Texas Pacific Land Corporation (TPL), headquartered in Dallas, Texas, owns and manages tracts of land and resource, and water services and operations businesses in Texas. Valued at $26.6 billion by market cap, the company’s income is derived from land sales, oil and gas royalties, grazing leases, and interest.

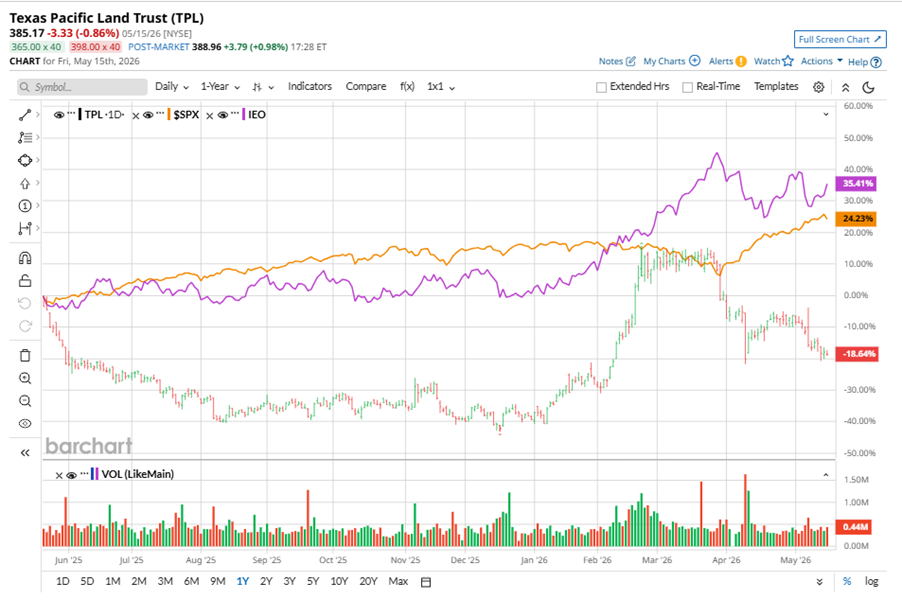

Shares of this leading owner of oil and gas surface acreage and subsurface mineral interests have underperformed the broader market over the past year. TPL has declined 18.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 25.2%. However, in 2026, TPL stock is up 34.1%, surpassing the SPX’s 8.2% rise on a YTD basis.

Narrowing the focus, TPL’s underperformance is also apparent compared to the iShares U.S. Oil & Gas Exploration & Production ETF (IEO). The exchange-traded fund has gained about 33.6% over the past year. Moreover, the ETF’s 34.6% returns on a YTD basis outshine the stock’s gains over the same time frame.

TPL lagged as operator activity was only “marginally” higher despite strong oil prices. Gains came from unhedged royalties were supported by $50 million revenue per $10/bbl move and record water volumes. TPL signed a $43 million, 20-year land & data center deal and is launching a 10k bpd desalination plant. Focus now is on power/data center deals and talks with AI hyperscalers, while drilling by majors like Exxon Mobil Corporation (XOM) and Occidental Petroleum Corporation (OXY) lifted well inventory.

On May 6, TPL shares closed down by 2.5% after reporting its Q1 results. Its revenue stood at $236.8 million, up 20.8% year over year. The company’s EPS increased 18.3% from the year-ago quarter to $2.07.

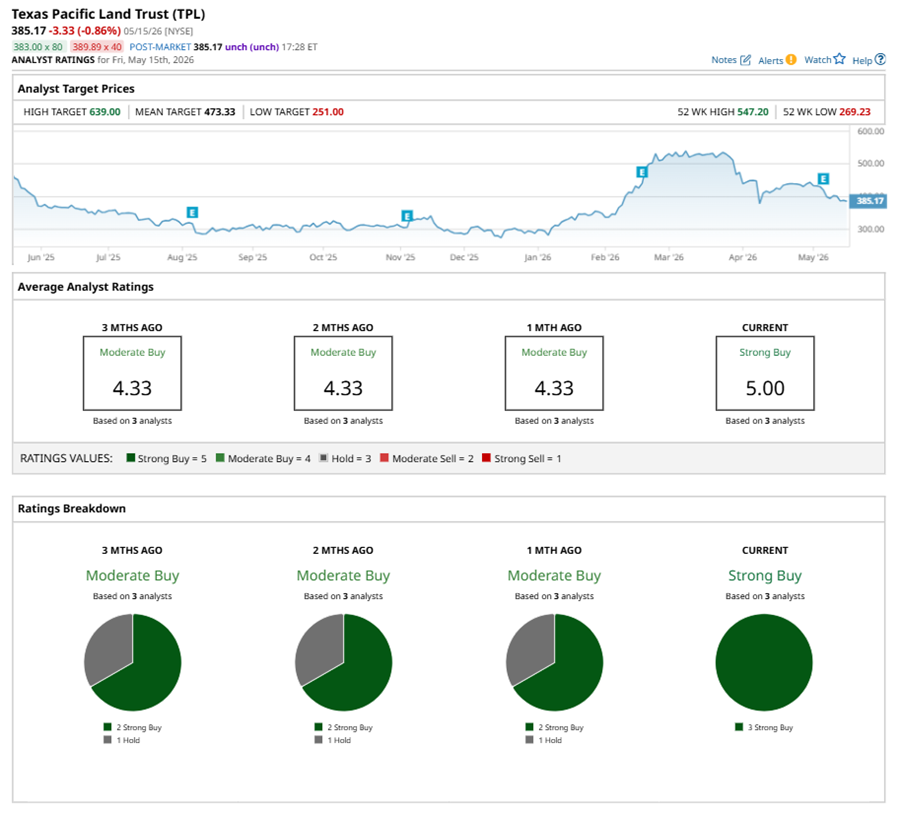

For the current fiscal year, ending in December, analysts expect TPL’s EPS to grow 33% to $9.27 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in both of the last two quarters.

Consensus for TPL stock is a "Strong Buy," with all three analysts recommending it.

This configuration is more bullish than a month ago, with an overall “Moderate Buy” rating, consisting two analysts suggesting a “Strong Buy.”

On Apr. 1, KeyBanc analyst Tim Rezvan maintained a “Buy” rating on TPL and set a price target of $639, the Street-high price target, implying a potential upside of 65.9% from current levels.

The mean price target of $473.33 represents a 22.9% premium to TPL’s current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)