/Cadence%20Design%20Systems%2C%20Inc_%20logo%20and%20chart-by%20IgorGolovniov%20via%20Shutterstock.jpg)

San Jose, California-based Cadence Design Systems, Inc. (CDNS) develops computational, AI-driven software, hardware, and silicon intellectual property (IP) products and solutions. Valued at a market cap of $95.4 billion, the company offers products and tools that help customers to design electronic products through the System Design Enablement (SDE) strategy. The company also offers software, hardware, services and reusable IC design blocks to electronic systems and semiconductor customers.

CDNS shares have lagged behind the broader market over the past year and surged 7.6% compared to the S&P 500 Index ($SPX) 24.3% surge. However, in 2026, the stock has grown nearly 10.7%, outperforming the SPX’s 8.1% rise.

Focusing on its industry benchmark, the State Street Technology Select Sector SPDR ETF (XLK) has risen 48.5% over the past year, outperforming the stock. In 2026, as well, XLK surged 21.1% and has rallied the stock.

On Apr. 27, CDNS stock rose 1.1% following the release of its better-than-expected Q1 2026 earnings. The company’s revenue for the quarter came in at $1.5 billion and surpassed the Street’s estimates. Moreover, its adjusted EPS amounted to $1.96, also surpassing Wall Street’s forecasts. The company expects full-year earnings in the range of $7.85 to $7.95 per share, with revenue ranging from $6.1 billion to $6.2 billion.

For the current year ending in December, analysts expect CDNS’ EPS to rise 13.7% year over year to $6.23. Moreover, the company has met or surpassed analysts’ consensus estimates in each of the past four quarters.

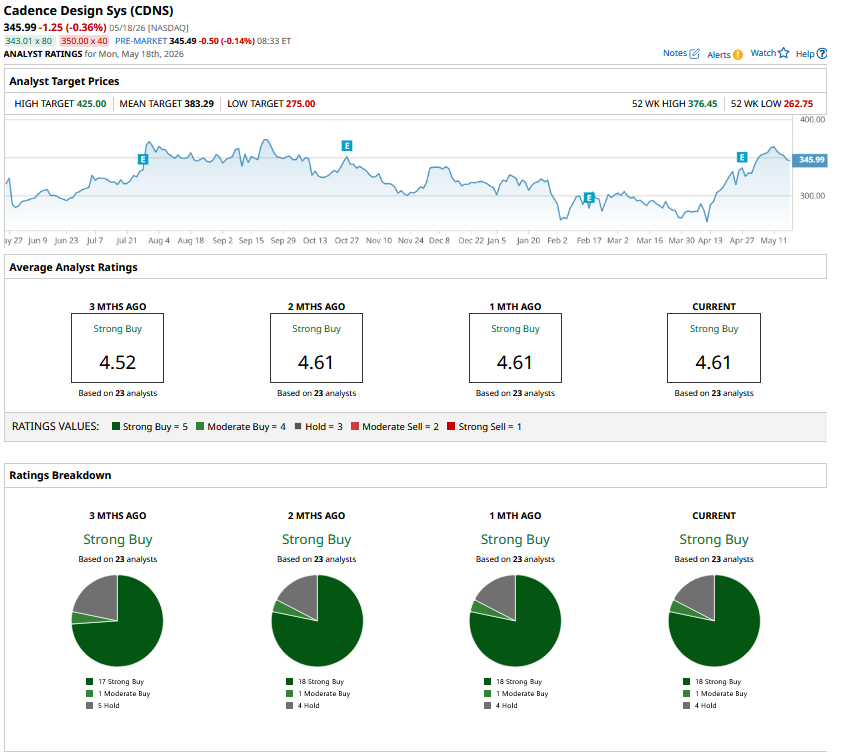

Among the 23 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 18 “Strong Buy” ratings, one “Moderate Buy,” and four “Holds.”

The configuration has remained more or less unchanged over the past month.

On Apr. 29, Citi analyst Kelsey Chia maintained a “Buy” rating for CDNS and adjusted its price target from $385 to $400.

CDNS’ mean price target of $383.29 indicates a premium of 10.8% from the current market prices. Its Street-high target of $425 suggests a robust 22.8% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)