/Lam%20Research%20Corp_%20logo%20on%20phone%20and%20stock%20chart-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

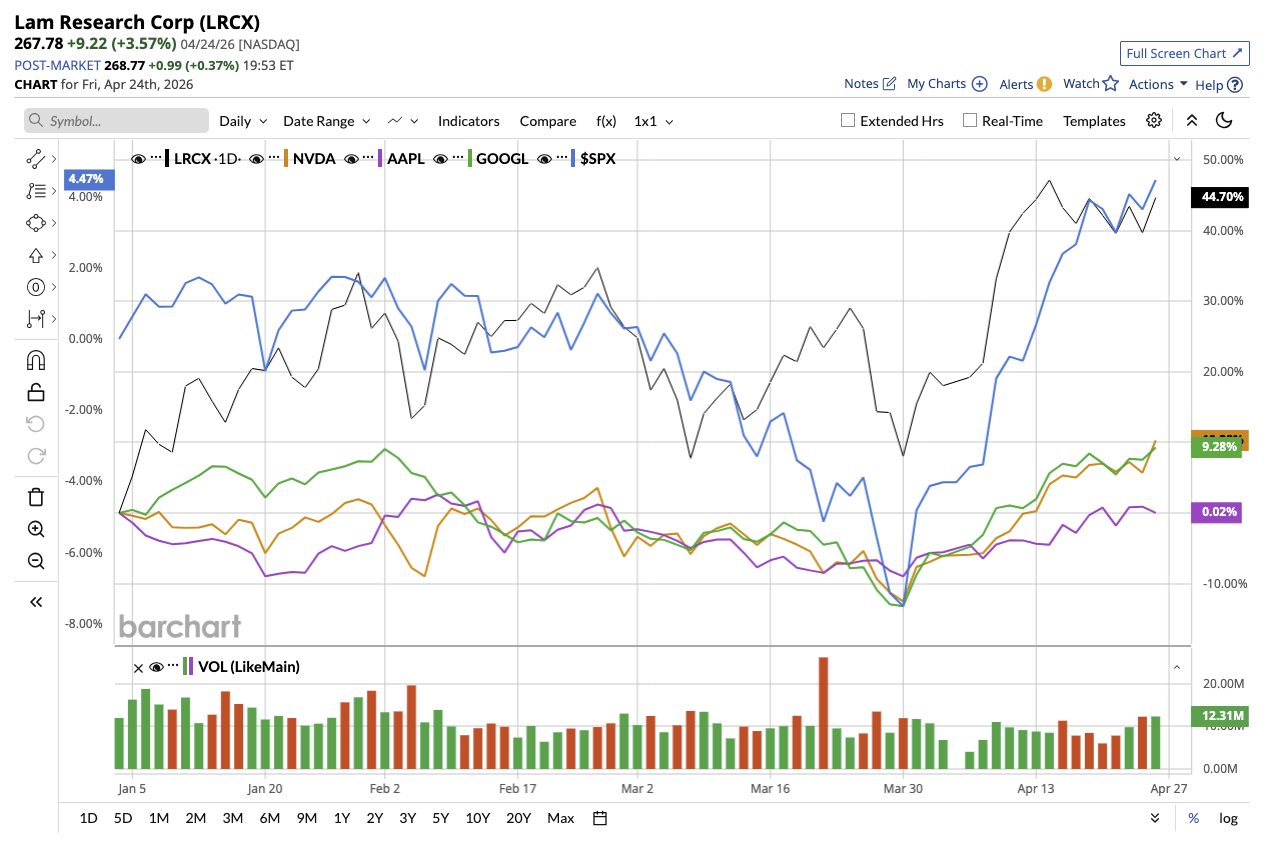

In a market fascinated with trillion-dollar names like Nvidia (NVDA), Apple (AAPL), and Alphabet (GOOG) (GOOGL), one of the year’s best-performing semiconductor stocks goes unnoticed. Lam Research (LRCX) shares have surged 52% year-to-date (YTD), outperforming many of the biggest names in tech. Yet, it is rarely showing up on headlines or “top AI stocks” lists. The reason is that Lam doesn’t create the flashy AI chips. Rather, it builds the machines that make those advanced chips possible. Lam’s March quarter report released last week says that this position is turning into a powerful but underappreciated advantage.

Foundry and Advanced Packaging Are Expanding the Opportunity

With a market cap of $334.8 billion, Lam Research is a semiconductor company that builds the equipment that chipmakers use inside fabs. Its core technologies include etching, which is to carve microscopic patterns into silicon wafers, and deposition, which is to add ultra-thin layers of materials to build chip structures. These processes are then repeated hundreds of times to create modern chips. As semiconductors become more complex, especially for AI, cloud, and high-performance computing, the manufacturing process demands more layers and greater precision. Without companies like Lam, advanced AI chips cannot be produced. This probably explains its outstanding performance in the recent quarters.

In the March quarter, Lam reported a 24% year-over-year (YoY) increase in revenue to $5.8 billion, marking the third consecutive quarter of record revenue. Adjusted earnings per share (EPS) rose 16% YoY to $1.47 per share, meeting the high end of the company’s guidance range. Revenue and earnings both beat consensus estimates.

Foundry accounted for 54% of systems revenue, rising 35% YoY, while memory contributed 39%. Within the memory segment, DRAM (Dynamic Random-Access Memory) alone accounted for 27% of systems revenue, reflecting strong demand tied to high-bandwidth memory and next-generation nodes. Meanwhile, non-volatile memory, which includes NAND (storage memory), made up 12% of systems revenue.

One of Lam’s key customers is Micron (MU), which manufactures DRAM, NAND, and other advanced, high-speed memory used in AI chips. Specifically, Micron plans to spend over $25 billion in capital expenditures in fiscal 2026 and even higher the next year. As supply in the memory industry is constrained but demand continues to rise, memory manufacturers like Micron need to build fabs to expand capacity. These companies will also require highly specialized tools such as etching and deposition equipment, which is where Lam Research excels. This means more business for Lam.

Additionally, Lam’s service business is becoming a silent powerhouse that has been completely overlooked. With an installed base of over 100,000 chambers globally, Lam generates recurring revenue from maintenance, upgrades, and productivity enhancements. During periods of low equipment spending, this growing, high-margin revenue stream adds stability to Lam’s business. While the company continues to invest for growth, it also returned 139% of its free cash flow through buybacks and dividends in the quarter, well above its long-term target of at least 85%.

Looking ahead, management is confident that the second half revenue will most likely exceed the first half. For the June quarter, revenue is expected to increase by 29.4% to $6.6 billion (plus or minus $400 million). EPS is expected to increase by 22.2% to $1.65, with gross margin landing at 50.5%. For the full year, analysts expect Lam’s earnings to increase by 37.2% to $5.68 per share.

Why the Market Is Still Overlooking LRCX Stock

Despite its outstanding performance, Lam has remained under the radar because of a few key reasons. First and foremost, the company operates behind the scenes in the semiconductor manufacturing business, which is complex to understand. This makes it less visible compared to the tech titans manufacturing AI chips. Second, semiconductor suppliers are often seen as cyclical businesses and not stable, revenue-generating companies. However, the scale of AI-driven demand and the complexity of next-generation chips suggest that this cycle may be more sustainable.

Interestingly, investors are slowly recognizing Lam’s long-term growth prospects as AI spending keeps increasing at a rapid pace. LRCX stock is trading at a premium of 34x forward 2027 earnings, which is expected to increase by 37% YoY.

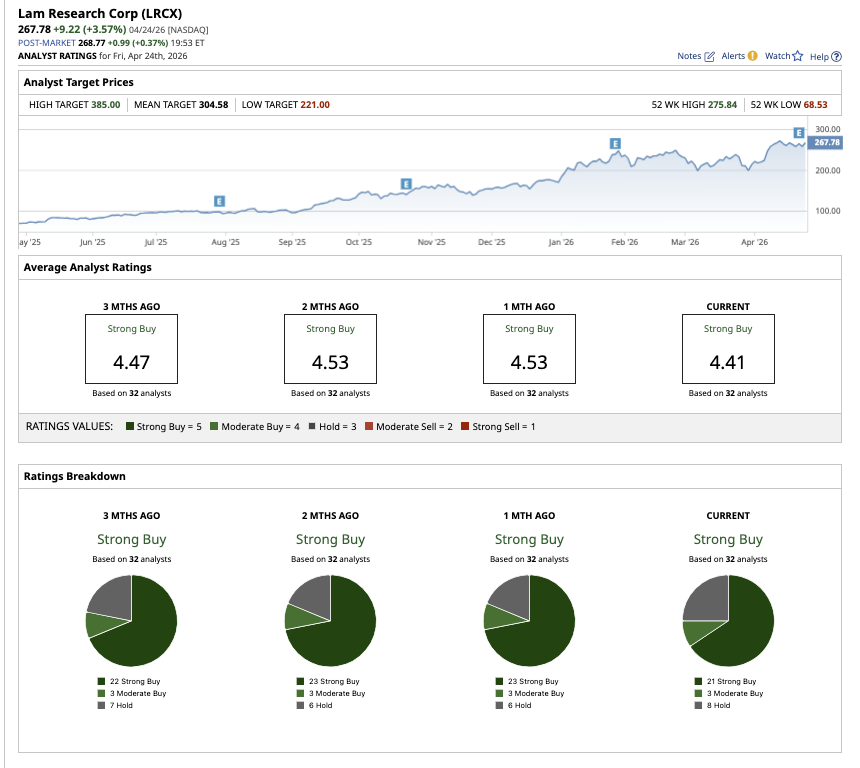

LRCX stock has earned its value on Wall Street, with overall analysts rating it a “Strong Buy.” Of the 32 analysts covering the stock, 21 offer a “Strong Buy” rating, three have a “Moderate Buy,” and eight analysts offer a “Hold” rating. Based on the average target price of $304.58, shares have potential upside of 13.7% from current levels. The Street-high estimate of $385 implies that shares can rally as much as 43.7% over the next 12 months.

Although Lam Research is not the kind of company dominating headlines, it is clearly benefiting from the same AI-driven forces powering the broader semiconductor rally. It remains one of the most overlooked AI winners in the market right now.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)