/Dexcom%20Inc%20logo%20on%20phone%20-by%20T_Schneider%20via%20Shutterstock.jpg)

California-based DexCom, Inc. (DXCM) is a leading medical technology company specializing in continuous glucose monitoring (CGM) systems for people with diabetes. With a market cap of $22.3 billion, the company develops wearable sensors and software platforms that allow users to track glucose levels in real time without the need for frequent fingerstick testing.

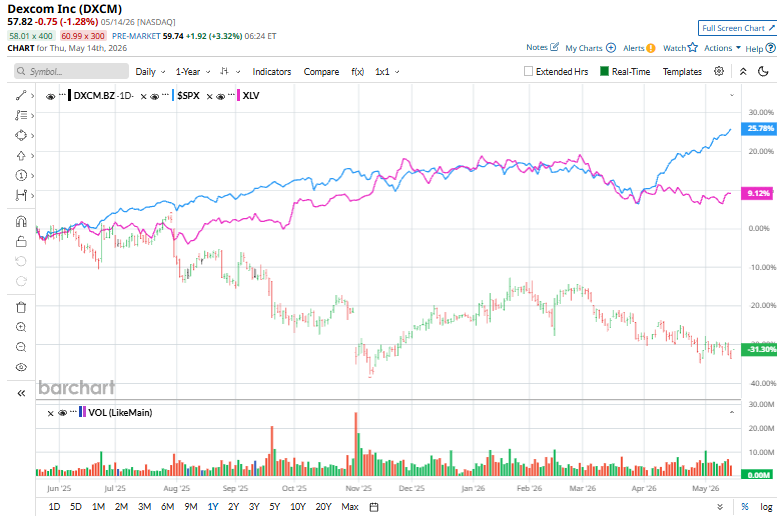

Shares of the medical device company have underperformed the broader market over the past 52 weeks. DXCM stock has declined 33.7% over this time frame, while the broader S&P 500 Index ($SPX) has gained 27.3%. Moreover, the stock has decreased 12.9% on a YTD basis, slightly outpacing SPX's 9.6% gain.

Further, shares of DXCM have also lagged behind the State Street Health Care Select Sector SPDR ETF's (XLV) 13.9% rise over the past 52 weeks and have dropped 5.3% in 2026.

On Apr. 30, DexCom shares popped 3.5% after the company announced the FY2026 Q1 results. Revenue rose 15% year over year to $1.19 billion, or 12% on an organic basis, exceeding Wall Street expectations, driven by continued global adoption of its continuous glucose monitoring (CGM) systems, expanding Type 2 diabetes penetration, and accelerating uptake of its G7 platform. U.S. revenue increased 10.9% to $832.30 million, while international revenue surged 26% to $356.90 million, reflecting strong global demand and expanding reimbursement access. Its non-GAAP EPS jumped 75% year over year to $0.56.

For the fiscal year that ended in December 2025, analysts expect DXCM's adjusted EPS to increase 22.5% year-over-year to $2.56. The company's earnings surprise history is stellar. It beat the consensus estimates in each of the last four quarters.

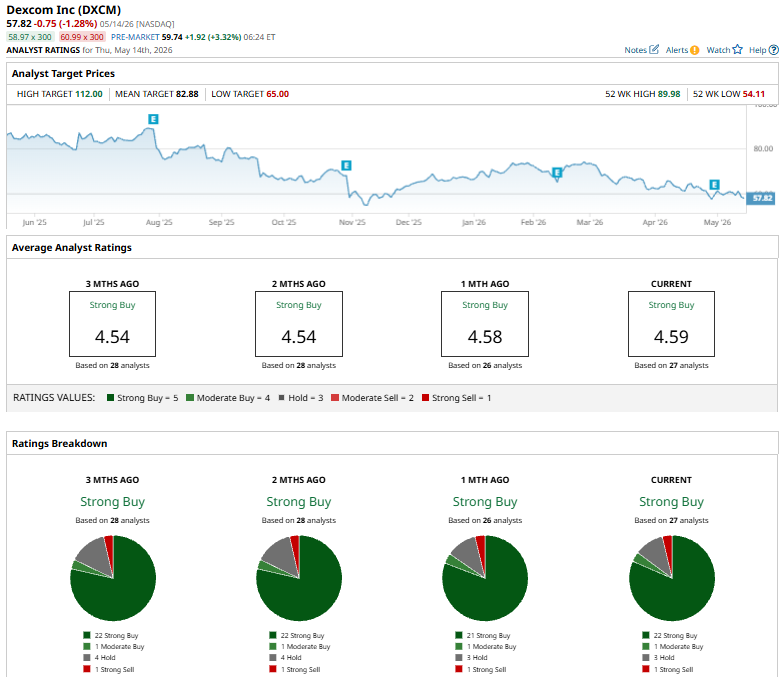

Among the 27 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 22 “Strong Buy” ratings, one “Moderate Buy,” three “Holds,” and one “Strong Sell.”

This configuration is bullish than a months ago when the stock had 21 “Strong Buy” suggestions.

On May 4, Citigroup analyst Joanne Wuensch reiterated a “Buy” rating on DexCom while lowering the price target to $79 from $84.

The mean price target of $82.88 represents a premium of 43.3% to DXCM's current levels. The Street-high price target of $112 implies a solid potential upside of 93.7% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.