/Thermo%20Fisher%20Scientific%20Inc_%20logo%20on%20building-by%20JHVEPhoto%20via%20iStock.jpg)

Valued at a market cap of $162.9 billion, Thermo Fisher Scientific Inc. (TMO) is a Waltham, Massachusetts-based company that provides life sciences solutions, analytical instruments, specialty diagnostics, and laboratory products and biopharma services.

This healthcare company has considerably underperformed the broader market over the past 52 weeks. Shares of TMO have gained 8.3% over this time frame, while the broader S&P 500 Index ($SPX) has soared 25.2%. Moreover, on a YTD basis, the stock is down 24.4%, compared to SPX’s 8.1% rise.

Narrowing the focus, TMO has also lagged the State Street Health Care Select Sector SPDR ETF (XLV), which gained 11.2% over the past 52 weeks and dropped 6.3% on a YTD basis.

On Apr. 23, shares of TMO plunged 9.2% after its Q1 earnings release, despite delivering better-than-expected results. The company’s revenue increased 6.2% year-over-year to $11 billion, surpassing consensus estimates by 1.7%, while its adjusted EPS of $5.44 topped analyst expectations of $5.20. Management credited the strong performance to robust growth in its bioproduction and clinical research businesses. However, management noted persistent softness in academic, government, and diagnostics-related demand, especially across the U.S. and China. The cautious commentary around broader macroeconomic uncertainty and ongoing spending constraints in these end markets appeared to weigh on investor sentiment.

For the current fiscal year, ending in December, analysts expect TMO’s EPS to grow 8.7% year over year to $24.86. The company’s earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

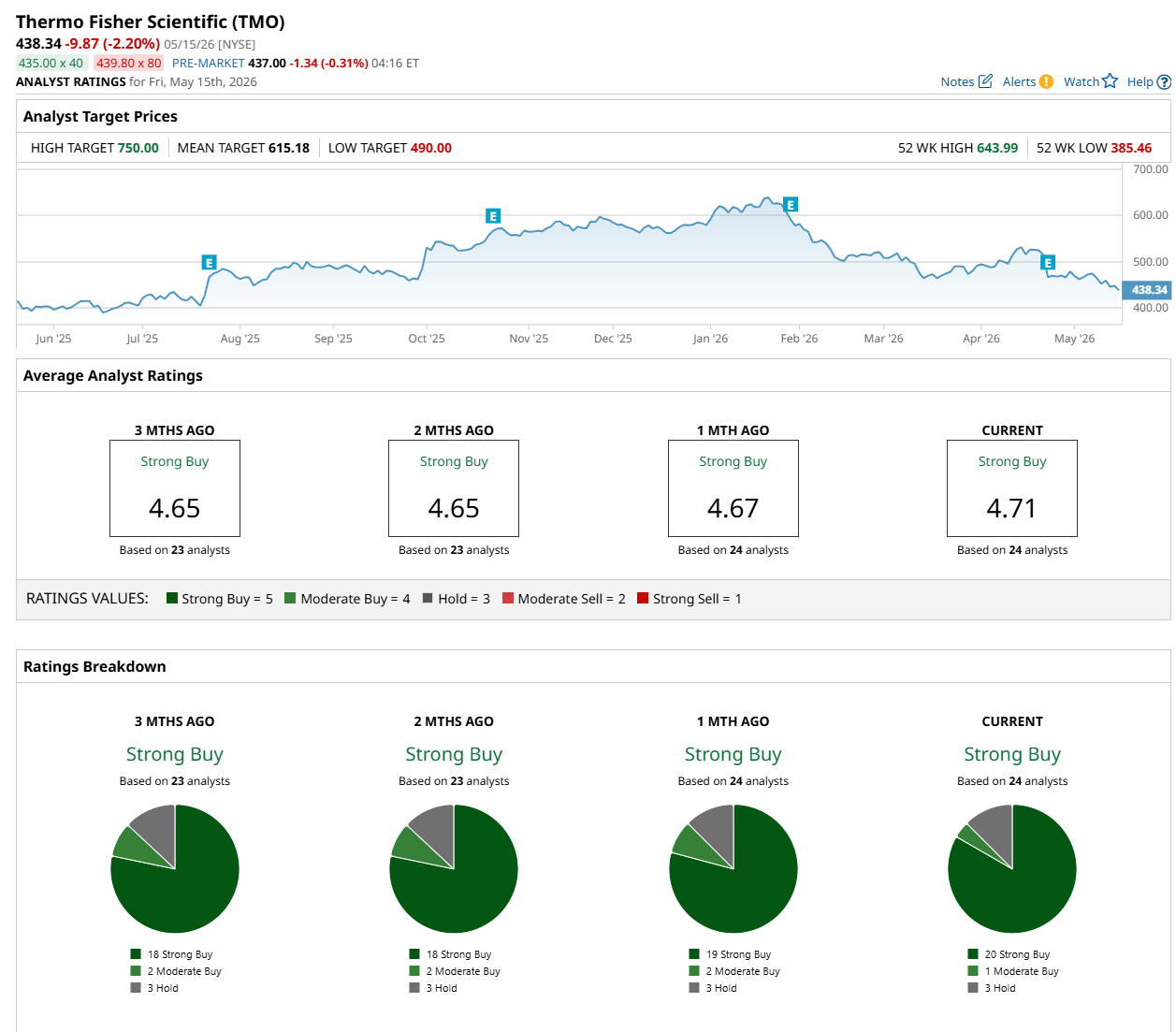

Among the 24 analysts covering the stock, the consensus rating is a "Strong Buy,” which is based on 20 “Strong Buy,” one "Moderate Buy," and three "Hold” ratings.

The configuration is more bullish than a month ago, with 19 analysts suggesting a “Strong Buy” rating.

On May 14, RBC Capital resumed coverage of TMO with a “Sector Perform” rating and $490 price target, indicating an 11.8% potential upside from the current levels.

The mean price target of $615.18 suggests a 40.3% premium to its current price levels, while its Street-high price target of $750 implies a 71.1% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)