/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

Tesla (TSLA) is in the news again, which is not always a source of comfort for investors. The company is still leaning hard into artificial intelligence (AI), autonomy, robots, and batteries, while its core electric vehicle (EV) business keeps sending mixed signals. That is the big tension in Tesla right now. On one hand, TSLA stock keeps getting support from robotaxi hopes, Full Self-Drivign (FSD) chatter and China strength. On the other, the company is also heading into a heavy spending cycle that could pressure cash flow later this year.

Tesla now says it will put almost $250 million more into battery cell production at its plant in Berlin, Germany, lifting planned annual capacity to 18 gigawatt-hours (GWh). That is good strategic news, but it also reminds investors that Tesla is spending more before it has fully proven the payoff.

About Tesla Stock

Tesla is no ordinary automaker. It sells EVs, batteries and energy storage, but shares trade more like a long-dated bet on self-driving, robotaxis and humanoid robots. That is why every new factory, chip project or software rollout matters so much. Tesla is trying to turn future optionality into today’s valuation. That is exciting. It is also why TSLA stock can look expensive even when the quarterly numbers come in fine.

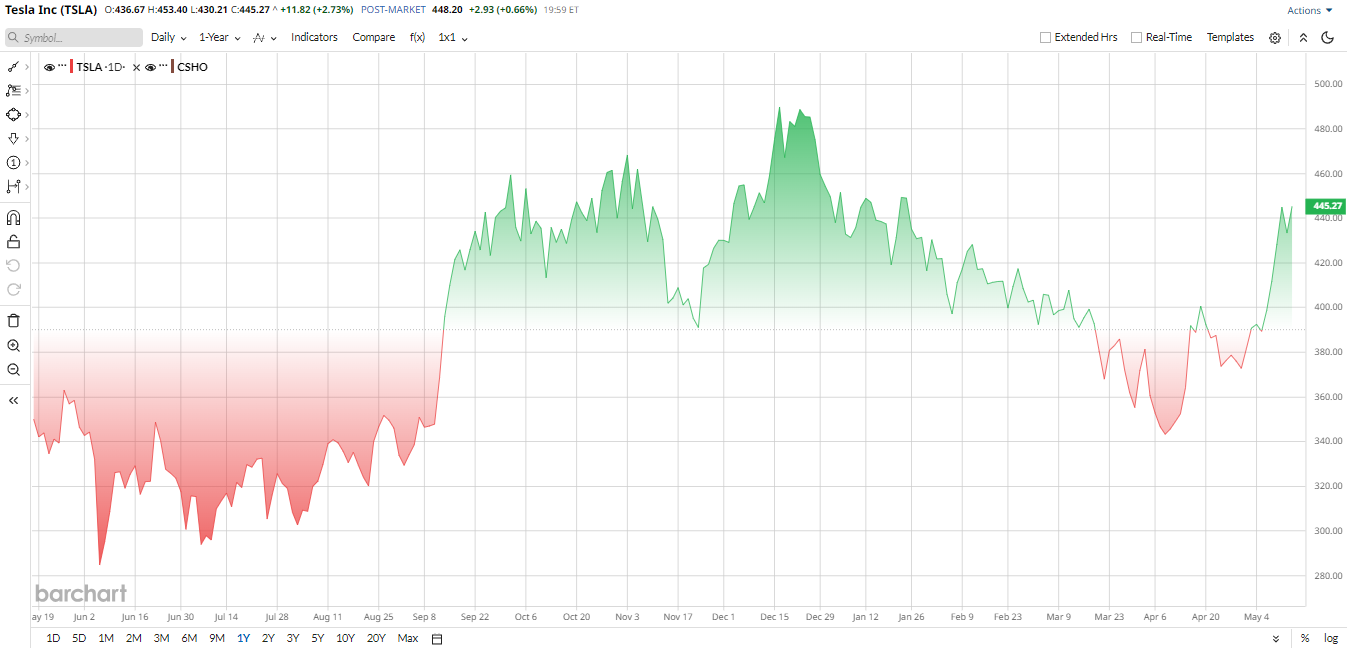

TSLA stock has also been moving around a lot. Currently, shares are up 25% over the past 12 months, but still trade about 15% below the 52-week high of $499.83. Tesla is also down roughly 5% on a year-to-date (YTD) basis.

More importantly, shares have pushed back above the 200-day moving average and cleared an aggressive buy point around $409, which tells you the market is still willing to pay up when the narrative turns brighter. China sales, AI hopes, and FSD speculation have all helped.

Despite underperformance, the valuation still looks rich. Tesla trades at 369 times forward earnings, while Toyota (TM) and General Motors (GM) trade at much lower single-digit multiples. That is the market saying Tesla is not really being priced as an automaker anymore. Rather, it is being priced as a future autonomy platform. Morgan Stanley has also said the stock already reflects a lot of its EV, AI and energy story, which is another way of saying investors are paying up for success that has not fully arrived yet.

Tesla Doubles Down on Europe

The recent Germany news fits Tesla’s bigger plan. The extra $250 million should help lock in European battery supply and push Berlin’s output higher. That is smart. But it also comes on top of a much bigger spending wave. Tesla has already told investors that 2026 capital spending will climb to more than $25 billion — nearly triple last year’s $8.5 billion — and management has said free cash flow could be negative for the rest of 2026.

We can say that the Berlin move is strategic, but it is not a near-term profit boost. Instead, it is another spending item in a year full of spending items.

Q1 Looked Good, But Not Spotless

The latest quarterly results were solid on the surface, but they were not as clean underneath. Tesla posted first-quarter revenue of $22.39 billion, up 16% year-over-year (YOY). Automotive revenue rose to $16.23 billion, while energy generation and storage revenue fell 12% to $2.41 billion, and services and other sales climbed 42% to $3.74 billion. Net income for the period came in at $477 million, up 17% YOY, while adjusted EPS was $0.41, up nearly 52%. Free cash flow was $1.44 billion while cash and short-term investments came to $44.74 billion.

Tesla also said revenue got help from FX and one-time auto benefits, while regulatory credit revenue fell to $380 million from $595 million a year ago. That is the part investors should not ignore — Q1 was good, but it was not bulletproof.

The real issue is what comes next. Tesla is building out robotaxis in Dallas and Houston, working on broader FSD approval in Europe, and pushing a cheaper compact SUV. The company is also moving faster on the Cybercab, Semi and Optimus.

That all sounds great, but most of it is still early. TSLA stock is being asked to fund a future that is not yet producing enough revenue to support the spending. That is why the Germany investment feels both promising and a little uneasy at the same time.

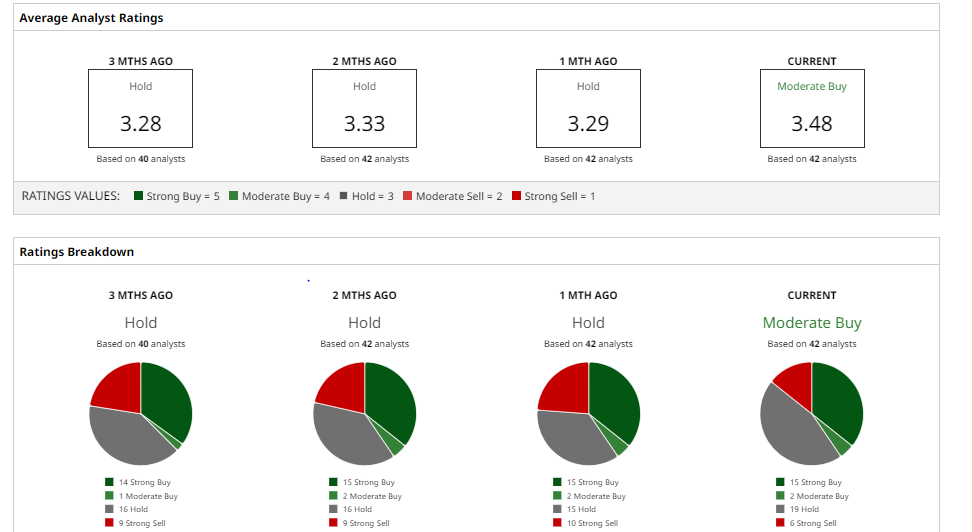

What Do Analysts Say About TSLA Stock?

Analysts are still split on TSLA stock, and that is probably the most honest read on the company today. BofA recently reinstated Tesla at a “Buy” rating with a $460 price target, saying the company leads in consumer autonomy. TD Cowen cut its target to $490 from $519 but kept a “Buy” rating, still leaning on robotaxis and FSD. Morgan Stanley has an “Equal Weight” rating with a $415 target and believes that the robotaxi rollout is a key catalyst.

JPMorgan is far more cautious with a “Sell” rating and $145 target. Analysts warn that TSLA stock could fall sharply if the cash flow and delivery story keeps weakening.

Overall, Wall Street looks more neutral than bullish. However, the consensus rating is a “Moderate Buy” with an average price target of $401.77. That suggests the stock has potential downside of 5% from current levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)