/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

The tech earnings season has kicked off with a bang, as two of the world’s most influential companies released earnings on April 29. The race to dominate artificial intelligence (AI) is heating up fast, with Meta Platforms (META) and Microsoft (MSFT) both pouring billions to build the future.

The big question now is which of these two “Magnificient Seven” stock is the better buy today — and better positioned to win over the next decade?

The Case for Meta Platforms

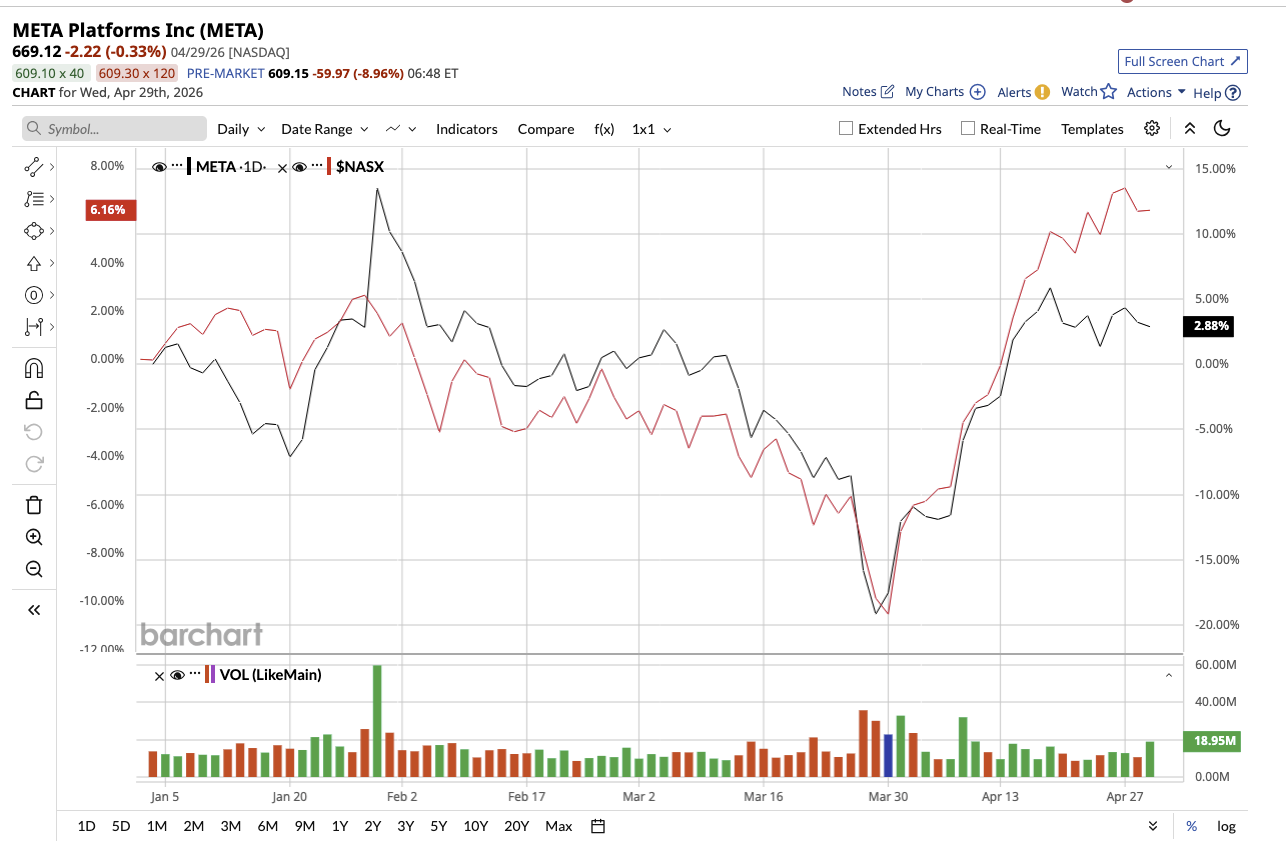

With a market capitalization of $1.54 trillion, Meta Platforms owns Facebook and Instagram, among other social media platforms. Meta Platforms has entered fiscal 2026 with strong momentum, showcasing the power of its advertising engine and the scale of its AI ambitions. META stock is down 7% year-to-date (YTD), trailing the tech-heavy Nasdaq Composite's ($NASX) gain of 8%.

Revenue in the first quarter jumped 33% year-over-year (YOY) to $56.3 billion. The bulk of this came from Meta's Family of Apps segment (all of its social media platforms), which generated $55.9 billion in revenue, up 33% YOY, with ad revenue alone contributing $55 billion, also up 33% YOY. Adjusted EPS increased by 62% to $10.44 per share. Meta’s biggest advantage is scale. Around 3.5 billion people use at least one of its apps daily, and AI is now deeply embedded across all of its social media platforms. However, this figure saw a slight dip in March due to internet disruptions in Iran and restrictions in Russia.

Meta continues to invest heavily in hardware and infrastructure to support its AI vision. It is deploying over 1 gigawatt of custom silicon developed with Broadcom (AVGO), alongside Advanced Micro Devices (AMD) and Nvidia (NVDA) systems, while expanding its global data-center footprint.

However, not everything is rosy. The biggest concern is still Reality Labs. Despite billions in investments, the segment still operated at a loss of $4 billion in Q1. It generated just $402 million in revenue, down 2% YOY, showing that VR is still not a meaningful contributor. While AI glasses are gaining traction, Quest headset sales declined in the quarter. Looking down 10 years from now, the Reality Labs segment might start generating profits, but that is a hope and not a guarantee. At the moment, it remains a major drag. Management’s capital allocation to this segment now raises concerns as it continues to weigh on overall profitability.

Meta is targeting between $125 billion and $145 billion in capital expenditures in fiscal 2026. Free cash flow stood at $12.4 billion in Q1, and the company ended the quarter with $81.2 billion in cash and marketable securities against $58.7 billion in debt.

All in all, Meta is executing exceptionally well in its core advertising business while aggressively building for an AI-driven future. The opportunity is massive, but so are the risks. The company’s ability to balance profitability with continued investments in Reality Labs will be critical in determining whether these bold bets ultimately pay off in a decade.

On Wall Street, META stock has a consesnus “Strong Buy” rating with an average target price of $853.87, which implies potential upside of 40% from current levels. Of the 56 analysts tracking the stock, 44 rate it as a "Strong Buy," three as a "Moderate Buy," and nine as a "Hold." The high price target of $1,015 implies that the stock could go up as much as 66% from its current levels.

The Case for Microsoft

Valued at $3 trillion by market cap, Microsoft is a diversified technology company that makes money from software, cloud computing, and enterprise services. Its legacy products include Microsoft 365, Windows, LinkedIn, Xbox, Edge, and Bing, with Microsoft Azure ranked among the top three global cloud computing platforms.

In Q3 fiscal 2026, Microsoft proved why it is a must-own tech stock. Revenue jumped 18% YOY to $82.9 billion, with Microsoft Cloud contributing $54.5 billion, up about 29% YOY. Its AI business alone has now crossed a $37 billion annual revenue run rate, increasing 123%.

Azure remains key to its growth story, with revenue climbing around 40%. Management noted that demand is so strong for Azure that it’s still outpacing available capacity. Hence, Microsoft is rapidly expanding its infrastructure, adding another gigawatt of capacity this quarter and aiming to double its data-center footprint in the next two years. Microsoft spent $31.9 billion on capex in the quarter, with two-thirds allocated to short-lived assets like GPUs and CPUs. Even with massive AI investments, Microsoft is still highly profitable. Adjusted EPS rose 21% in the quarter.

What makes Microsoft stand out is its full-stack approach. It owns everything from cloud infrastructure and AI models to enterprise software, security, and developer tools and is now monetizing AI across its ecosystem. Its Foundry platform gives businesses access to a variety of models, including OpenAI, Anthropic, and open-source options, while Fabric combines enterprise data into a unified intelligence layer. Around 15,000 clients now use both Foundry and Fabric, a 60% YOY increase.

Meanwhile, products like Microsoft 365, LinkedIn, and GitHub create recurring, subscription-based revenue streams, making the business more predictable and resilient. Segment-wise, Productivity and Business Processes grew in the high teens, led by Microsoft 365 and Copilot, while Intelligent Cloud revenue increased around 30%, with Azure leading the way. Meanwhile, More Personal Computing revenue dipped slightly due to weakness in Windows OEM and gaming. However, Microsoft's diversification has allowed it to not rely on just one business to drive growth over the last decade.

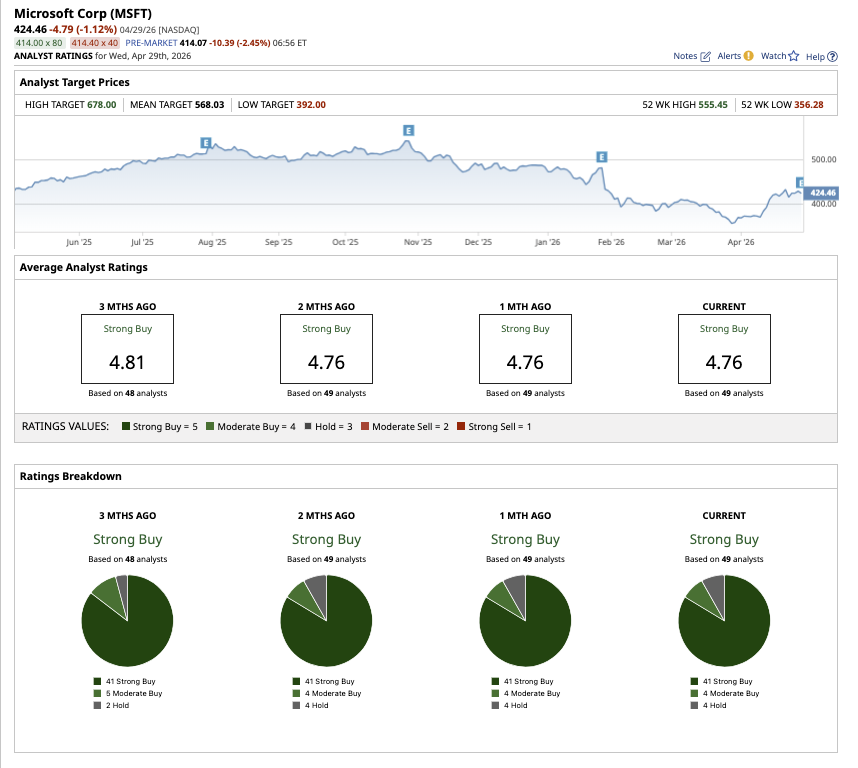

On Wall Street, the consensus on MSFT stock is a “Strong Buy” rating. Of the 49 analysts tracking the stock, 41 have a "Strong Buy" rating, four have a "Moderate Buy," and four offer a “Hold” rating. MSFT stock has fallen 14% YTD, underperforming the Nasdaq Composite. Yet, Wall Street expects potential upside of 36% from current levels, based on the average target price of $565.91. The high price target of $678 implies that the stock could climb 63% from current levels.

Which Is the Better Buy Now?

Both Meta and Microsoft are leading in the AI race. Meta is using AI to strengthen its ad business while betting big on future platforms. The core business is strong, but its long-term bets are still uncertain and expensive. Microsoft, on the other hand, has a diversified and proven business model. Its legacy products across software, cloud computing, and enterprise services have kept its business thriving even before AI entered the picture. Now, with the help of AI, Microsoft is running a massive profit engine.

For long-term investors looking for both hyper-growth and stability over the next decade, Microsoft looks like the better bet.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)