McCormick & Company, Incorporated (MKC) leverages its global flavor‑creation platform from its Hunt Valley, Maryland headquarters to design, manufacture, and distribute spices, seasonings, condiments, and custom flavor systems for consumers and food‑industry customers worldwide. The company has a market capitalization of $12.46 billion.

There are concerns surrounding the company’s merger, which has affected its stock performance. Over the past 52 weeks, the stock has dropped 38.1%, and it is down 31.4% year-to-date (YTD). The stock reached a 52-week low of $44.82 on May 13 but is up 4.2% from that level.

On the other hand, the broader S&P 500 Index ($SPX) has gained 24.3% and 8.1% over the same periods, respectively, indicating that the stock has underperformed the broader market over the past year. Next, we compare the stock with its own sector. The State Street Consumer Staples Select Sector SPDR ETF (XLP) has gained 4.7% over the past 52 weeks and 10.6% YTD. Therefore, the stock has underperformed its sector over these periods.

McCormick is set to combine with Unilever’s (UL) Foods business, excluding India and other excluded businesses. The company is set to pay $15.70 billion for Unilever’s food portfolio, including Hellmann’s Mayo and the U.K.’s favorite Marmite. In the combined entity, Unilever shareholders are expected to own 55.1%, McCormick shareholders 35%, and Unilever is also expected to hold a 9.9% stake.

Hoping to create revenue synergies through its spice portfolio and Unilever’s food offerings, the deal is expected to close in mid-2027, subject to shareholders’ approval.

McCormick also reported better-than-expected Q1 results for fiscal 2026, with a 16.7% year-over-year (YOY) growth in total net sales and 1.2% organic sales growth. For the current fiscal year, the company is expecting a 13%-17% net sales growth and a 1%-3% organic sales growth.

For the current quarter, Wall Street analysts expect McCormick’s EPS to grow 2.9% YOY to $0.71 on a diluted basis. Moreover, EPS is expected to increase 3% annually to $3.09 in fiscal 2026, followed by a 9.7% improvement to $3.39 in fiscal 2027. The company has a solid history of surpassing consensus estimates, topping them in three of the four trailing quarters.

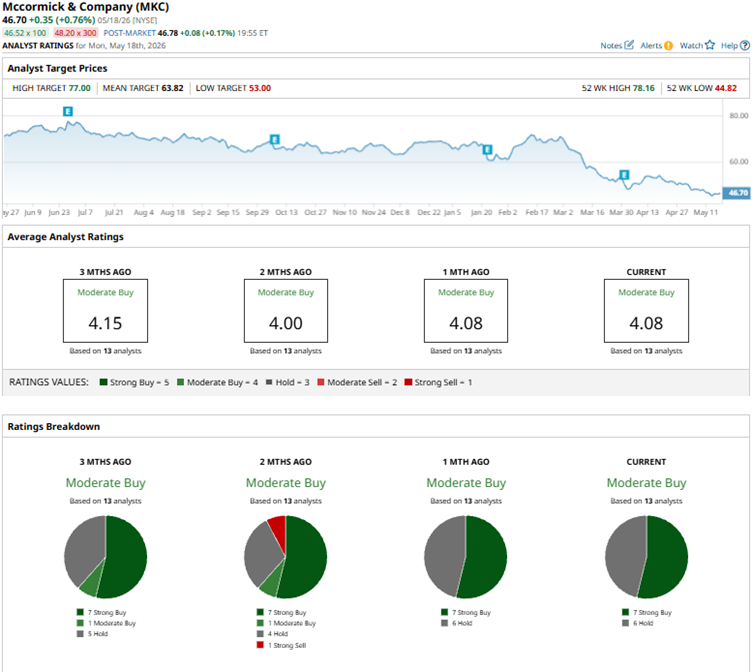

Among the 13 Wall Street analysts covering McCormick’s stock, the consensus is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings and six “Holds.” The ratings configuration has remained the same over the past month.

Last month, analysts at BTIG initiated coverage of McCormick with a “Neutral” rating. The firm considered MKC’s valuation fair given its base business and is not convinced of the merged entity's ability to capture revenue synergies.

McCormick’s mean price target of $63.82 indicates a 36.7% upside over current market prices. The Street-high price target of $77 implies a 64.9% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)