/Verisk%20Analytics%20Inc%20logo%20magnified-by%20Casimiro%20PT%20via%20Shutterstock.jpg)

Jersey City, New Jersey-based Verisk Analytics, Inc. (VRSK) engages in the provision of data analytics and technology solutions to the insurance industry in the United States and internationally. Valued at a market cap of $22.4 billion, the company offers underwriting solutions, including forms, rules, and loss-cost services, such as policy language, prospective loss costs, policy writing, and other services.

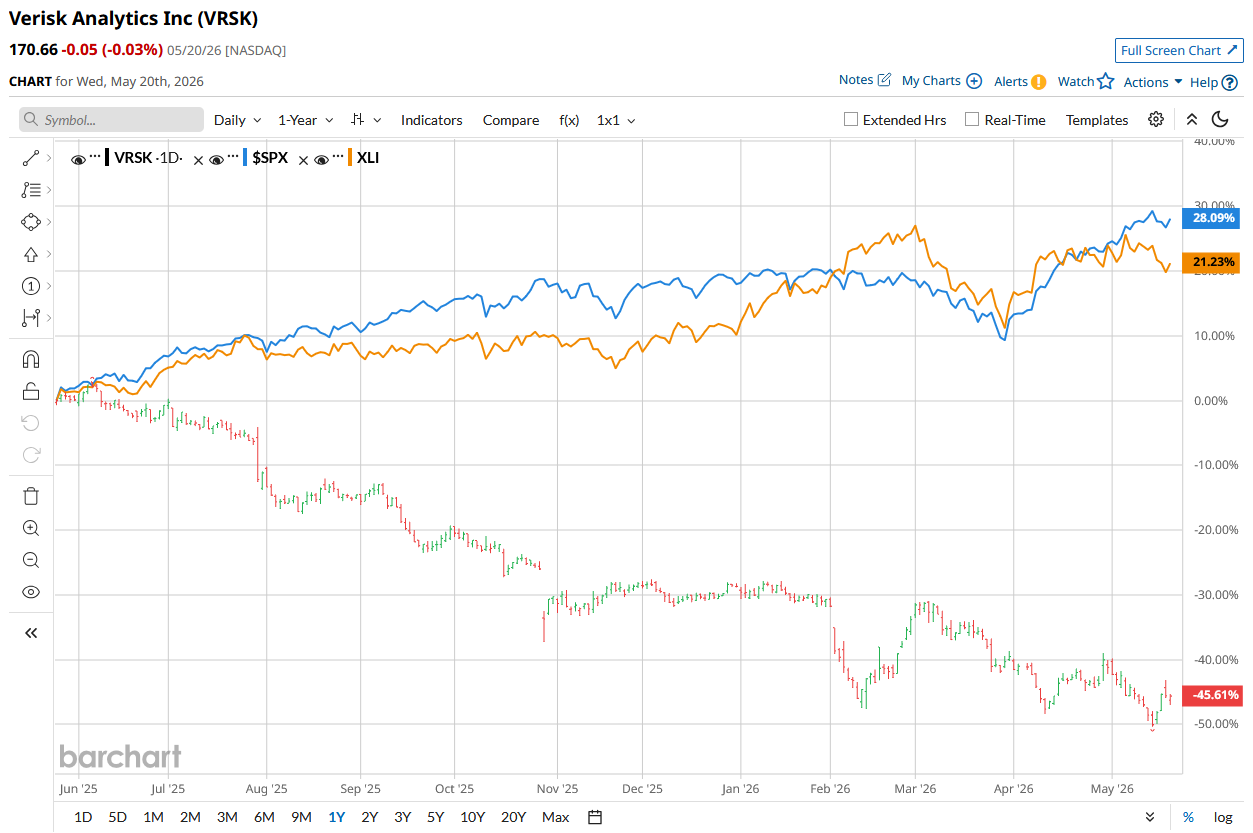

VRSK shares have underperformed the broader market over the past year and in 2026. VRSK stock has declined 45.5% over the past 52 weeks and 23.7% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 25.1% over the past year and risen 8.6% in 2026.

Narrowing the focus, VRSK has also lagged behind the State Street Industrials Select Sector SPDR ETF’s (XLI) 18.8% rise over the past 52 weeks and its 10.1% increase this year.

On Apr. 29, VRSK stock rose 6.5% following the release of its Q1 2026 earnings. The company’s revenue rose 3.9% from the prior year’s quarter and came in at $782.6 million, surpassing the Street’s estimates. Moreover, its adjusted EPS amounted to $1.82, also coming in on top of Wall Street’s estimates. Verisk expects full-year earnings in the range of $7.45 to $7.75 per share, with revenue in the range of $3.19 billion to $3.24 billion.

For the current year, which ends in December, analysts expect VRSK’s EPS to rise 6.6% to $7.63 on a diluted basis. The company’s earnings surprise history is solid. It surpassed the consensus estimate in each of the last four quarters.

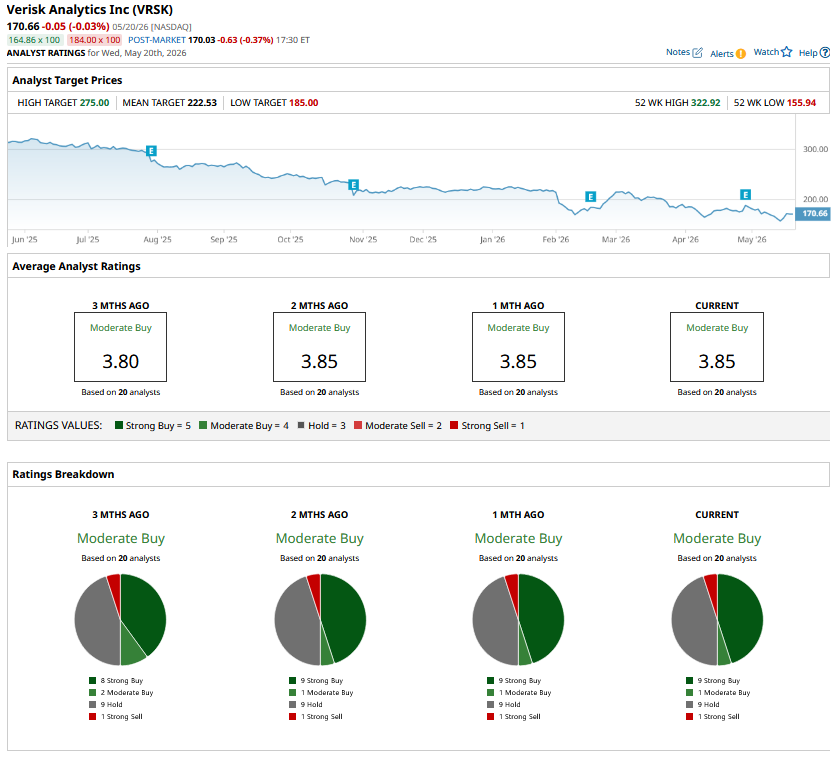

VRSK has a consensus “Moderate Buy” rating overall. Of the 20 analysts covering the stock, opinions include nine “Strong Buys,” one “Moderate Buy,” nine “Holds,” and one “Strong Sell.”

The configuration has remained the same over the last month.

On Apr. 30, JP Morgan analyst Andrew Steinerman maintained an "Overweight" rating for Verisk Analytics and raised its price target from $220 to $230.

VRSK’s mean price target of $222.53 indicates a modest premium of 30.4% from the current market prices. While the Street-high target of $275 suggests a notable 61.1% upside potential.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)