/Synopsys%2C%20Inc_%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Sunnyvale, California-based Synopsys, Inc. (SNPS) provides electronic design automation (EDA) software products used to design and test integrated circuits. With a market cap of $96.5 billion, the company provides design technologies to creators of advanced integrated circuits, electronic systems, and systems on a chip.

Shares of this global leader in EDA have underperformed the broader market over the past year. SNPS has gained marginally over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.4%. In 2026, SNPS’ stock rose 8%, compared to the SPX’s 8.8% rise on a YTD basis.

Narrowing the focus, SNPS’ outperformance is apparent compared to the iShares Expanded Tech-Software Sector ETF (IGV). The exchange-traded fund has declined about 9.1% over the past year. Moreover, the stock’s single-digit returns on a YTD basis outshine the ETF’s 11.6% losses over the same time frame.

On Feb. 25, SNPS shares closed up by 1.9% after reporting its Q1 results. Its adjusted EPS of $3.77 surpassed Wall Street expectations of $3.57. The company’s revenue was $2.41 billion, beating Wall Street forecasts of $2.39 billion. SNPS expects full-year adjusted EPS in the range of $14.38 to $14.46, and revenue ranging from $9.6 billion to $9.7 billion.

For the current fiscal year, ending in October, analysts expect SNPS’ EPS to grow 19.1% to $10.30 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

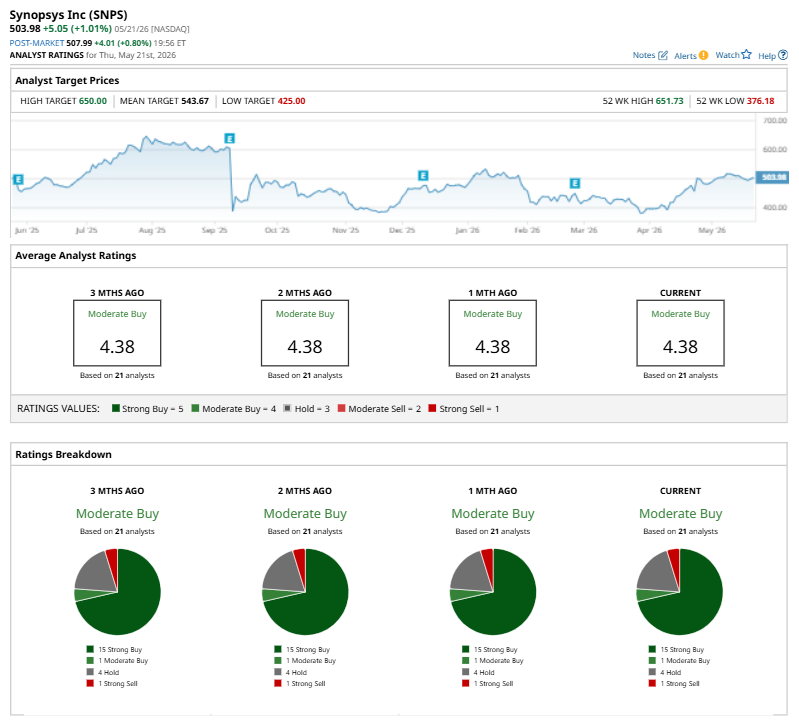

Among the 21 analysts covering SNPS stock, the consensus is a “Moderate Buy.” That’s based on 15 “Strong Buy” ratings, one “Moderate Buy,” four “Holds,” and one “Strong Sell.”

The configuration has been consistent over the past three months.

On May 20, Morgan Stanley (MS) analyst Lee Simpson maintained a “Hold” rating on SNPS and set a price target of $493.87.

The mean price target of $543.67 represents a 7.9% premium to SNPS’ current price levels. The Street-high price target of $650 suggests a notable upside potential of 29%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)