When macro volatility ticks up and tech momentum begins to feel fragile, the Health Care Select Sector SPDR Fund (XLV) is routinely prescribed as the ultimate defensive remedy. This time around, XLV seems like an especially effective treatment for portfolio maladies.

This daily chart is encouraging to me. That’s a very promising percentage price oscillator (PPO) indicator, even if the moving averages have yet to turn up meaningfully.

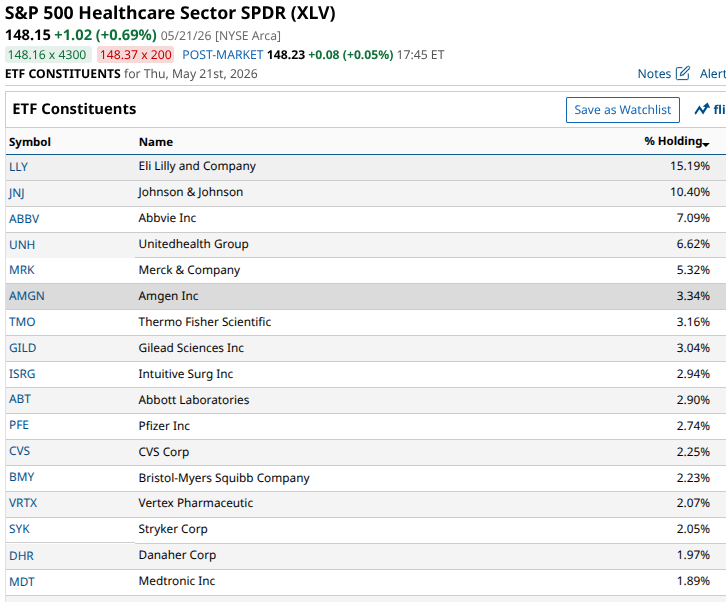

This is one of the 11 sectors of the S&P 500 Index ($SPX), and the ETF holds all the healthcare stocks within the index, with weightings to each stock based on its market capitalization. Healthcare was once a leading S&P 500 sector. Now, it ranks sixth.

The mighty have fallen. But they might just get back up.

Healthcare provides a multitrillion-dollar cushion of inelastic demand. In other words, people need medical treatment regardless of where interest rates go or how a single chipmaker’s earnings shake out. That does not mean it should be the biggest sector any time soon. However, it does mean that when it sells at under 18x trailing earnings, it is worth a look. Especially with the technicals rounding into shape.

XLV has about 60 holdings. However, in classic 2026 fashion, just 10 of them account for 60% of the assets. That’s because over time, a few drug makers, healthcare providers, and medical device makers have come to dominate. And that’s where the current case gets interesting.

Why XLV Is an Interesting Contrarian Play Right Now

However, looking at XLV solely as a monolithic safety trade masks a massive fundamental divergence occurring beneath the surface. To truly understand where the risks and rewards lie for the rest of the year, we have to look past the core ticker and dissect the three critical subsegments powering the sector: medical devices, health insurance, and pure pharmaceuticals.

Medical devices function as the high-beta, growth-oriented engine of the healthcare universe. The segment is heavily driven by procedure volumes, technological milestones, and capital expenditure budgets at major hospitals. Now, with interest rates stuck in a higher-for-longer regime, capital-intensive med-tech firms are facing compressed margins.

This chart of the iShares U.S. Medical Devices ETF (IHI) shows where much of XLV’s underperformance comes from. That’s a horrendous chart, on a backward-looking basis. However, I’m looking forward, to an industry within healthcare that might finally be washed out “enough.”

Then there’s healthcare providers, the insurance giants like UnitedHealth (UNH) and Elevance Health (ELV). These companies are essentially massive cash-flow utilities, although they are heavily exposed to regulatory policy, corporate benefit trends, and government reimbursement rates.

Lastly, there’s the drug sub-sector, driven by legacy global powerhouses like Eli Lilly (LLY), Merck (MRK), and Pfizer (PFE). This segment of healthcare is insulated by robust patent portfolios and massive, recurring global drug spend. There’s also a good chance that AI plays a role in increasing profit margins here, as well augmenting the speed of new drug discovery.

XLV is a highly effective tool for broad sector exposure, but it is a sum of vastly different moving parts. If you are looking for defensive insulation from a top-heavy stock market, the reliable yield and pricing power of pharmaceuticals, such as through the VanEck Pharmaceutical ETF (PPH), offer a sturdy anchor. If you are counting on a resilient consumer and a return to tech-driven growth, medical devices provide the operational leverage.

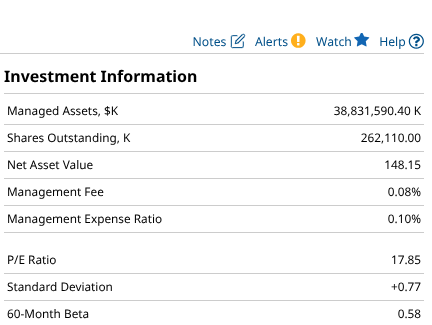

Navigating healthcare requires looking past the broad index label and understanding exactly which engine is driving your capital. But as I see it, there’s going to come a point where the market will look at that historically low volatility (beta=0.58) and say, “OK, I’ll buy some” once tech-mania fades a bit.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)