/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)

With a market cap of $106.6 billion, ServiceNow, Inc. (NOW) is a cloud-based software company that provides digital workflow solutions to help organizations automate and manage IT, customer service, security, HR, and business operations across multiple industries worldwide. It also offers AI-driven platforms, database solutions, and enterprise collaboration services to support scalable and secure business transformation.

Shares of the Santa Clara, California-based company have lagged behind the broader market over the past 52 weeks. NOW stock has tumbled 50.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 23.8%. Moreover, shares of the company are down 33.9% on a YTD basis, compared to SPX's 7.9% gain.

In addition, shares of ServiceNow have underperformed the State Street Technology Select Sector SPDR ETF's (XLK) 48.7% surge over the past 52 weeks.

Shares of ServiceNow fell 17.8% following its Q1 2026 results on Apr. 22 as the company projected a lower-than-expected full-year subscription adjusted gross margin of 81.5%, below analysts’ estimate, primarily due to the impact of recent acquisitions, including the Armis deal. Investors were also concerned that subscription revenue growth faced an approximately 75-basis-point headwind from delayed closings of several large on-premise deals in the Middle East caused by ongoing regional conflict. Although Q1 revenue rose 22% year-over-year to $3.77 billion and the company raised its full-year subscription revenue forecast to $15.74 billion - $15.78 billion, the weaker margin outlook overshadowed the otherwise strong growth and guidance.

For the fiscal year ending in December 2026, analysts expect NOW's EPS to grow 19.9% year-over-year to $2.35. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

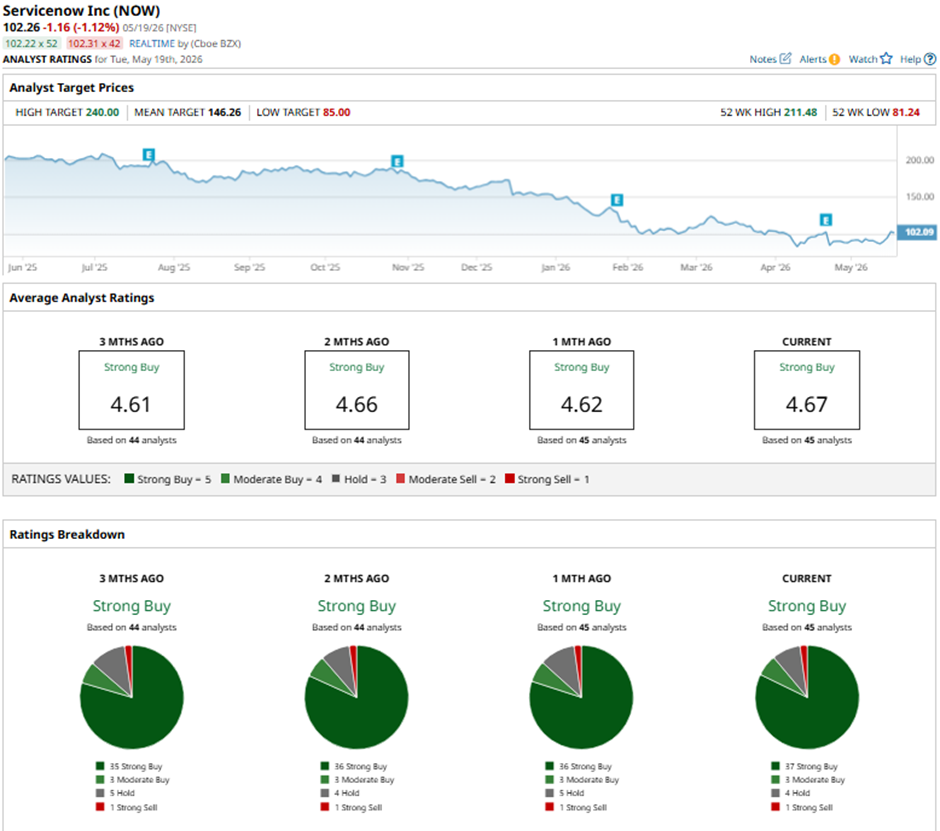

Among the 45 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 37 “Strong Buy” ratings, three “Moderate Buys,” four “Holds,” and one “Strong Sell.”

On May 7, Bernstein analyst Peter Weed raised ServiceNow’s price target to $236 while maintaining an “Outperform" rating.

The mean price target of $146.26 represents a 43% premium to NOW’s current price levels. The Street-high price target of $240 suggests a 134.7% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)