With a market cap of $150.9 billion, Welltower Inc. (WELL) is a leading healthcare real estate investment trust (REIT) that owns, develops, and manages properties focused on senior housing, post-acute care, and outpatient medical services. Headquartered in Toledo, Ohio, the company is one of the largest healthcare REITs in the world and operates across the United States, Canada, and the United Kingdom.

WELL stock has surged 45.5% over the past 52 weeks and has grown 15.2% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 25.2% over the past year and has surged 8.2% in 2026.

Narrowing the focus, WELL has also outperformed the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 4.2% rise over the past 52 weeks and 7.1% rally this year.

Shares of Welltower climbed 2% on Apr. 28 after the company delivered strong first-quarter 2026 results that exceeded investor expectations and highlighted continued momentum in the senior housing market. It posted normalized FFO of $1.47 per diluted share, up 23% year over year and above analyst expectations of $1.44 per share. Revenue surged 38.3% annually to roughly $3.35 billion, fueled by strong occupancy gains, rent growth, and acquisition activity.

For the current year ending in December, analysts expect WELL to report a 18.7% year-over-year growth in adjusted EPS to $6.28. The company has a stellar earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

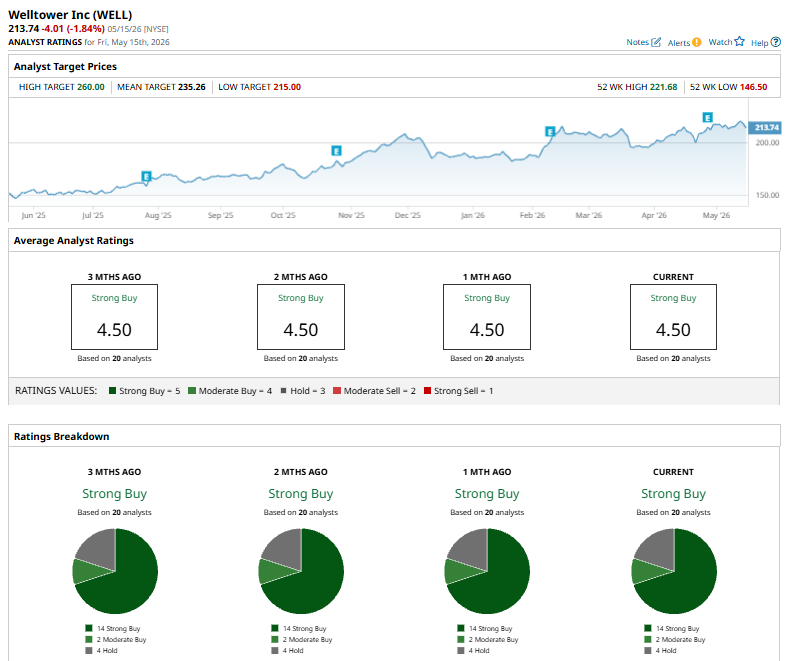

WELL has a consensus “Strong Buy” rating overall. Of the 20 analysts covering the stock, opinions include 14 “Strong Buys,” two “Moderate Buys,” and four “Holds.”

The configuration has remained mostly stable in recent months.

On May 13, Jefferies analyst Jonathan Petersen raised his price target on Welltower to $248 from $237 while maintaining a “Buy” rating on the stock. The analyst updated estimates following Welltower’s strong first-quarter earnings report and increased full-year guidance, reflecting confidence in the company’s accelerating senior housing growth, improving occupancy trends, and stronger operating performance.

WELL’s mean price target of $235.26 indicates a 10.1% premium to the current market prices. Its Street-high target of $260 suggests a robust 21.6% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)