/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

Intel Corporation (INTC) has suddenly become one of Wall Street’s hottest comeback stories as a fresh central processing unit (CPU) rally is sweeping through the semiconductor sector. After spending years stuck in the shadows while Nvidia Corporation (NVDA) dominated the artificial intelligence (AI) boom, Intel now finds itself back in the thick of the conversation.

Wall Street is realizing that AI infrastructure cannot survive on graphics processing units (GPUs) alone. Training large AI models might still lean heavily on Nvidia’s accelerators, although AI inference and agentic workloads require massive amounts of general-purpose computing power. That trend has thrown CPUs back into the spotlight, putting Intel’s Xeon processors right at the center of the action.

Big money has already started following the trail. Chase Coleman’s Tiger Global Management, one of the most closely watched hedge funds on Wall Street with nearly $78 billion in assets under management (AUM), opened a brand-new Intel position during Q1 2026. The fund purchased 1,638,700 shares valued at roughly $180 million, according to its latest 13F filing.

However, the company is still facing stiff competition from Taiwan Semiconductor Manufacturing Company Limited (TSM) and Nvidia in advanced chip technology. If AI spending continues spreading beyond GPUs, the current CPU rally may or may not still have plenty of runway left.

About Intel Stock

Based in Santa Clara, Intel powers everything from household laptops to enormous data centers through its semiconductor technology. The company built its empire on x86 processors and now channels that legacy into AI, cloud computing, and advanced manufacturing.

Carrying a market cap of approximately $546.7 billion, the company has refused to sit on its hands, charging full steam ahead into foundry services and next generation chip architecture.

On the price performance front, Intel stock surged 393.26% over the past 52 weeks. The rally did not cool off in 2026 either as its shares climbed 189.54% year-to-date (YTD) along with another 55.97% jump during the last month alone.

On the valuation front, the market is pricing in a lot of ambition as INTC stock is trading at 100.16 times forward adjusted earnings and 9.33 times sales. This puts it well above both industry benchmarks and their own five-year average multiples.

Intel Surpasses Q1 Earnings

On April 23, Intel delivered Q1 FY2026 results that sailed past Wall Street expectations, giving fresh life to the once struggling chipmaker. The stock gained 2.3% that day before exploding another 23.6% during the following trading session.

Revenue grew 7.2% year-over-year (YOY) to $13.58 billion, comfortably outpacing the Street's estimate of $12.42 billion. Intel has now beaten its own revenue expectations for six quarters running. Adjusted EPS climbed 123.1% YOY to $0.29, leaving the Street’s forecast of $0.01 far behind.

The firm’s data center business led the charge, where AI traction is finally building on the back of surging demand for CPU. That division posted $5.1 billion in revenue, good for 22% growth.

The same wave of CPU demand also fueled Intel’s $14 billion acquisition of a 49% stake in its Ireland chip fabrication facility, which the company had previously sold to Apollo Global Management (APOS).

Intel’s recent partnerships also signal that the CPU revival carries real weight. The company expanded its collaboration with Alphabet (GOOG) (GOOGL) in Q1 through continued Xeon deployment across Google Cloud along with joint development of custom AI infrastructure processors. And, Intel secured a major win after Nvidia selected Intel Xeon 6 as the host CPU for Nvidia’s DGX Rubin NVL8 systems.

Intel’s foundry business delivered strong numbers, with its revenue climbing 16% YOY to $5.4 billion, although much of that operation still revolves around manufacturing Intel’s own chips. The Client Computing Group, which handles personal computer chips, generated $7.7 billion in revenue after posting 1% growth.

Looking ahead, Intel expects Q2 revenue between $13.8 billion and $14.8 billion along with adjusted EPS of $0.20. Analysts, meanwhile, expect Q2 EPS to surge 138.5% YOY to $0.10. FY2026 bottom line could jump 625% from the prior year’s quarter to $0.63. Analysts also forecast FY2027 EPS to rise another 54% YOY to $0.97.

What Do Analysts Expect for Intel Stock?

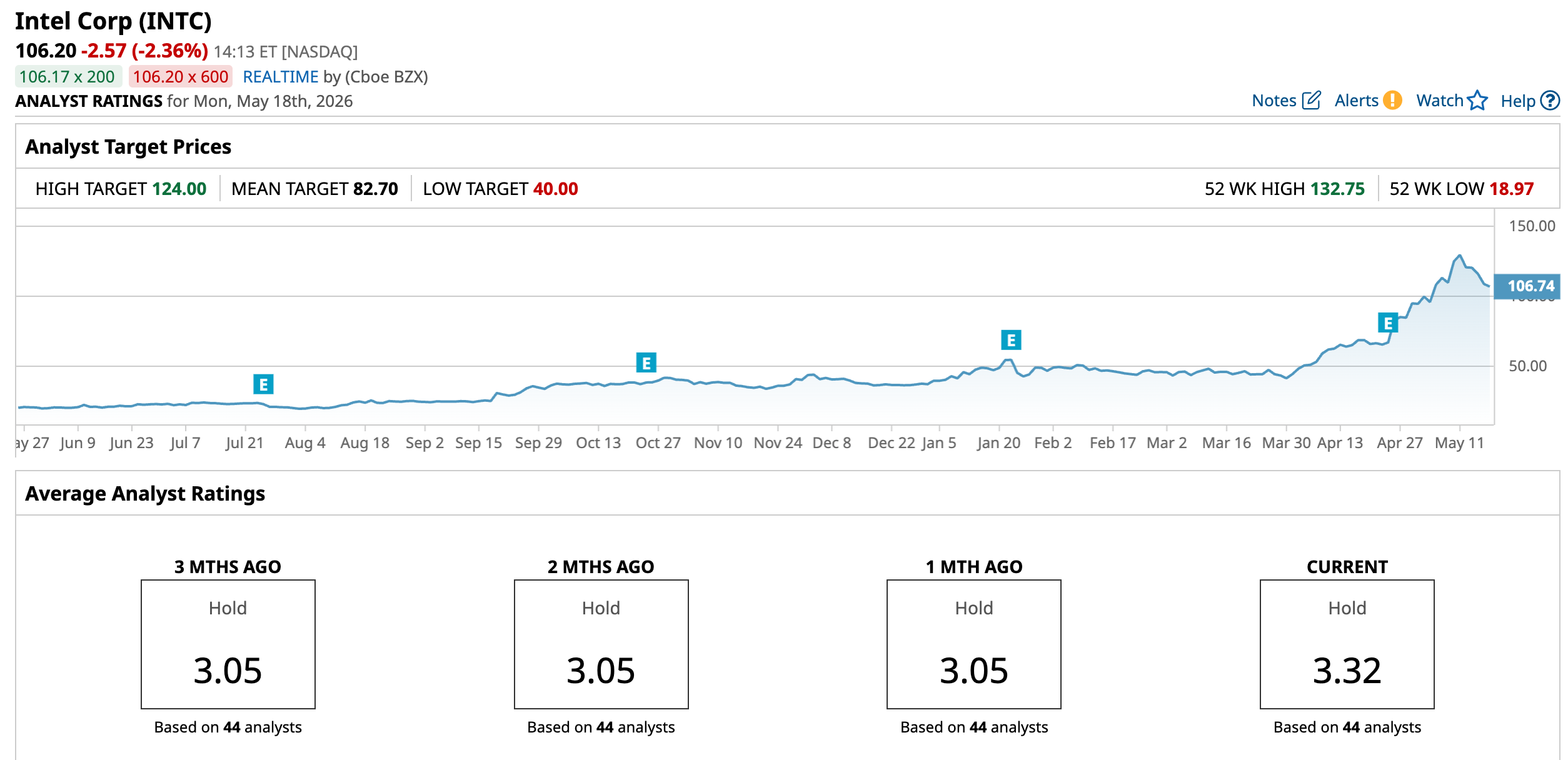

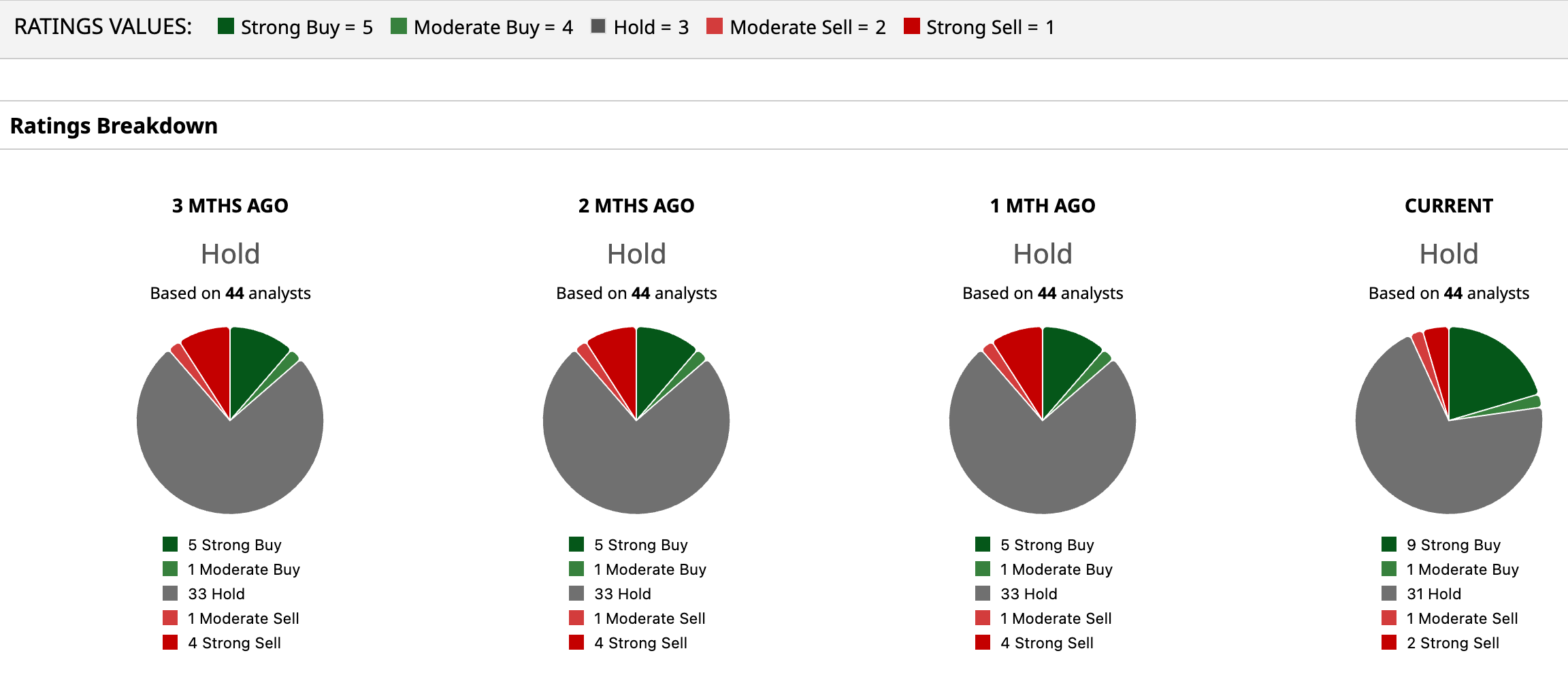

Wall Street still refuses to put all its chips on the table, giving INTC stock an overall “Hold” rating for now. Among 44 analysts covering the company, nine rate the shares a “Strong Buy,” one assigns a “Moderate Buy,” 31 stick with “Hold,” one calls for a “Moderate Sell,” and two wave the “Strong Sell” flag.

Interestingly, Intel stock already trades above the average analyst price target of $82.70, signaling that much of the near-term optimism may already sit baked into the share price.

Even so, Mizuho’s Street-High target of $124 still leaves room for potential upside of 16.8% current levels. The firm raised its target from $100 while maintaining a “Neutral” rating on the stock.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)