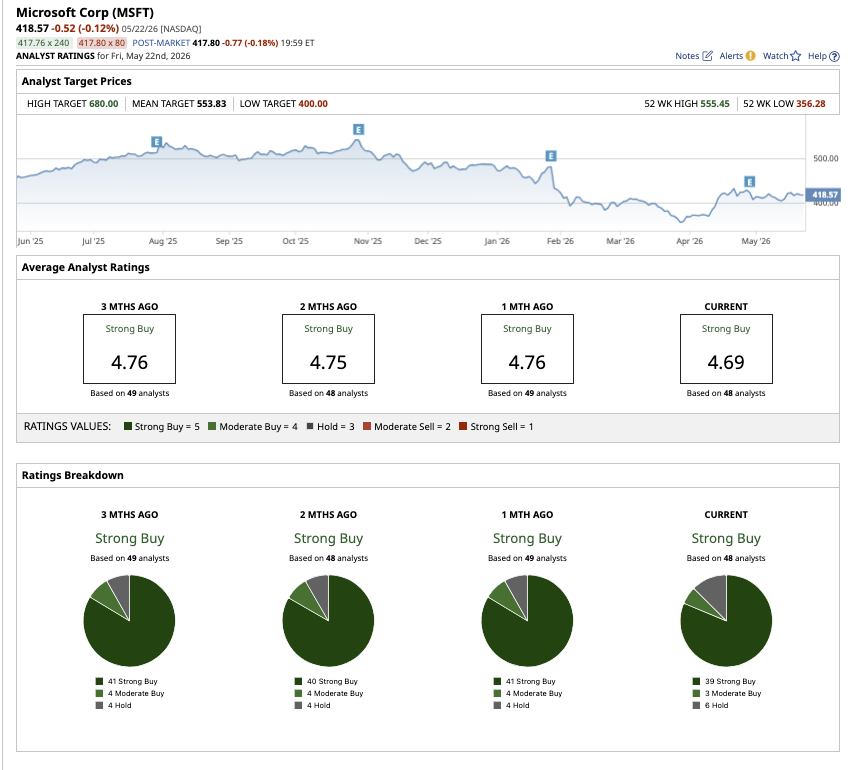

Microsoft is controlling multiple layers of the AI ecosystem while maintaining consistent profitability. This could be the major reason why it is poised to be the biggest long-term AI winner in the next decade. Despite the consistent growth, MSFT stock is down 14% year-to-date (YTD), underperforming the Nasdaq Composite's ($NASX) gain of 15%. Nonetheless, Wall Street expects potential upside of 33% from current levels based on the average target price of $553.83. Additionally, the high price target of $680 implies that the stock could climb as much as 64% from here.

On Wall Street, MSFT stock has a consensus “Strong Buy” rating. Of the 48 analysts tracking the stock, 39 have a "Strong Buy" rating, three have a "Moderate Buy," and six offer a “Hold” rating.

Top AI Stock #2: Lam Research (LRCX)

Lam Research (LRCX) makes the machines and equipment used to manufacture semiconductor chips. Its tools help chipmakers produce advanced memory and AI chips through processes like etching, deposition, and wafer fabrication. LRCX stock is finally getting the attention it deserves, with shares up 87% YTD, massively outperforming the broader market.

Lam Research’s business is a critical part of chip manufacturing. But Lam is not simply growing alongside the semiconductor industry; it is capturing a larger portion of industry spending. Lam mostly serves major semiconductor manufacturers building NAND, DRAM, and AI-related chips. As AI systems scale, massive amounts of data storage are required across hyperscale data centers, creating massive demand for NAND, DRAM and high-bandwidth memory (HBM) products.

As a result, Lam now projects worldwide wafer fabrication equipment (WFE) spending to climb to roughly $140 billion. The company expects its served available market (SAM) exposure to rise slightly above the mid-30% range of total WFE spending in 2026. If that happens, Lam will stay on track to achieve its goal of reaching the high-30% range over the next few years.

During the March quarter, revenue climbed 24% YOY to $5.8 billion, while adjusted EPS rose 41% YOY to $1.47 per share, with both beating consensus estimates. The Foundry business represented 54% of systems revenue during the quarter. Lam is heavily benefiting from accelerating NAND conversion spending, strong DRAM demand, expanding HBM investments, advanced packaging growth, and rising service revenue from its vast installed equipment base. Lam Research may ultimately become one of the most important long-term AI infrastructure winners.

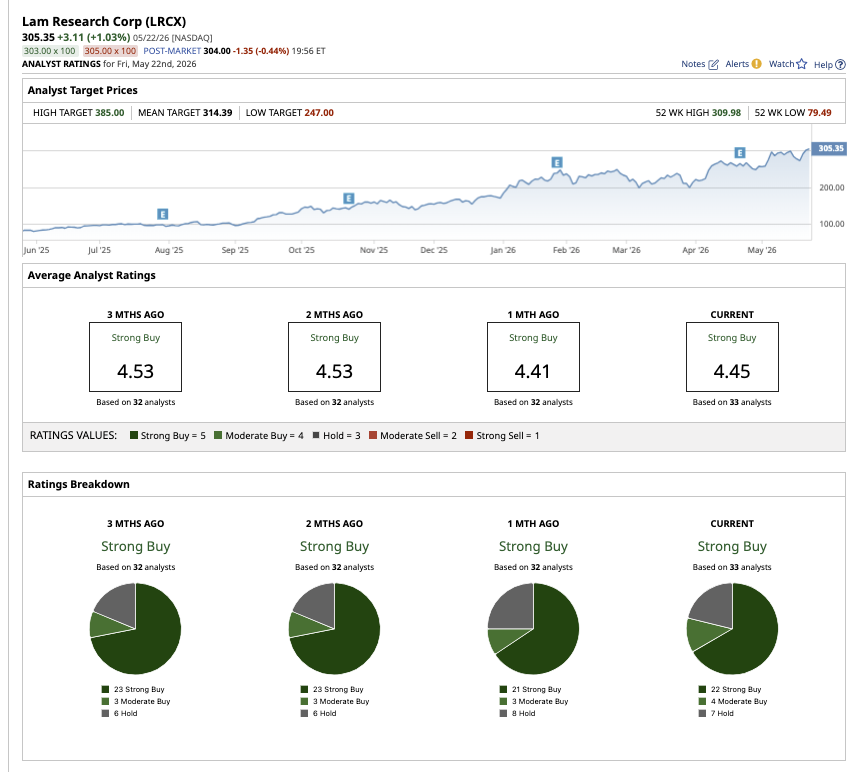

On Wall Street, LAM stock has an overall “Strong Buy” rating. Of the 33 analysts covering the stock, 22 offer a “Strong Buy” rating, four have a “Moderate Buy” rating, and seven analysts offer a “Hold” rating. Based on the average target price of $314.39, shares have potential downside of 2% from current levels. However, the Street-high price estimate of $385 implies that shares could rally as much as 20% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)